Global| Apr 23 2008

Global| Apr 23 2008Euro Area Orders Stabilize: A Leading or Misleading Statistic?

Summary

What is for real and what is whistling past the graveyard? Tangled trends Euro Area orders are up in February, making it a two-month gain following a dive in December. Still the 3-month growth rate is negative for orders at a -3.9% [...]

What is for real and what is whistling past the

graveyard?

Tangled trends

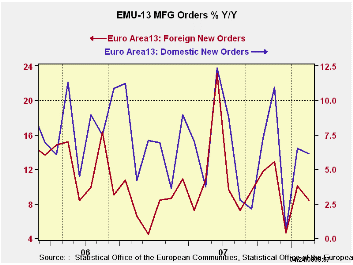

Euro Area orders are up in February, making it a two-month gain

following a dive in December. Still the 3-month growth rate is negative

for orders at a -3.9% compared to an annual rate gains of 6% over six

months and 6.6% over 12-months. So the sequential growth rates point to

some sliding in growth despite recent two-month pickup.

Orders: the lagging leading statistic…

More to the point is the fact that the orders figures for the Euro Area

are for February when many other series at the country level already

are available for March. Survey data are beginning to come available

for April as we saw in the release of the Belgian National Bank’s April

index that plunged – ironically, led by weakness in orders. The Belgian

index April result is nothing like the recent numbers we are seeing

through April. Still, the BNB survey, truncated at February, would have

been quite compatible with the figures in the table above. That begs

the question of what the trend really is, doesn’t it? At the end of the

month we we’ll get the comprehensive survey results for April that

addresses the sectors of the Euro Area and EU from the European

Commission. Based on the Belgian report we would seem to have a much

darker set of trends that will be placed before us. Germany’s Zew index

for April is already in hand and it shows a weakening in expectations

to a very low level with some so-far minor weakness in current

conditions. But this is a survey of expectations among financial

experts. The upcoming German IFO report will survey the industrial and

other sector participants directly about how their businesses are

performing. .

The drop off in the Belgian index is still isolated but it is highly

topical and reasonably comprehensive across sectors… and it is an index

known to have leading indicator properties.

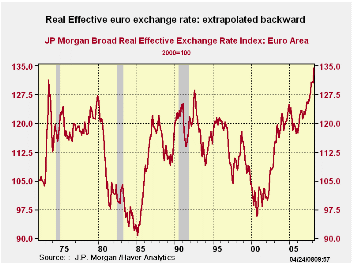

Whistling past the graveyard?

For my taste the smugness of the European reaction to ongoing growth

there and the ECB’s stubbornness in ignoring the high euro exchange

rate value in setting policy has been hard to stomach since this

behavior has sent inconsistent signals to the markets. In looking at

the euro historically –even extending the construction of a ‘synthetic

euro’ back to the early years of fluctuating exchange rates- it is

PAINFULLY clear how overvalued that rate has become – and not just VS

the dollar! All the talk of how robust Germany’s economy remains in the

face of this strikes me as akin to the Spartans swallowing their teeth

to hide the fact that they have been injured. The index above is broad

and inflation adjusted. It is the real deal showing ‘euro’

competitiveness at its lowest level in 36 years – or more. The ECB’s

ignoring this clearly deflationary force in setting policy is similarly

puzzling. The real, broad euro exchange rate stands nearly 20% above

its average for the period.

Single mandate does

not mean closed-minded

Single mandate does

not mean closed-minded

It does not matter if the ECB has a singular focus and mandate on

inflation with no growth mandate at all. To crank rates up and to

threaten to do it some more as temporary ‘inflation’ effects wash

through economy when they ‘know’ there is a powerful deflation force at

work (i.e. the overly strong euro) is not good monetary policy. The

German government has long known its place in such monetary fights and

has taken to extolling the benefits of a strong euro. I guess the

response there is this: If you can’t beat ‘em, join ‘em. Thus the

German economics and finance ministries seem in some way complicit with

this policy of excessive anti-inflation zeal. It may be that ECB-types

feel they have to lean hard against the unwanted advice urging

flexibility from the IMF. The International Monetary Fund said Monday

in its latest Regional Economic Outlook for Europe that the European

Central Bank has some leeway to loosen its monetary stance. Today aft r

the euro has screamed higher, the IMF’s John Lipsky has called euro

monetary policy appropriate as it is. I don’t know if that will end

this verbal silliness or not.

Right hand does not seem to know (or care?) what the left is

doing…

So the economic growth/inflation outlooks and assessments have flies in

the ointment. Unfortunately it seems that the more topical reports are

the weaker ones. While the title ‘industrial orders’ sounds like a

leading sort of barometer, no report is any fresher than the data it

contains. If this one continued fish you would not touch it. The

topical reports lead us to be cautious in the assessment of current

trends. Germany and Europe have for too long been too resistant to the

impact of a euro whose strength has been eating away ravenously at

their competitive positive. The resiliency of the economic data has

belied the urgency in the tone of policy makers who have sought some

help in stemming the euro’s rise. But, in the end, you can’t have it

both ways. If the euro is too strong it must do damage. If it does not,

it is not too strong. If policy markers are going to extol the vibrant

nature of their own economies as its fundamentals are being undercut

surely they can expect no urgency to help them with their nonexistent

FX problem!

Call to action: THINK!

Governmental and central banking policymakers must be on the same page

and willing to look ahead if they are to foster a correct view of their

economy. For the moment we continue to have the sort of fair-weather

analysis from officials that we were spoon fed by commercial bankers

over the previous year. We know what that is worth. It is a good time

to look closely at the data yourself and remember the key

constituencies of the policymakers that go public. I think we may be in

for a rude awakening. But that’s only one man’s opinion. And economists

are wrong at least as often as markets are… Who is ‘wrong’ now?

| Euro Area and UK Industrial Orders & Sales Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | % m/m | Feb-08 | Feb-07 | Feb-06 | Qtr-2 Date |

||||

| Euro Area Detail | Feb-08 | Jan-08 | Dec-07 | 3Mo | 6mo | 12mo | 12mo | 12mo | Saar |

| Manufacturing Orders | 0.6% | 2.2% | -3.7% | -3.9% | 6.0% | 6.6% | 7.0% | 11.1% | 2.7% |

| MFG Orders | |||||||||

| Total Orders | 0.6% | 2.2% | -3.7% | -3.9% | 6.0% | 6.6% | 7.0% | 11.1% | 2.7% |

| Countries: | Feb-08 | Jan-08 | Dec-07 | 3Mo | 6mo | 12mo | 12mo | 12mo | Qtr-2 Date |

| Germany: | -0.1% | 0.1% | -1.6% | -6.5% | 7.7% | 5.9% | 12.7% | 12.3% | -0.9% |

| France: | 1.0% | 4.1% | -1.7% | 14.2% | 5.7% | 9.7% | 5.9% | 4.7% | 17.8% |

| Italy | 2.0% | 2.8% | -5.2% | -2.5% | 3.9% | 9.9% | 1.6% | 11.4% | 5.5% |

| UK (EU) | -13.2% | 23.8% | -6.3% | 2.9% | 4.6% | 13.7% | -7.5% | 15.8% | 81.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.