Global| Oct 29 2015

Global| Oct 29 2015EU Sentiment Falls; EMU Sentiment Rises

Summary

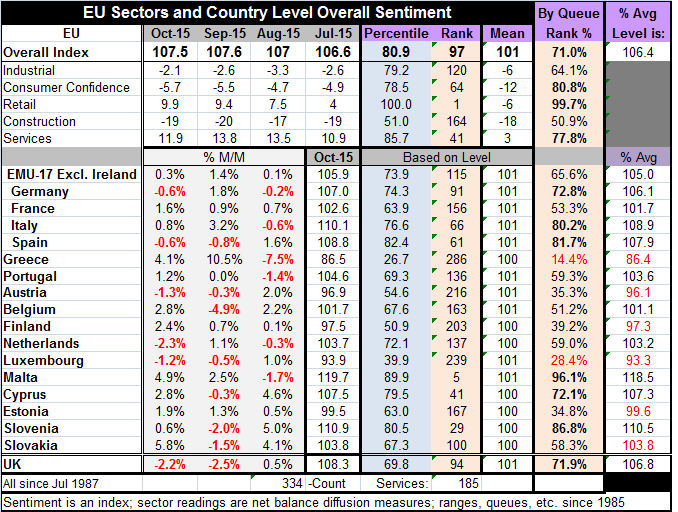

The EU and EMU indices are split this month with the EMU area improving and the broader EU index that includes EMU nations deteriorating. Still, only five of 16 EMU nations showed deteriorated indices in October. The overall EU index [...]

The EU and EMU indices are split this month with the EMU area improving and the broader EU index that includes EMU nations deteriorating. Still, only five of 16 EMU nations showed deteriorated indices in October.

The EU and EMU indices are split this month with the EMU area improving and the broader EU index that includes EMU nations deteriorating. Still, only five of 16 EMU nations showed deteriorated indices in October.

The overall EU index sits in the 71st percentile of its historic queue of data, a firm standing; the EMU index sits lower, in its 65th percentile.

In October there were improvements across three of five EU sectors. The exceptions were the services sector which took a large step back and consumer confidence which has been slipping since June. Retailing has been moving up voraciously. But its pace of ascent has slowed now that it has hit an all-time high. The services sector had been advancing steadily too until it took its setback this month.

The industry ratings in the EU are mostly firm to strong this month, but the ones that are weak are notable. Retailing is posting the highest standing it has ever seen. It is the consumer not the producer that is keeping the EMU strong, and that is unusual. Consumer confidence and services stand near the 80th percentile of their respective historic queues of data- a solid position. However, the key industrial sector sits only in its 64th percentile. Construction stands in its 50th percentile- no better than mid-range.

Challenges for the future

We have already seen evidence that the migrant crisis has begun to set back confidence in Germany. The GfK survey which looks forward to November found German confidence stepping back partly because of concerns over the impact of the influx of migrants. Angela Merkel is under fire for her acceptance and welcoming of this mass of people.

The big four EMU economies continue to post gains with only Spain having flattened out after a period in which it outperformed everyone else. However, solid momentum is still lacking.

On balance, despite the backtracking in the EU and the small gain in the EMU this month, the dynamics of growth in the EU/EMU have worked. The question we have to ask is if it is sustainable for retailing to be leading growth. Manufacturing is still well behind and with little momentum. It has been the traditional leading sector. Now, despite the rising role of retailing, consumer confidence is starting to back-off. Is that a signal that retailing is about to slow? If it does slow, what will take its place?

Perhaps the most interesting thing about the EMU right now is that the low currency makes the region highly competitive internationally. Yet, instead of being led by its manufacturing sector, it is being led by retailing with manufacturing the laggard sector along with construction. This is peculiar, but it is also an indictment of the weak state of global growth. Some of the problem is that Germany, the leading exporter in the EMU, has had its wings clipped in its Russian trade with sanctions imposed, then it found itself highly exposed to an imploding China market. But these events remain economic reality. Of course, Germany has an extra problem with its largest corporation, Volkswagen, about to be put under heavy fines for egregious cheating on environmental standards. The migrant issue will fester. Germany, the leading economy in Europe, is about to be put under an unusual matrix of stresses.

Summing up

The expression `so far, so good' is not an encouraging one in the case of Europe since risks are stepping up. Despite the relative strength in retailing, overall growth has been weak and the ECB seems to be planning to engage in more monetary stimulus. Ongoing adherence to the principles of austerity continues to keep growth in the region restrained. While this month's economic indices seem to be relatively solid, there is no strength of momentum. Italy alone among the large EMU members has upward momentum with a strong index. Germany's index fell this month; Spain's has fallen for two months in a row. The overall standing of the EMU index in its 65th queue percentile tells the real story. This is still a very sluggish reading. Europe is surviving, but it is not prospering. It is not in gear for much improvement and still to face stepped up challenges.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief