Global| Oct 30 2015

Global| Oct 30 2015EMU Unemployment Rate Falls/Inflation Goes Dead Flat; No Phillips Curves Need Apply

Summary

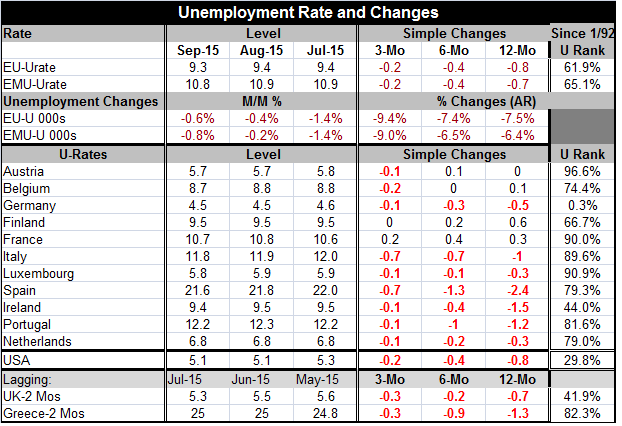

The unemployment rate ticked lower in both the EU and the EMU in September. EMU area unemployment now stands at 10.8% with EU unemployment at 9.3%. Both are still high and in the neighborhood of where U.S. unemployment would be today [...]

The unemployment rate ticked lower in both the EU and the EMU in September. EMU area unemployment now stands at 10.8% with EU unemployment at 9.3%. Both are still high and in the neighborhood of where U.S. unemployment would be today had the labor force participation rate not fallen so much.

The unemployment rate ticked lower in both the EU and the EMU in September. EMU area unemployment now stands at 10.8% with EU unemployment at 9.3%. Both are still high and in the neighborhood of where U.S. unemployment would be today had the labor force participation rate not fallen so much.

Of the 11 original EMU members in the table, the unemployment rate fell in September in seven of them. Over three months, the unemployment rate is lower in 11 of them; over six months, seven have a net drop in unemployment, the same as over 12 months.

The U.S. and the EU are showing the save pace of drop in the unemployment rate of three months, six months and 12 months. The EMU drop is slightly less over 12 months.

However, in terms of the level of unemployment, there is a huge difference between the U.S. and the EMU. The U.S. rate has been lower less than one-third of the time while the EMU rate has been lower about 60% of the time; it has been higher only about 40% of the time. German unemployment is relatively (and absolutely!) lower than everyone with a rate of 4.5% and a percentile standing in the bottom 0.3% of its historic queue. Unemployment at 4.5% is the lowest rate on record for Germany over this period back to January 1990.

Ireland's unemployment rate is in its 44th queue percentile on this period. Finland is in its 66th percentile. Belgium is in its 74th percentile. The Netherlands is in its 79th percentile along with Spain. Portugal stands in its 81st percentile. After Italy's 89th percentile standing, France, Luxembourg, and Austria all have standings in the 90th percentile or higher. Clearly unemployment rates are high by each country's historic standards everywhere except Germany and perhaps Ireland.

Unemployment has been falling and inflation is falling too. This is the opposite of what the Phillips curve relationship predicts. Falling unemployment is supposed to be associated in the short run with rising inflation. That is not true in Europe or in the U.S. The EMU HICP has gone dead flat, putting more pressure on the ECB to take additional steps of stimulus.

The improvement in the European unemployment rate is a good thing. However, as you can see, that rate is still very high. The low inflation is not just a problem for central banks with inflation targets, but it smacks of weak growth and possibly deflation. Just today the Bank of Japan has announced that it will not be able to get inflation to its 2% target until mid-year next year, and, frankly, even that sounds like a very ambitious objective.

The bottom line is that global growth is still weak. Grudging progress is being made in the reduction of what is still very high unemployment. But renewed inflation weakness is an issue and there are signs in both the U.S. and Europe of new encroaching economic weakness. Even though the Fed is no longer fixed on events overseas, weakness there from China, to Japan, to the developing world, will not leave the U.S. or Europe unscathed. Central banks can try to ignore it, but global weakness is an added burden.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief