Global| Aug 12 2020

Global| Aug 12 2020Euro Area IP Continues Its Rapid-Fire Recovery

Summary

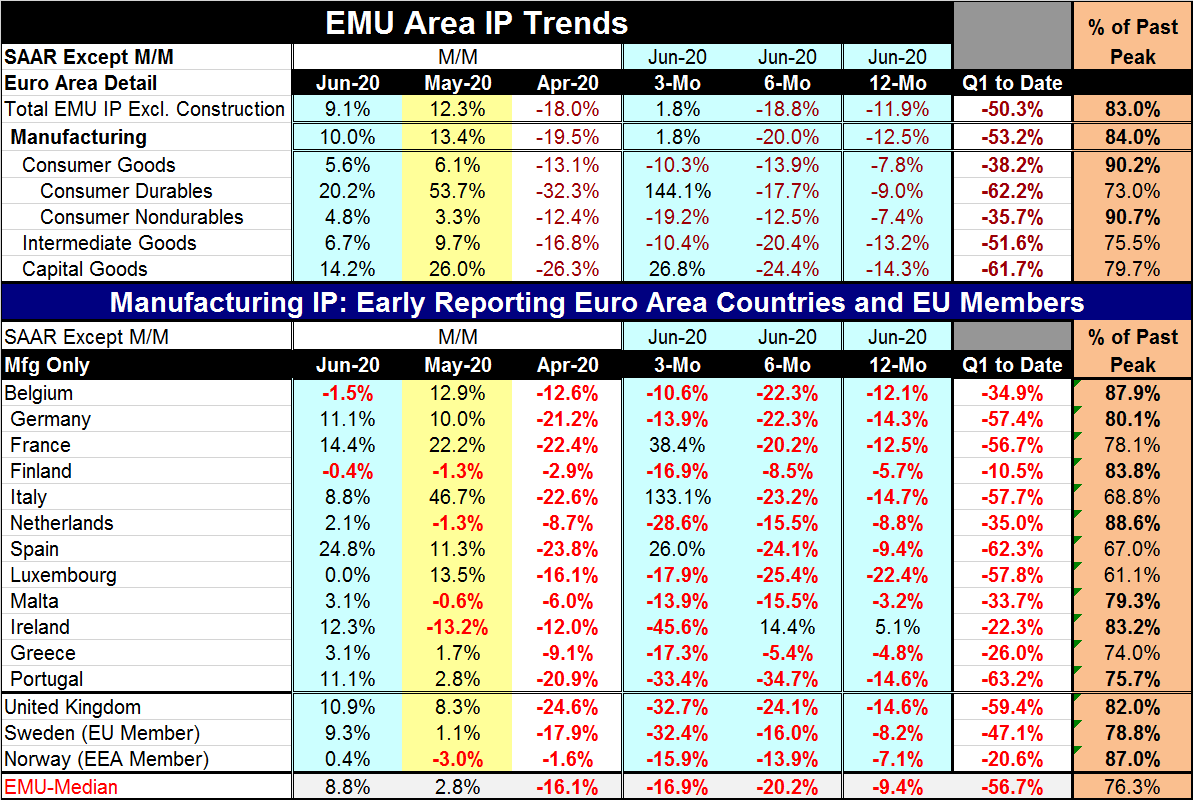

There are at least two views of the ongoing European recovery in production. One is expressed by the chart. It shows a relatively strong V-shaped rebound but one that leaves output still declining on balance in each major sector [...]

There are at least two views of the ongoing European recovery in production. One is expressed by the chart. It shows a relatively strong V-shaped rebound but one that leaves output still declining on balance in each major sector relative to its value of one-year ago. The other view simply looks at the strength over the last two months where output has recovered by over 20% from its pit in April. And looking ahead at IP if output were to remain at its current level and not change at all in July, August and September, the annualized growth rate for IP in Q3 would be at an 45% annual rate compared to Q2. Already the recovery late in Q2 is so powerful that an exceptionally strong Q3 is ‘in the bag.’ Yet, the finding of the chart is still clear and correct that output would still not be back to its pre-virus level.

There are at least two views of the ongoing European recovery in production. One is expressed by the chart. It shows a relatively strong V-shaped rebound but one that leaves output still declining on balance in each major sector relative to its value of one-year ago. The other view simply looks at the strength over the last two months where output has recovered by over 20% from its pit in April. And looking ahead at IP if output were to remain at its current level and not change at all in July, August and September, the annualized growth rate for IP in Q3 would be at an 45% annual rate compared to Q2. Already the recovery late in Q2 is so powerful that an exceptionally strong Q3 is ‘in the bag.’ Yet, the finding of the chart is still clear and correct that output would still not be back to its pre-virus level.

So there is a relative and an absolute way to look at output and its revival. The question of growth in Q3 is not very interesting per se because we can see how strong it will be from the patterns of the decline and rebound within Q2. Q2 has set up Q3 to be strong. The number does not matter. It will be an eye-popping number. But what does matter is if output is on a sustainable path higher. What matters is whether the virus has been dealt with so that life and growth can progress. And whatever the numbers that post in Q3, they alone will not answer those questions.

The table, however, shows us what is in train. Consumption is not all that strong over three months. That is because of the split trend on durables vs. nondurables. Consumer durable goods output is up at a 144.1% annual pace over three months compared to consumer nondurables where output is falling at a 19.2% annual rate. Intermediate goods output also is falling on balance over three months, at a 10.4% annual rate. But capital goods output is up at a 26.8% annual rate over three months. Manufacturing overall is up at a 1.8% annual rate. The overall quarter-to-date decline in output is at a 50.3% annual rate. That will probably be surpassed by a stronger positive number next quarter. But will it be enough?

The table contains 15 countries; 12 of them are EMU members. All but two, Belgium and Finland, show manufacturing IP gains in June. All but five show gains in May. All countries in the table show steep output declines ranging from -1.6% in Norway to -24.6% in the U.K. in April. All but three countries (France, Italy and Spain) show deep declines in manufacturing output over three months (annualized). And all but Ireland show a steep decline in output over 12 months with the median decline in the table at -9.4% year-over-year -- still nearly double digits after two strong months of rebound.

The rebound so far has been about everything one could hope for and yet it is not enough. It will take a lot more expansion to put output back on its previous path, trend and footing. It may not happen for quite a while. This rebound may be more like charging your nearly dead cell phone battery. At first it will charge up rapidly. But the closer you get to 100%, the slower it charges. The same thing is in progress with the economy especially since some service sector industries remain unable to open in full. That missing piece will hold back manufacturing as well.

What we see so far is a rapid recovery. But we also know that the virus has spread and led to another scattered lockdown-slowdown. Even New Zealand that had rid itself of the virus has discovered infection there again and is taking mitigation steps. Covid-19 is nothing if not pesky. It is very dangerous to people with preexisting medical problems and not so life threatening to the healthy or to the young. Science is making some progress in treating it. Russia claims to have a vaccine. In other countries, the race for a vaccine is still in progress. No one outside Russia is quite sure what to make of the Russian claim that it has a successful workable vaccine. For now growth in the West continues to be tentative with social distancing and mask-wearing and lots of uncertainty about the virus and its ability to spread. The outlook remains clouded but with a chance of vaccine discovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief