Global| May 23 2016

Global| May 23 2016Euro Area PMI Weakens As the Fed Rattles Its Policy Saber

Summary

Conditions and patterns vary across EMU-somewhat by size The EMU region seems to be a story of `rich getting richer and poor getting poorer.' Both France and Germany have seen their composite PMI gauges rise in May. They are the two [...]

Conditions and patterns vary across EMU-somewhat by size

Conditions and patterns vary across EMU-somewhat by size

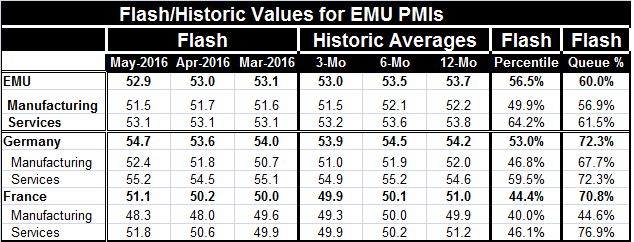

The EMU region seems to be a story of `rich getting richer and poor getting poorer.' Both France and Germany have seen their composite PMI gauges rise in May. They are the two largest EMU economies and carry the two largest weights in the EMU composite index. Although both Germany and France showed advances, the EMU region index fell, which means that the other countries whose data are embedded in the EMU index weakened much more substantially overpowering the impact on the EMU index of its two largest members. Both France and Germany also carry higher queue standings for their respective PMIs than the EMU as a whole. That implies that the other countries which have not yet reported have relatively weak queue standings. I refer here to the queue standings not to the raw diffusion index since Germany has a diffusion composite greater than that for the EMU while France's is lower.

Sectors

The EMU sector aggregates shows a slightly weaker manufacturing gauge on the month with the services gauge stuck at the same level for three months running (at a 61.5% standing). Germany's manufacturing and services sector gauges each improved in May. France saw its manufacturing gauge improve in tandem with services, but manufacturing still does not get back to 50 and still registers contraction.

Sector standing

The German Manufacturing sector has 67.7 percentile standing with services at its 72.3 percentile standing. France's indicators show much more divergence with manufacturing at a weak 44.6 percentile standing and services at a 76.9 percentile standing. France has a lower manufacturing standing than either the EMU or Germany and French services have a standing in excess of either the EMU or German services. However, the absolute levels for diffusion are greatest for each of the German sectors.

These statements help to clarify the conditions in the EMU vis a vis the two largest economies with clear implied conditions for the rest. This month has not been kind to the rest of the EMU.

Trends in EMU within EMU

Trends show that the EMU composite in May is weaker than its previous three-month, six-month and 12-month averages. The averages themselves show steady decay. The EMU sector components show decay even including the May values. This again speaks to conditions outside of the two largest economies. In contrast German shows a surge in its May composite reading relative to its past moving averages, each of which it stands above. The German composite averages have no clear pattern of acceleration or deceleration. But German manufacturing sector patterns show steadily eroding period averages with an up-move in May. German services are mostly firm with sideways momentum. France's composite moving average shows mostly stability with some erosion over three months but with a May reading above (slightly) all the period moving average values. The patterns of its manufacturing and services sectors show some weakening in manufacturing (which dips over three months) while services averages erode more steadily. Services show some lift in May while manufacturing does not.

Down the rabbit hole with the Fed

The Fed is saying that international risks are gone or are greatly diminished. But we are seeing some oil market and stock market backtracking in global markets as they puzzle-out the Fed's actions. The Fed has been unable to sort out the classic simultaneity problem: there are significant global feedback responses from its own actions. Therefore, the Fed cannot sketch out a path for itself nor can it assess pre-conditions of the global economy without taking its own actions into account. It, in fact, is doing that, but that very act is a fallacy. Each time the Fed tries to construe global conditions as safe and stable, it sets out to normalized U.S. policies which means to take (at some speed) the fed funds rate to the 3.5% to 4% level and when that actuality is known to markets it destabilizes them. The Fed is stuck in a box or loop with no escape. I look for that to continue to play out. It does not matter what the Fed members think; their actions will continue to bump up against the constraint of reality and that will force policy modification and moderation.

The importance of making the right judgement

EMU and other global data suggest to me that the Fed has judged the international economy wrong. These data also suggest that the Fed decided to make its move to normalcy too soon. In short, the December rate hike and the starting point for the normalization process was a mistake. The Fed has misjudged the extent of the linages of the U.S. to global economy and the dependency of the global economy on the U.S. and on dollar's value. The Fed has all but completely ignored the transmission from the dollar to commodity prices and global markets well as undervaluing the impact of a strengthening dollar to the global economy overall- and the connection of both of those things to U.S. monetary policy. These are significant misjudgments and they will define the risks for the period ahead. The weakness in the EMU especially for the peripheral countries appears to underline that fragility.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief