Global| Mar 01 2018

Global| Mar 01 2018EMU Unemployment Rates

Summary

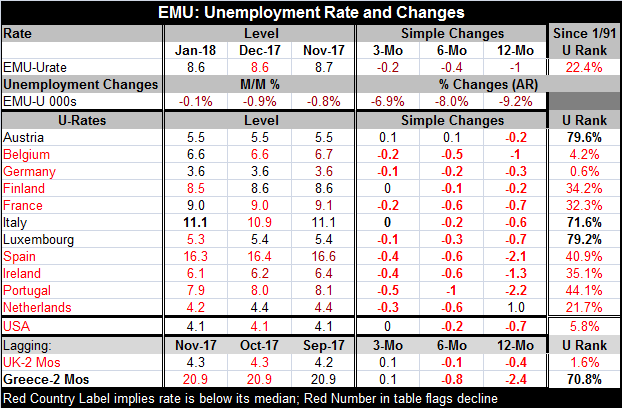

Unemployment rates continues to fall in the EMU. The EMU rate itself is at 8.6% in January and in December 2017 which was revised lower. The EMU wide unemployment rate is the lowest since December 2008. Of the eleven original EMU [...]

Unemployment rates continues to fall in the EMU. The EMU rate itself is at 8.6% in January and in December 2017 which was revised lower. The EMU wide unemployment rate is the lowest since December 2008.

Unemployment rates continues to fall in the EMU. The EMU rate itself is at 8.6% in January and in December 2017 which was revised lower. The EMU wide unemployment rate is the lowest since December 2008.

Of the eleven original EMU members that have reported unemployment rates topically in January 2018, six of them are lower, four of them are unchanged, and for one, Italy, the unemployment rate has risen relatively significantly. Over three months, unemployment rates are lower in eight of eleven countries, unchanged in two of them, and higher in one, Austria. Over six months, unemployment is lower in ten of eleven countries with Austria again the exception. Over 12 months, unemployment rates are lower in ten of eleven countries with the Netherlands as an exception and an unemployment rate that is higher by 1 full percentage point over 12 months.

For the EMU, the unemployment rate has been this low or lower (than its 8.6% level) only 22.4 % of the time since January 1991. However, only Germany (0.6%), Belgium (4.2%) and the Netherlands (21.7%) have their respective unemployment rates lower than their January levels less frequently than the EMU mark.

The very low German unemployment reading and the high weight of the German labor market are driving the result for the EMU as a whole. The average of all other January reporters is a 44.3 percentile standing, nearly twice the standing for the WEIGHTED EMU average. Austria, Italy and tiny Luxembourg are countries with their respective unemployment rates in the upper 30th percentile (that is also above a 70th queue percentile standing as presented in the table above). It means that their unemployment rate has been higher less than 30% of the time.

Greece, that reports late, has a queue percentile standing for its unemployment rate in its 70.8 percentile. The U.K., an EU member (still), has a very low 1.6 percentile standing in its (lagging) unemployment rate.

By comparison, the U.S. has seen its unemployment rate flat-line over the last three months and has a low 5.8 percentile standing, a slightly higher percentile standing than for Germany.

These statistics underscore the ongoing improvements in the international job market. Levels of employment are improving. Levels of unemployment are generally lower and falling. However, while the German unemployment rate is very low, it does not generally represent the condition across the rest of the EMU. It does, however, contribute to making the EMU overall situation look better. While the weighted approach to understanding EMU data is certainly the best approach, it is also important to understand the degree of difference or variation that exists among members when the ECB is making its policy. Currently, the standard deviation among EMU members has a 45th percentile standing, slightly below its historic median (the median occurs at the 50th percentile). The job of the ECB to make policy continues to be challenged because the largest economy in the EMU is in such a different economic position from the rest of the EMU and there is no way for the ECB to make a policy that is going to be optimal for Germany and optimal for the rest of the EMU at the same time. Until such time as the German economy better integrates with the rest of EMU and run policies that put its economy more in line with the rest of the EMU, the ECB will continue to be given a task --to make one policy for such a disconnected zone -- that is impossible to execute effectively.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief