Global| Jan 28 2016

Global| Jan 28 2016EU and EMU Indices Hit 5-Month Low As Momentum Erodes

Summary

The comprehensive EU sentiment index and its counterpart for the EMU fell and each index fell to a five-month low in January. Happy New Year! The indices are out relatively late in the month, allowing for the month's activities to be [...]

The comprehensive EU sentiment index and its counterpart for the EMU fell and each index fell to a five-month low in January. Happy New Year! The indices are out relatively late in the month, allowing for the month's activities to be more fully reflected including economic data and the ongoing market selloff. Previously, we saw the Germany's Ifo index fall and reverse a less worrisome signal from the ZEW index. Contrarily, country-level consumer confidence indices have remained solid to date. In the EU framework, however, we see consumer confidence falling by more in January and the counterpart measure for the EMU reaches its weakest value since October with this month's drop. Maybe the other shoe is starting to fall?

The comprehensive EU sentiment index and its counterpart for the EMU fell and each index fell to a five-month low in January. Happy New Year! The indices are out relatively late in the month, allowing for the month's activities to be more fully reflected including economic data and the ongoing market selloff. Previously, we saw the Germany's Ifo index fall and reverse a less worrisome signal from the ZEW index. Contrarily, country-level consumer confidence indices have remained solid to date. In the EU framework, however, we see consumer confidence falling by more in January and the counterpart measure for the EMU reaches its weakest value since October with this month's drop. Maybe the other shoe is starting to fall?

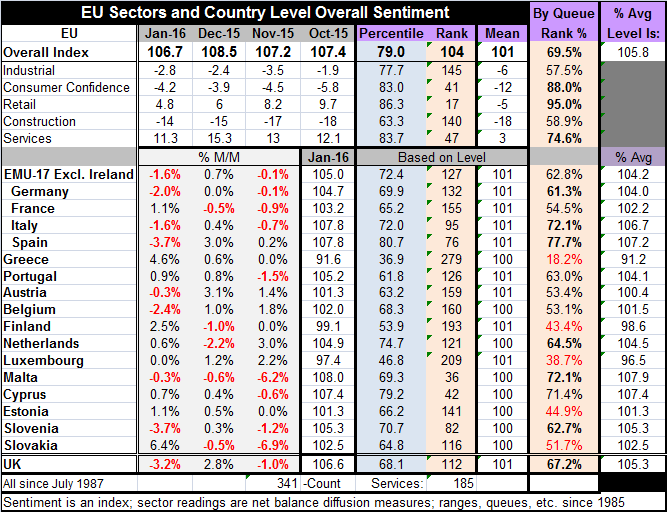

Besides a drop in the overall indicator and a setback to confidence in January, retailing continues to lose momentum as it continues to drop and has fallen for three straight months, more than halving its peak reading for October. The industrial sector continues to post negative numbers, slipping further to -2.8 this month from -2.4 in December. The services sector reading took a sharp turn lower, falling to 11.3 from December's 15.3. The reading of 15.3 was this cycle's high and the highest reading since October 2007. The drop to 11.3 brings the index back to its lowest reading since April 2015. The services sector tends to be the job sector. A setback here could pave the way for further weakness in consumer confidence as it would likely mean a less robust job market. The sharp four-point drop in the services index is the ninth largest one month drop in the last 14 years. The setback is substantial for this key sector. The construction sector, also having continued to post negative readings, showed a one-point improvement to -14 in January.

Levels and momentum.a grim result on momentum

We can assess these indices by their historic standing in their ranked data. The industrial and construction sectors are the weakest as each located in its 57th or 58th percentile of its respective historic queue of data. The overall EU metric stands in its 69th queue percentile. Services now stand in their 74th percentile with both consumer confidence (88th percentile) and retailing (95th percentile) higher. Confidence and retailing are still in very strong positions. However, momentum viewed over 12 months, is slipping. The overall index is net lower by 2.5 points and only the construction sector index is higher on this basis. The EU indices clearly are on a path lower and no longer are gaining momentum. All indicators except construction are net lower over 12 months, six months, and three months with the exception of consumer confidence which is still net higher over six months; it remains lower over 12 months and three months.

Trends in the four largest economies

The factory sector shows negative readings overall and for each of four largest economies. Moreover, each of the Big Four economies also shows either unchanged conditions (France) or worsened conditions over the last four months. For consumer confidence, the results are more mixed. Confidence readings still are net negative for each of the Big Four EMU economies (Germany, France, Italy and Spain) except in Italy where the reading climbed to zero in January. Germany is net weaker over four months and Spain is unchanged as both Italy and France have showed some confidence improvement. Retailing still has positive readings across the Big Four economies with France as an exception. Since October, each Big Four economy has a weaker retail sector except Spain. However, Italy, France and Germany each show substantial slippage. The services sector which slipped so badly for the EU overall is net lower in each of the four largest EMU economies over four months except Spain. There the reading is only flat. Construction shows negative readings in each of the largest four economies. But it is net lower compared to October only in Italy and in Spain.

Sum-up

On balance, the EU indices seem to be making a watershed move to weaker values and to be establishing a weaker trend, too. The Big Four EMU economies generally are showing slippage in their main indicators over the last four months. The strength in services took an outsized step backward in January. Migrant issues continue to dog Europe and the ongoing stock market crash cannot be good for growth as it has destroyed so much wealth. Europe is a net oil importer. Lower energy prices are still an aid to this region. But there are a lot of negatives and some the key stalwarts like the firmness in services giving way this month - that is an unambiguously bad sign. The ECB has been talking about doing more. It now may have put itself behind the eight-ball, having waited too long to pull the trigger on more stimulus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief