Global| Apr 30 2008

Global| Apr 30 2008EU Indices in Steady State Decline…

Summary

If they were ski runs, they’d be black diamonds. The EU sentiment index fell sharply in April with declines in all sectors and with all sector readings south of zero except services. Ironically the service sector is the weakest of the [...]

If they were ski runs, they’d be black diamonds.

The EU sentiment index fell sharply in April with declines in all sectors and with all sector readings south of zero except services. Ironically the service sector is the weakest of the lot in terms of its standing as a percentile of its range. That standing is the 31st percentile Consumer confidence is the next weakest measure in its 51st percentile followed by retailing in the 55th percentile. The industrial sector for which we get the most data is in its 73rd range percentile, the strongest of the lot. Overall the EU index is in its 57th percentile and above its average and range midpoint.

Percentiles give us an idea of the relative standing of each sector since each has a different intrinsic range and variability. Looking at percentiles helps us to see where the weakness is hitting the hardest.

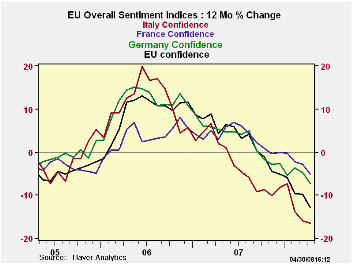

EMU is in the 54.6th percentile of its range. Within EMU among the large countries France ranks in its 67th percentile, Germany is in its 60th, Italy is in the 41st, and Spain is in the weakest of these, 27th percentile of its range.

The chart shows that the pace of the slide is as yet, unabated.

For industrial production expectations and order volumes are still firm in their respective 65th and 77th range percentiles. Among large EMU countries Germany and France are in league unto themselves as their respective 78th and 71st percentile standings are high; Italy and Spain are at lower rankings in percentile terms.

The consumer situation is best in Germany where consumer sentiment still in the 75th percentile of its range; in France confidence is down to the 50th percentile Italy’s consumer sentiment is in the 37th percentile and for Spain its the 27th percentile. For the UK the confidence measure is in its 42nd percentile.

Notwithstanding these results the French retail sector is in the 80th percentile of its range in April followed by Italy in the 75th percentile – despite a sour consumer. Germany, with the most upbeat consumer, finds retail confidence in the 40th percentile. Spain’s consumers are weak with retailing in the bottom 4 percent of its range. The UK retail sector reading fell sharply in April to -17 from -1 in March marking a 28th percentile reading in its range.

The services sector rankings show France’s service sector is in the 58th percentile, and Germany’s in the 41st percentile. For Italy the service sector is much worse off, in the bottom 6% of it range near Spain’s reading that is at an all time low reading in April. Spain’s service sector shed 6 points to drop from -8 to -14 in raw terms in one month. UK services also fell hard to -6 from +13 and to a 29 percentile ranking.

On balance the EMU and EU readings show a great deal of distress and some of it quite recent. The country by country findings are revealing. What remains curious is that amid all the concern about the strong euro the service sector is getting hit so hard. Some of that may be financial turbulence. In any event the extent of financial sector weakness is striking. It seems a good time to put Europe on a weakness watch. For the industrial sector even selling price expectations have been reduced somewhat to the 61st percentile they are not one of the stronger industrial components anymore. Does that mean that inflation is not so much of a risk?

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Apr 08 |

Mar 08 |

Feb 08 |

Jan 08 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/ Overall |

| Overall | 98.1 | 101.9 | 100.3 | 103.3 | 57.9 | 122 | 116 | 73 | 43 | 100 | 1.00 |

| Industrial | -2 | 0 | 0 | 2 | 73.5 | 64 | 7 | -27 | 34 | -7 | 0.88 |

| Consumer Confid | -12 | -11 | -11 | -10 | 51.7 | 124 | 2 | -27 | 29 | -10 | 0.83 |

| Retail | -6 | 1 | 1 | -3 | 55.6 | 100 | 6 | -21 | 27 | -6 | 0.47 |

| Construction | -11 | -9 | -7 | -4 | 68.9 | 75 | 3 | -42 | 45 | -17 | 0.43 |

| Services | 6 | 11 | 6 | 11 | 31.6 | 105 | 32 | -6 | 38 | 17 | 0.81 |

| % m/m | Apr 08 |

Based on Level | Level | ||||||||

| EMU | -2.5% | -0.6% | -1.5% | 97.1 | 54.6 | 124 | 117 | 73 | 44 | 99 | 0.95 |

| Germany | -1.2% | 0.3% | 0.6% | 102.8 | 60.0 | 85 | 119 | 79 | 40 | 99 | 0.70 |

| France | -2.4% | 0.0% | -1.3% | 103.1 | 67.1 | 97 | 119 | 72 | 47 | 100 | 0.79 |

| Italy | -1.7% | -1.3% | -3.7% | 92.1 | 41.6 | 167 | 121 | 71 | 50 | 100 | 0.78 |

| Spain | -3.8% | -4.1% | -3.4% | 80.7 | 27.2 | 193 | 118 | 67 | 51 | 100 | 0.63 |

| Memo: UK | -8.5% | 10.7% | -8.7% | 95.8 | 54.7 | 147 | 118 | 69 | 50 | 101 | 0.43 |

| Since 1990 except Services (Oct 1996): 208 | -Count | Services: | 126 | -Count | |||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief