Global| Nov 23 2016

Global| Nov 23 2016Euro Area PMI Hits Year's High

Summary

EMU PMIs make a push for the mediocre levels of readings that prevailed earlier in this cycle. The EMU is improving and the very weak readings of 2016 are being put behind it. Still, there is a long way to go to reach true normalcy [...]

EMU PMIs make a push for the mediocre levels of readings that prevailed earlier in this cycle. The EMU is improving and the very weak readings of 2016 are being put behind it. Still, there is a long way to go to reach true normalcy and longer still before we think of any real strength. But by the relative standards on the past six years, the current lot of PMI readings range from 'firm' to 'strong' on a relativistic scale.

EMU PMIs make a push for the mediocre levels of readings that prevailed earlier in this cycle. The EMU is improving and the very weak readings of 2016 are being put behind it. Still, there is a long way to go to reach true normalcy and longer still before we think of any real strength. But by the relative standards on the past six years, the current lot of PMI readings range from 'firm' to 'strong' on a relativistic scale.

EMU readings are big fish in a small pond

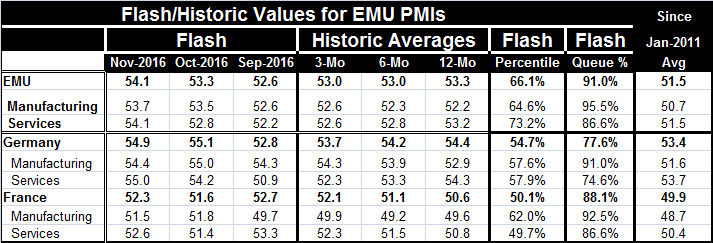

At 54.1 the EMU private sector PMI has been stronger over the past six years only about 9% of the time. But on this horizon, the PMI only averaged a reading of 51.5 and that is barely signaling expansion. The sequential averages show a steady diet of readings at 53 over three months, six months and 12 months. This month's 54.1 breaks out of that range. All in all, it's not much of a break-out and too soon to get excited about there being any new trend. The readings for EMU manufacturing are steady with a slight acceleration built into the raw readings that cluster around vales of 52 on the diffusion scale. The November manufacturing reading is above this (at 53.7) with a percentile standing that is this high or higher less than 4.5% of the time. But that is on a diffusion index that has averaged only 50.7 over the past six years making the PMI's ranking accomplishment considerably less effusive. The services moving averages actually show a tiny bit of deceleration in train. Still, the November services reading popped to 54.1 from 52.8 and it is well above its previous sequential averages. The queue standing for the services gauge is in its 86th percentile; its six-year average raw diffusion score is only 51.5. So, yes, the EMU is doing better and there is some pick up involved, but it is still a moderate and nascent rebound after a period of substantial sluggishness.

Germany- very mixed (mixed up!) momentum

Germany shares many of the traits of the EMU index, which is not too surprising since Germany carries a large weigh in the EMU as the largest economy in the euro area. The German manufacturing index actually is getting stronger on its progressive averages, while its services sector is getting weaker on the same timeline. Still, both the manufacturing sector and the services sectors show relatively strong values in November that elevate them above their respective three-month averages. The increment for manufacturing is thin since manufacturing in Germany actually slowed a bit in November. The German manufacturing gauge has a 91st percentile standing in its six-year queue while the services sector standing is in its 74th percentile, considerably more moderate. Yet, manufacturing has only averaged a diffusion reading at 51.6 over the last six years while services has lodged an average value at a more respectable 53.7. In relative terms, manufacturing is breaking out, but in reality it is breaking out from an extremely weak set of historic readings plus it is weakening on the month. Contrarily, services have been slowing, but they accelerated this month. All this leaves Germany with uncertain momentum.

France- a clear but slow pick up for an economy that desperately needs it

France has been a study in weakness. And while its trends are generally positive and its diffusion readings show progress compared to the last six years, we are looking at a comparison with PMI readings that have been and still are quite weak to moderate. For example, manufacturing in France has PMI values that are below 50 on all horizons (all averages are calculated with a one-month lag on actual, not flash data, excluding the current month's value). But the current manufacturing index is higher than its three-month average for both manufacturing and services. Still at 51.5 and 52.6 for manufacturing and services, respectively, these are the weakest indices for November in the table. Still, the standing of French manufacturing is in its 92nd percentile and for services the standing is in its 86th percentile. These values are strong standings connected to weak current monthly diffusion observations, but they represent considerable progress for France. Its six-year average for manufacturing is 48.7 and for service is 50.4.

Summing up: progress amid fragility

The above comparisons show that there is some monthly pick-up to most of these readings but that the levels of activity being attained are still quite modest. Even when the pick-up is solid by historic standards, it is weak enough to be tentative. The ECB policies are not clearly gaining the central bank any traction. European inflation is rising for the headline and less clear excluding energy prices/costs. The world is awaiting the outcome of the OPEC meeting where a great deal of skepticism exists even as the market has backed up to give the meeting some respect. On many fronts, the global economic and geopolitical scene still exhibits a great deal of unrest or uncertainty. There has been some revival, but the PMIs are sensitive gauges and liable to be among the first indicators to pick this up. Still, whatever pick-up there is still is in need of nurturing. And yet it will have to weather whatever OPEC does, the Italian referendum results in early December and the Fed's December action which is expected to bring a rate hike.

Reassurances that do not reassure

In his recent remarks, the Fed Vice Chair Stanley Fischer has 'reassured' us that the dollar will not stand in the way of the Fed doing what it needs to do. Actually that statement goes a long way toward frightening me rather than reassuring me. The Fed needs to wrap its arms around the dollar and understand how deflationary a dollar rise might be for the rest of the world in this environment. The Fed seems to be clueless or at least of a different opinion in this regard. I think it is in error. I see Stanley Fischer making his second big mistake. The first one was telling the markets last year how wrong they were and that there would be perhaps four rate hikes. Now he is trying to reassure us that the Fed will not let the prospect of a strong dollar deter it from raising rates. That means as the Fed hikes rates and the dollar reacts there will be no circumspection about whether the dollar's gain will put the Fed on hold and that will goad the markets on to more dollar-buying. Doesn't the Fed know by now how that works? Wasn't that all made clear last year in the wake if the Fed's single rate hike? The dollar is highly reactive to Fed policy moves. Beware.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief