Global| Oct 30 2014

Global| Oct 30 2014EU Indices Head Higher in October

Summary

The EU overall sentiment index rose to a level of 104 in October from 103.5 in September, an increase that was unexpected. European Monetary Union data, especially the PMI data on manufacturing and service sectors, have continued to [...]

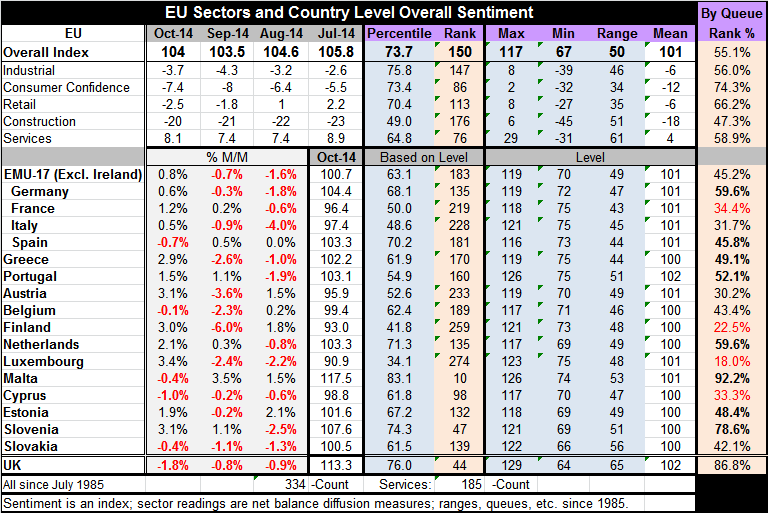

The EU overall sentiment index rose to a level of 104 in October from 103.5 in September, an increase that was unexpected. European Monetary Union data, especially the PMI data on manufacturing and service sectors, have continued to be weak.

The EU overall sentiment index rose to a level of 104 in October from 103.5 in September, an increase that was unexpected. European Monetary Union data, especially the PMI data on manufacturing and service sectors, have continued to be weak.

The five sector readings on the EU show that four of five improved in October. The industrial sector improved in October with its index reading rising to -3.7 this month from -4.3 in September. Consumer confidence also improved in October, rising to -7.4 from -8. The retail sector worsened, falling to -2.5 from -1.8. The construction sector improved, rising to -20 from -21. The services sector also improved, rising to 8.1 from 7.4. As you can see, four of five sectors improved on the month. However, the deteriorating sector was the important retail sector. A counterpoint consumer confidence did improve.

Next we turn our attention to the data for the absolute standing of these responses for the various EU sectors. The EU overall index stands in the 55th percentile of its historic queue, meaning that 45% of the values are higher and 55% of values are lower. By definition, the median for the EU index falls at a 50% queue standing. The industrial sector is at a 56 percentile reading that is marginally above its historic median. Consumer confidence is relatively more robust, in the 74th percentile. The retailing sector stands at its 66th percentile. Construction is in its 47th percentile, below its historic median. The services sector is in its 58th percentile, nearly at 59th. Readings between the 50th and 59th percentile, are still rather weak. Readings in the 60th percentile are moderate. Readings in the 70th percentile begin to get firmer. Readings in the 80th and 90th percentiles are quite firm to quite strong, but nothing is in that range.

Next we look at the specific countries and at EMU member economic sentiment gauges. For the European Monetary Union, the overall index rose by 0.8% in October after a 0.7% decline in September. The EMU reading is distinct from the EU reading; its stance is at its 45th percentile, five percentage points below its historic median. EMU countries are doing worse than the EU overall. Remember that the EU contains all of EMU countries plus some extra members. The results for October show that there was an improvement in the sentiment indices in Germany, France and Italy with only Spain among the big four EMU countries posting a decline. Germany sits in the 59th percentile of its historic queue while France sits in the low 34th percentile with Italy in the 31st percentile and Spain in its 45th percentile. Among the big four countries, only Germany is anywhere close to being moderately firm.

The production sector reading for EMU shows an improvement to -5 in October from -6 in September with most of the improvement coming in the production expectation index which moved up to a 6 reading from 5, export orders which also improved to -15 from -16 and selling price expectations which moved up to zero from -2. Other indicators were flat with employment expectations worsening to a reading of -7 from -5 in September. By country, conditions worsened in Germany, were unchanged in Spain and improved slightly in France and Italy. The queue percentile standing for industry in all of EMU is in its 54th percentile with Germany providing the strongest percentile reading at the 56.9 percentile, Spain is in its 49th percentile, France is in its 47th percentile and Italy is much lower in its 32nd percentile. There's a good deal of variability just among the big four countries. Among them only Germany is anywhere near being firm and it still falls short of that label.

The consumer confidence reading for the EMU improved slightly to -11.1 from a level of -11.4. We see some improvements in the economic situation expected over the next 12 months and in unemployment expectations as well as in the ability to save and the environment for making major purchases in the next 12 months. By country, conditions were unchanged in Germany and in France and Spain, with Italy moving lower by two points month-to-month. The queue percentile standing of consumer confidence is in its 56th percentile for all of EMU. The German percentile standing is in its 74th percentile with Spain in its 63rd percentile. Italy is in its 46th percentile and France at a very weak 25th percentile standing. Consumer confidence in France is only weaker about one quarter of the time.

Retail confidence in the EMU rose by 1 point to -6 in October from -7 in September. Those improving items included the expected business situation, and in orders placed, with the other indicators substantially unchanged on the month. By country, Germany and Spain worsened while France improved by three points month-to-month as Italy improved by one point. The queue percentile standings for retail overall in the EMU is in its 70th percentile. Germany stands firm in the 75th percentile. Spain's is even stronger (relatively) in its 96th percentile. Italy is in its 55th percentile, while France is in its 25th percentile near the bottom quarter of its historic queue.

In the EMU services sector, conditions improved in October by 1 point to 4 from 3. There were slight improvements across most categories, including current demand, expected demand, current employment, and expected employment, with the business climate being unchanged from month-to-month. By country, Germany showed an increase month-to-month along with France and Italy. Only Spain among the big four countries showed a decline in conditions; it's deteriorated by four points. The queue percentile standing for services is weak, standing only in its 44.9 percentile, below its median. For Germany, the queue standing is in its 65th percentile; for Spain, it's in its 53rd percentile; for Italy it's in its 42nd percentile; and for France, it's in its 29th percentile.

The October EMU construction indicator improved to -25 from -28 in September. There were improvements in each of the big four countries except France. There was a significant strong improvement in Spain. The construction indicator for the euro area sits in its 42nd percentile. For Germany, the reading is in its 90th percentile, extremely strong. For Spain, the indicator is in its bottom 38th percentile. For Italy, it is in its bottom 24th percentile. For France, the indicator is in its bottom 10th percentile. Once again conditions in France are extremely weak.

While the EMU readings and the EU readings for October were surprisingly up instead of lower, a detailed assessment of these sectors and member countries shows that there continues to be a great deal of weakness in the EMU as well as in the EU. The percentile standings for these indicators are for the most part no better than moderate and in many cases weak to quite weak. It's against this perspective that we are not particularly impressed about the rebound in the European indicators this month and would caution against viewing the bounce as anything that's fundamental or that will necessarily start a lasting uptrend. Europe still has a great deal of troubles and the European Central Bank has very few degrees of freedom. Fiscal policy is still in handcuffs and is being held in solitary confinement across the euro area.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief