Global| Oct 27 2015

Global| Oct 27 2015Euro Area Money and Credit Pause and Dip

Summary

While we are looking at growth and inflation developments in the EMU, we should also be looking at the financial raw material of growth: money and credit in the EMU. Here we see both series are slowing after about one year of [...]

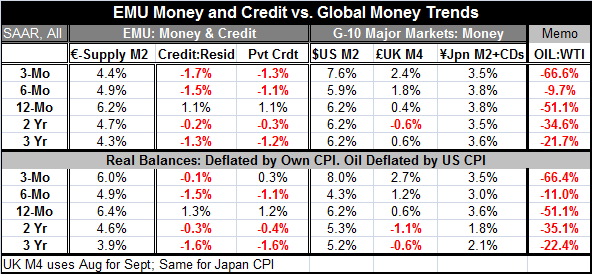

While we are looking at growth and inflation developments in the EMU, we should also be looking at the financial raw material of growth: money and credit in the EMU. Here we see both series are slowing after about one year of acceleration. Real money growth and real credit growth are flirting with negative growth rates. Only over 12 months are money and credit both posting growth rates of more than 1% in real terms, breaking a two-year string of real (inflation adjusted) declines.

While we are looking at growth and inflation developments in the EMU, we should also be looking at the financial raw material of growth: money and credit in the EMU. Here we see both series are slowing after about one year of acceleration. Real money growth and real credit growth are flirting with negative growth rates. Only over 12 months are money and credit both posting growth rates of more than 1% in real terms, breaking a two-year string of real (inflation adjusted) declines.

For a short while, as ECB QE was announced and implemented, there seemed to a response in the form of a pick-up in loan volume. Private credit has registered positive year-over-year growth for nine consecutive months, with only one minor deceleration, until now. In September, total private credit growth dropped to 1.1% from 1.7% and it is the slowest year-over-year credit growth in five months.

The combination of the return of deflation - or at least disinflation, continued plodding growth and now weak money and credit growth should sound alarm bells at the ECB. It appears that it has. But our recent history shows that QE has seemed to have had the most potent impact when done quickly and early in a zero rate environment. The ECB has delayed and is now trying to implement this program with interest rates already exceedingly low. Japan's and the U.S. experiences show us that the impact of QE on the exchange rate is fleeting. But the EMU is showing us that in this environment, even of the exchange rate is pushed lower, there is precious little to be gained from it. Global growth is simply very weak and improved price competitiveness does not get much purchase for exports.

The U.S. and the U.K. each are showing some slight acceleration in the growth rate of money supply. Japan is mostly stable with a slightly weaker three-month pace. The real money stock grows slightly faster in the U.S. and the U.K. while Japan shows a halting slowdown. Why do the countries that are now implementing QE and using it for stimulus have the weakest money supply growth and a withering trend? Money supply data show no hints that special monetary accommodations are being implemented in Japan or in the EMU. Of course, we know that both started operations and have been on hold since. Both have given some lip service to the possibility of doing more. We shall see.

More economists are prevaricating on the future path for growth. We cannot say that this economic recovery is long in the tooth. And we can observe that it has been one of the weaker recoveries in the post war period for G-10 member nations. Despite that, demographic changes in the U.S. have the authorities there thinking that there is not much labor market slack and the Fed is `planning' (scheming?) to hike rates.

The U.S., EMU and the whole of the global economy are at an odd crossroads: hopefully not a tipping point. Economic development conducted without a mind to getting exchange rates right has run amok. China's desire to develop fast come hell or high water has taken a toll on the global economy. China's speed of development has been a critical part the malaise that has developed. And now the inability to keep up that pace will become China's own problem. Meanwhile exchange rates are still out of alignment and being pulled this way and that by monetary policy excesses. The Fed in the U.S. is set to hike rates. That will pull an already overvalued dollar higher, undercutting further opportunities for investment and employment in the U.S.

Europe is still under the vision of German austerity and perhaps ready to unleash another round of soon-to-be disappointing QE. Japan is slowing as its own QE has become progressively less effective. We seem to live in a world without options or where the best options for growth are being shuttered.

Europe's dilemma is being played out globally as monetary solutions are sought to problems that are not monetary in nature. These solutions are doomed not to work, but they do buy time and do so at a cost. There is little to make us optimistic.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief