Global| Aug 31 2017

Global| Aug 31 2017EMU Unemployment Rate Steadies Employment Growth Rates in U.S., Germany and EMU Converge

Summary

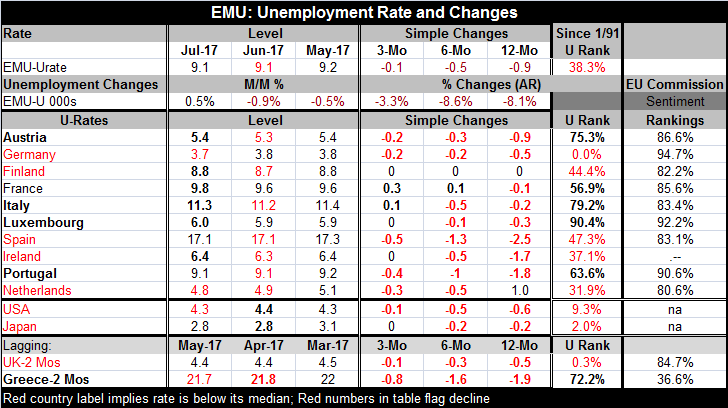

Unemployment in the EMU area was unchanged at 9.1% in July. However, the number unemployed rose by 0.5%, a sharp difference from June's 0.9% decline. Still, unemployment rates are unaffected for the region as a whole. But 10 of the [...]

Unemployment in the EMU area was unchanged at 9.1% in July. However, the number unemployed rose by 0.5%, a sharp difference from June's 0.9% decline. Still, unemployment rates are unaffected for the region as a whole.

Unemployment in the EMU area was unchanged at 9.1% in July. However, the number unemployed rose by 0.5%, a sharp difference from June's 0.9% decline. Still, unemployment rates are unaffected for the region as a whole.

But 10 of the original members report data in July and of them only two show unemployment rate declines in July while six show increases. This contrasts sharply with June when seven nations showed unemployment rate declines and none showed increases.

Over three months, only two countries France and Italy show unemployment rate increases. France also shows a net rise over six months. Finland, Luxembourg and Ireland show no net changes in their respective rates of unemployment over three months. But declines are reported in Austria, Germany Spain, Portugal and the Netherlands. Declines on all three horizons are reported in Portugal, Spain, Germany and Austria - a rare example of two Southern European countries being on the same economic page with two hard-core EMU countries.

Unemployment rates are below their medians since early 1991 in Germany, Finland, Spain, Ireland, and the Netherlands. Above median unemployment rates continue in this recovery period in Luxembourg, Italy, Austria, Portugal, and France. That's five countries above their medians and five below.

Following up on the calculations, I presented yesterday using the EU Commission index (for August) I present the new unemployment rates for the EMU in July and add a column to the table for the ranking of each country (where possible and applicable) on the August EU Commission sentiment gauge.

In comparing the two gauges, I rank them each on a high to low scale so matching results occur when low unemployment rate standing correlates with a high EU Commission index ranking (or vice versa) such as with Germany that ranks as 0% on the unemployment scale (an all-time low) vs. a 94.7 percentile rank on the EU Commission scale. But Germany is a rare match. If I re-rank the unemployment rate so they are ranked low-to-high, the rank correlation between the two gauges is in the neighborhood of 5% - very low. This ranking of these countries by the 'strength of the labor markets' vs. ranking by their EU Commission rankings produces very different results. In Europe, the EU Commission indexes show conditions to be much better than do unemployment rate rankings. The EU Commission results are strong. The unemployment data show progress but still are not adequate.

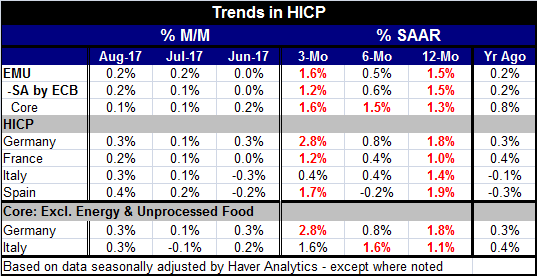

New inflation data (preliminary) show inflation is creeping up. The core is moving very slowly and is at only 1.3% (y/y) as it gained just 0.1% in August. The headline for now is slightly ahead of that at a 1.5% year-over-year pace and now we have oil prices moving again with oil and product prices split with effects from U.S. hurricane Harvey wreaking havoc on the global oil market. Oil has a very strong correlation with inflation especially with headline inflation and there is at least some risk that the oil impact on prices will be misread as actual inflation or at least used as an excuse. Central bankers with the baggage of ideology are no better than politicians with their own partisan agendas. So we are now at risk to events.

From the ECB's perspective, none of this is much help and chaos from oil prices may even do harm. EU Commission data-watchers will point to strength and call for the ECB to begin to unwind stimulus. Some may even point to rising inflation and try to downplay the oil role there. Meanwhile, half the EMU members have unemployment rates above their medians since early 1991. For all of the EMU, the gauge resides at its 38th percentile (well below its median) because the large economies- weighted heavily to Germany- are doing so well. Among the four largest economies, only Italy is doing really poorly with its unemployment rate. France has a 57th percentile standing of its rate, slightly above its median compared to Italy with a much higher 79th percentile standing. Both Spain and Germany are below their respective medians. The stage is set for disagreement.

But since we have seen that confidence measures in Europe are still relatively and uniformly high tensions over a coming ECB policy shift may not be as divisive as in the past. There may be a political will for the ECB to go ahead soon and do what it must do eventually, unwind stimulus. Today's inflation data for the EMU are a non-factor, but the tailwind from oil - at least from oil products- is now blowing more strongly. But since Draghi has been taking measured steps, when he finally shifts his position, he may have demonstrated the kind of forbearance and discipline that commands attention and compliance. The populist divisive voices in Europe have been quieted by the consistent noncontroversial election results and losses at the polls by extremists. That should actually help monetary policy to get on with the job at hand. It's one less thing to worry about.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief