Global| Aug 28 2020

Global| Aug 28 2020EU Commission Indexes Show Ongoing But Slowing Recovery

Summary

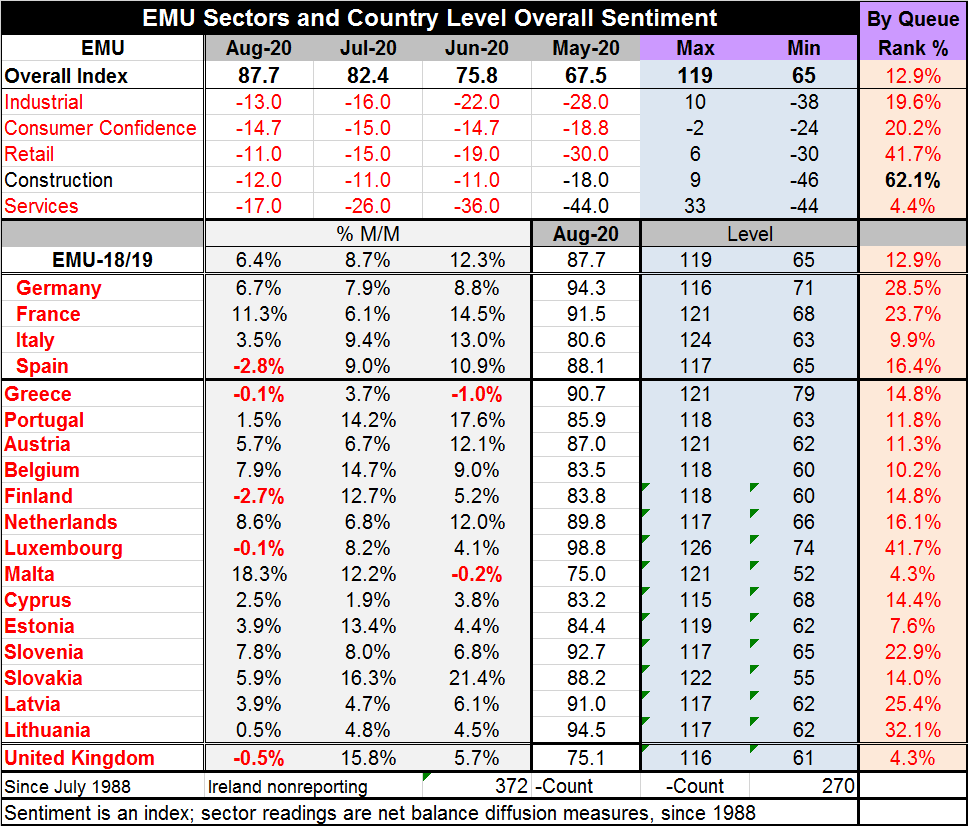

The overall EMU index shows an ongoing rebound with significant monthly gains, but as of August the queue standing of the index is at its 12.9 percentile and nearly 16 points below its February value. The index rose by 8 points in [...]

The overall EMU index shows an ongoing rebound with significant monthly gains, but as of August the queue standing of the index is at its 12.9 percentile and nearly 16 points below its February value. The index rose by 8 points in June, by 6 points in July and by 5 points in August. These all are large monthly gains, among the largest ever, but the pace of improvement is still slipping and there is a long way to go to get back to where the index was in February.

The overall EMU index shows an ongoing rebound with significant monthly gains, but as of August the queue standing of the index is at its 12.9 percentile and nearly 16 points below its February value. The index rose by 8 points in June, by 6 points in July and by 5 points in August. These all are large monthly gains, among the largest ever, but the pace of improvement is still slipping and there is a long way to go to get back to where the index was in February.

All sectors in EMU improved in August except construction

Among the 18 early reporting EMU countries, and the U.K. to make the total 19, only four EMU members plus the U.K. failed to improve in August. All of them improved in July and all but two improved in June. The gains in the indexes have been both strong and widely shared across the EMU. However, just like the overall gauge, none of the members have sentiment indexes that have been returned to strong or even firm standings. No EMU member nation has a queue standing as high as its median (50% mark). The highest readings are generally among the smallest nations such as Luxembourg (41.7%), Lithuania (32.1%) and Latvia (25.4%). Germany and France manage standings of 28.5% and 23.7%, respectively. All of these are still extremely weak readings despite their being among the best the area has to show.

The sector readings are weak too with construction in the EMU the strongest sector of the lot. Retailing has a 41.7 percentile standing. After the industrial sector and consumer confidence has standing in the lower 20th percentile and the all-important jobs-production service sector saw a very weak 4.4 percentile standing. Construction alone has a standing above its median at its 62nd percentile and its employment impact is miniscule.

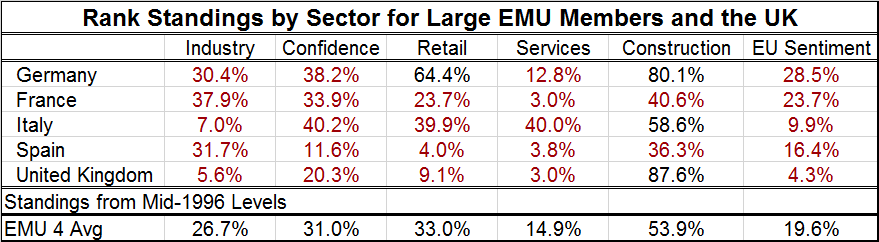

The table below gives queue standing assessments by sector for the four largest EMU members plus the U.K. Among the five sectors and five countries, there are 25 sector assessments of which only four have standings above their respective historic medians. Three of those above-median assessments are in the construction sector; one is for retailing in Germany.

The EU sentiment reading for each country is also listed in the table. It shows that the two largest EMU economies Germany and France also have the two strongest readings. The next two largest, France and Spain, are much weaker. The U.K., no longer with any EU affiliation, has the weakest standing. The EU indexes are a weighted average of the sector indexes in the table. Nothing anywhere in this table or in the broader country table is really strong. Momentum seems to be fading. The virus continues to spread and cause new shutdowns or measures to be implemented. France has just adopted a policy of mandatory mask-wearing in Paris. Angela Merkel has just issued a warning that the virus impact would drag on warning that even if a vaccine were successful, producing and administering it would still take a substantial amount of time.

The outlook has to continue to be one of extreme uncertainty. There are hopes, plans, and even forward purchases of expected vaccines. But no one knows if the vaccines being developed will pass muster. There are all sorts of divisions among people including policymakers on how to handle this. The recent flare up of virus in countries that thought they were on the downslope of their troubles is a stark warning for the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief