Global| Jun 06 2017

Global| Jun 06 2017Euro Area Retail Sales Inch Ahead But Still Manage to Look 'Solid Enough'

Summary

It is odd how sales can be so weak and yet appear to be so firm. It a trick that retail sales in the EMU area seems to have been able to perform. Real sales are up by just 2.4% over 12 months and just 2.2% for nonfoods. Yet, three- [...]

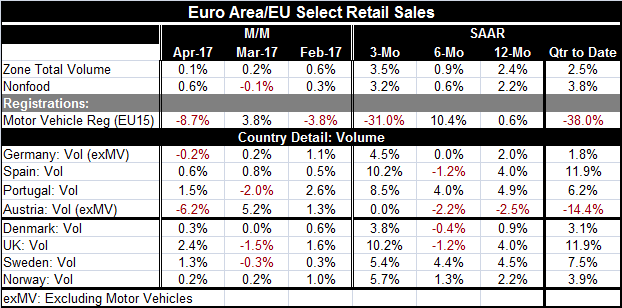

It is odd how sales can be so weak and yet appear to be so firm. It a trick that retail sales in the EMU area seems to have been able to perform. Real sales are up by just 2.4% over 12 months and just 2.2% for nonfoods. Yet, three-month, six-month and 12-month growth rates for both series are all positive and the recent three-month growth rate is accelerating to over a 3% pace for each series. In the quarter-to-date (an early concept in April), retail sales are up at a 2.5% annualized pace even though vehicle registrations seem to be in trouble, falling sharply in April and plunging in the quarter-to-date.

It is odd how sales can be so weak and yet appear to be so firm. It a trick that retail sales in the EMU area seems to have been able to perform. Real sales are up by just 2.4% over 12 months and just 2.2% for nonfoods. Yet, three-month, six-month and 12-month growth rates for both series are all positive and the recent three-month growth rate is accelerating to over a 3% pace for each series. In the quarter-to-date (an early concept in April), retail sales are up at a 2.5% annualized pace even though vehicle registrations seem to be in trouble, falling sharply in April and plunging in the quarter-to-date.

Across the EMU and in Europe, retail sales seem to be on something like cruise-control. The pace is rarely very hot and there is no evidence of sales about to stall. Sales look their weakest over six months a venue over which EMU-wide sales volumes slip to under a 1% pace and Spain logs a sales drop along with Austria. The non-EMU nations of Denmark and the U.K. also experience a sales decline over six months.

But across the EMU, sales are up by 0.9% or more everywhere except in Austria when sales, while falling over 12 months, are actually on a consistent improving path over shorter horizons. The pace of sales across countries on a quarter-to-date basis ranges from 1.8% in Germany to 11.9% in Spain and in the UK - omitting Austria. Austria has the unfortunate problem of logging a sharp sales decline in April which has driven its quarter-to-date retail sales growth rate deeply into negative territory. However, its 6.2% plunge in April follows a 5.2% rise; thus, Austria seems to be caught in a period of volatility more than weakness, but time will make that clearer.

The only really troubling trend in the table of retail sales and auto registrations is the recent performance of auto registrations. That series is often volatile, but it is also sharply lower in April after swinging widely down then up in February and March. The U.S. is also starting to see some prevarication in its own auto sales after autos have strongly driven U.S. retail sales gains. I know of no connection between European registrations and U.S. sales and in fact U.S. sales have a number of very local peculiarities that are nagging at sales stemming from excess and bad lending practices to an outsized number of vehicles coming off lease to compete with new car sales. But like the U.S., Europe has seen a strong and steady revival in vehicle registrations that may no longer be so compelling moving forward for some of the same reasons stemming from demographics to the catch up of sales to past demand.

For the moment, Europe's retail sales are looking consistent. They are not accelerating and do not appear to be strong in any fashion, but they do not seem threatened either. My best descriptor for them is 'consistent.' To keep growth on track in the EMU, sales are going to have to continue to expand. On these trends, that does not seem to be at risk.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief