Global| Jan 07 2015

Global| Jan 07 2015Euro Area Pairs High Unemployment with Deflation Showdown at Not-So-OK Corral

Summary

During the euro area crisis, Europeans contended that the European Monetary Union was and is a political union much more than an economic union. And we can see that this is true because what is happening here is not for the betterment [...]

During the euro area crisis, Europeans contended that the European Monetary Union was and is a political union much more than an economic union. And we can see that this is true because what is happening here is not for the betterment of economic conditions in Europe.

During the euro area crisis, Europeans contended that the European Monetary Union was and is a political union much more than an economic union. And we can see that this is true because what is happening here is not for the betterment of economic conditions in Europe.

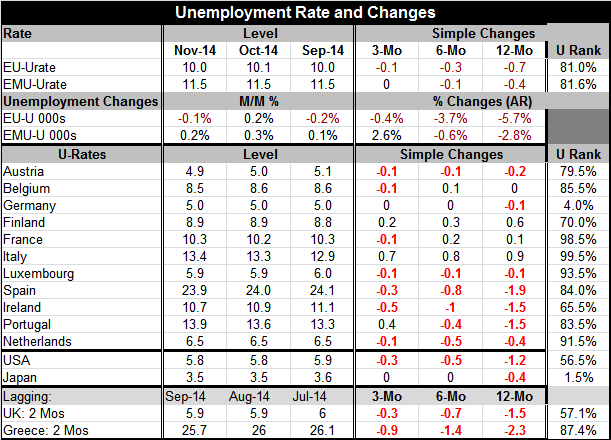

The Union weathered the storm. It bailed out Greece (a country that now needs another bailout) and assisted Cyprus, also painfully (for Cyprus). And now the `union' is together but it is falling apart together.. but not quite altogether. Germany still is running quite low but positive inflation and look! It also has its unemployment rate at its all-time low! While in Italy has an unemployment rate that is at an all-time high! For EMU as a whole, the unemployment rate has been higher only 11% of the time. However, except for Finland and Germany, all the EMU members in the table are worse off than that.

Of course, there is deflation, too. Some will argue it is not real deflation. The core HICP gauge is up by 0.8% year-over-year. It is not falling. It is, however, decelerating. And while oil prices may have tipped the balance on the HICP, it is the gauge that the ECB has been determined to target, knowing that such problems would occur. Moreover, not only did oil prices fall in December, they are still falling in January. And there is undoubtedly more `deflation' in the pipeline from the knock on effects. This deflation may be induced by oil, but the oil price plunge is now so extreme it would be foolish to argue that the deflation is not real.

Europe may seem to get a relatively pure stimulative effect from dropping oil prices as it is not a producer. But we can see in the U.S. that a steel company (also not an oil producer) has furloughed over 600 workers who were making pipe for the oil sector. Germany in particular exports capital equipment. Norway and the U.K are going to get pulled into the oil vortex since they are producers. Still, the capital goods sector may get hit hard - even if selectively- as oil production and exploration is cut back.

For Europe, the continuing and more serious problem is the political impact that stems from heterogeneity: the uneven impact of the ongoing economic slowdown. If the Monetary Union is mainly a political construction, it will need a political solution to its divisive economic problems. The table provides the percentile standings of unemployment rates by country and region. It is an astonishing table with Germany looking like it is on different planet from the rest of the EMU, not in the same union. The German unemployment rate at 5% is at an all-time low. Since the EMU was formed, Italy is at an all-time high. Four countries in the table have unemployment rates that are higher less than 10% of the time.

In terms of dynamics, seven of eleven members in the table have unemployment rates that have fallen over three months; six have rates that have fallen over six months. Seven have rates that have fallen over 12 months. The experience is slightly tilted to see more unemployment rate declines, but the tilt is not decisive.

It is the heterogeneity of the experience that is most decisive especially with Germany, the country experiencing the least pain that also is pushing to take the least action to remedy the situation. Germany as the largest economy in the EMU has clout. It is hard to see how this does not end badly. Germany desperately needs to show some flexibility; instead it seems to be even more rigid. The euro area may have its showdown at last.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief