Global| Nov 17 2017

Global| Nov 17 2017Euro Area Current Account Surplus Hits An 'All-time' Record

Summary

Not only is the EMU current account at surplus an all-time record of 37.8 billion euros (all-time means since the area was formed in January 1999) but that surplus has been stubbornly large. And that is a symptom of something bad. We [...]

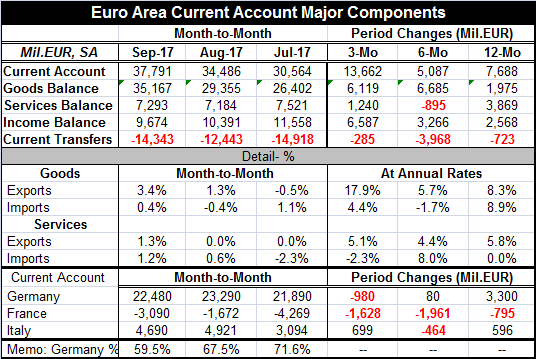

Not only is the EMU current account at surplus an all-time record of 37.8 billion euros (all-time means since the area was formed in January 1999) but that surplus has been stubbornly large. And that is a symptom of something bad.

Not only is the EMU current account at surplus an all-time record of 37.8 billion euros (all-time means since the area was formed in January 1999) but that surplus has been stubbornly large. And that is a symptom of something bad.

We live in strange times with shifting values and news that is not new or even true. We are told facts that are in dispute by some and taken as gospel by others. While some find this a curious new twist in life, I have found it the basis for global policy for some time.

For a long time, economists have promoted the notion of free trade as the best of all possible worlds. On the back of this bit of economic theory, they then strapped the lie (alternative truth) that any increase in trade was better than a situation with less trade. And they submerged any reference to the sorts of conditions that had to occur for trade to be construed as consistent with the free trade model that assures us of such grand results. In forming the euro area, many appealed to Robert Mundell's famous paper on Optimal Currency Area (OCA). It was well known that the EMU even in its original, smaller form, was not an OCA, but that sort of logic was brought forth in any event to support its formation. Germany's Helmut Kohl famously welcomed as many as wanted membership.

In the cold hard light of the morning reality, Europe has awakened in bed with something it did not expect. It now realizes that the euro area is a mostly a political construct. And it is under this political fusion that the 'natives' are starting to balk and become restless. Germany wants everyone to swallow its diktat for immigration absorption. The U.K. found this intolerable as a condition of EU membership. The EU is a broader non-currency zone relationship that is a customs union that cocoons the EMU in its center. And the union is now an agglomeration of requirements that has gone far beyond how it began.

The politics and economics have exerted strong pressures on the euro area. The uneven fiscal positions of its members and the very uneven inflation performance across members assures us that members have different interests and that is not good for an area that will have only one monetary policy and that constrains local fiscal efforts. In the wake of the recession and financial crisis, the price level disparities have been greatly reduced, but some members still have competitiveness issues. Many still have their hands tied with large stocks of debt that must be worked down.

The German's have jerry-rigged the EMU by consistently running the lowest inflation rate as we pointed out in yesterday's report on the HICPs. As a result of that strategy, the German price level has risen the least among EMU members; thus, making Germany the most competitive country in the EMU. So now at whatever exchange rate the euro has, Germany will be the EMU member that is most competitive. And this is a factor in the current account. Over the last three months, the German current account has accounted for between 60% and 70% of the EMU surplus. Germany has a locked in surplus like the EMU. And with that, the EMU is committing another disservice to economic theory by soaking up demand in the rest of the world at a time that global demand is scarce. Another way of looking at it is that the EMU, despite its wealth and position, is absorbing too few goods made overseas and selling too many of its own. The large and growing surplus contributes to euro area growth while diminishing growth elsewhere in the world.

The chart at the top shows the EMU and German current account surpluses as a percentage of GDP with the U.S. deficits as a ratio to GDP presented as well. The U.S. current account deficit ballooned its ratio to GDP in recession; it has since recovered. Since roughly 2009, the U.S. ratio, the German ratio, and the EMU ratio have all been moving higher. They should all be moving lower. These are large deficits/surpluses to GDP and the international mechanisms are supposed to cause deficits and surpluses to be competed away in a cloud of free trade through currency movements. But currency movements don't do that these days. Currency movements have been coopted by growth seeking economies to stoke their export industries. Germany has contrived a position for itself in a currency zone with much weaker members that will give it some natural shelter from exchange rate pressures and fuel its export machine. And it is not alone in this objective.

We unfortunately live a world of bait and switch or of alternative facts in which we are sold policy on the basis of one set of beliefs, but we operate in a totally different system with very different underpinnings from those sold in theory. The enormous and unmoving current account as a ratio to GDP are only codifying more trouble. The U.S. cannot continue to leach growth to the rest of the world through its current account and to mound on debt year-after-year to balance its accounts. The German surplus, the EMU surplus, and the U.S. deficit are all things that ought to ebb and flow in a dynamic trading system. But they do not. The trading system is not dynamic; it is stuck.

It is no longer clear how this situation will resolve itself. At China's recently concluded five-year party Congress, it set aside its progression toward more freedom and any hint that capitalism was encroaching. Instead, it hit back and embraced its communist roots. China is too big to have a managed economy and managed trade with a managed exchange rate and to think that it will not be sending disturbing repercussions through the rest of the international system. When Mao ruled, China was isolated and its policies while isolated hardly affected anyone. But now China has some degree of openness. It trades in massive quantities with the rest of the world and yet we can have no faith that Chinese exchange rates inflation or prices bear any resemblance to true economically-determined variables. And having prices determined in a competitive framework is the bedrock of economics and of free trade. So losing this connection puts us into some nether world in terms of trade and welfare theory as we use the term in economics (to refer to the welfare of people or a nation and not to programs for the poorest).

At a time when stock markets are booming and everyone is getting happy because growth seems to have returned and manufacturing seems to have recovered and monetary policy looks like it will head back to 'normal,' it is instead the case that we are living on borrowed time. We are not taking these improved conditions as an opportunity to make right what has been wrong.

Make no mistake about it; the international trade system remains very broken. Look at the value of trade being conducted under conditions that are not aligned with free trade principles. All that means is that we still are not getting free trade results. We are spreading distortions. There is again a trend for companies to merge and to become huge to control their markets. But the economy does best with smaller firms that must compete rather than with larger firms that can control. But this our world and the control is over not just the economic system but the political system as well. In Europe, we have seen a backlash against the ruling elites, but they have been able to survive. In the U.S., the election of Donald Trump was supposed to shake the tree and drain the swamp, but there are as many alligators as ever in Washington DC. The stubborn trade positions tell the story in a succinct way. Nothing has changed. We are building excesses on top of excesses again. There is no progress, just illusion.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief