Global| Jan 30 2017

Global| Jan 30 2017EU Commission Indices Hold Uptrends

Summary

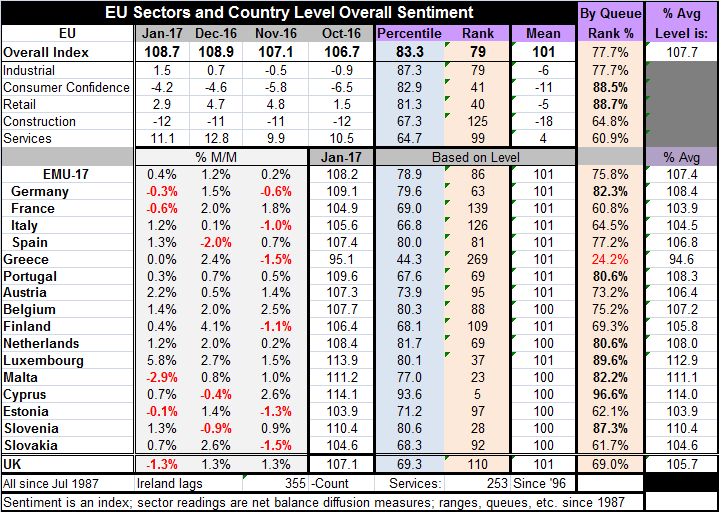

The EU area index compiled by the EU Commission fell in January while the EMU area index rose for the fourth month in a row. The EU index sits in the 77th percentile of its historic queue of values while the EMU index resides in the [...]

The EU area index compiled by the EU Commission fell in January while the EMU area index rose for the fourth month in a row. The EU index sits in the 77th percentile of its historic queue of values while the EMU index resides in the 75th percentile of its queue of values. Despite the monthly oscillations, the EMU indices are in uptrend for each of the four largest EMU economies.

The EU area index compiled by the EU Commission fell in January while the EMU area index rose for the fourth month in a row. The EU index sits in the 77th percentile of its historic queue of values while the EMU index resides in the 75th percentile of its queue of values. Despite the monthly oscillations, the EMU indices are in uptrend for each of the four largest EMU economies.

By sector, retailing and consumer confidence are the two relative strongest sectors; they have the highest queue standings in their respective upper 80th percentiles. The industrial sector has a 77th percentile standing in its historic queue for all of EU. Services and construction lag with standings in their respective 60th percentiles.

The EMU 17 nations (Ireland is a late reporter and excluded here, dropping the number of reporters to 16) show only four members with their EU sentiment index dropping in January. However, the two largest EMU economies France and Germany saw declines along with Malta and Estonia. This is up from three in December but less than the six nations that saw sentiment declines in November.

Seven of the 16 reporters in this table show standings of their EU Commission indices in the top 20% of their historic queues. Only Greece is below its 50th percentile; in fact no member in this table- as of January 2017- has a standing has low as its 60th percentile (except Greece).

Most of the EMU Commission indices show slippage since mid-2015 but have reversed that pattern in the last four to five months. Most of the sector indices are stable to stronger although momentum is tempered even when it is present. The EMU is doing better but this is no growth surge.

Inflation is starting to rise. With the economy showing somewhat firmer readings, the probabilities have begun to tilt toward the ECB removing stimulus. However, inflation is largely a manifestation of oil and growth is still not on solid footing even if it has spread and firmed somewhat. The ECB will soon find itself under enormous pressure from Germany where inflation is rising faster than it is in the EMU region as a whole and where economic readings are stronger as well. The ECB has an inflation only mandate; with oil pushing inflation up soon, ECB President Mario Draghi will be out of counter arguments against ending his special stimulus programs and will be pressured to actually hike rates. Conditions are changing in the EMU. But they are changing in such a way as to make policy decisions as difficult as possible.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief