Global| Jul 31 2015

Global| Jul 31 2015EMU Unemployment Is Unchanged; There's Germany; Then There's Everyone Else

Summary

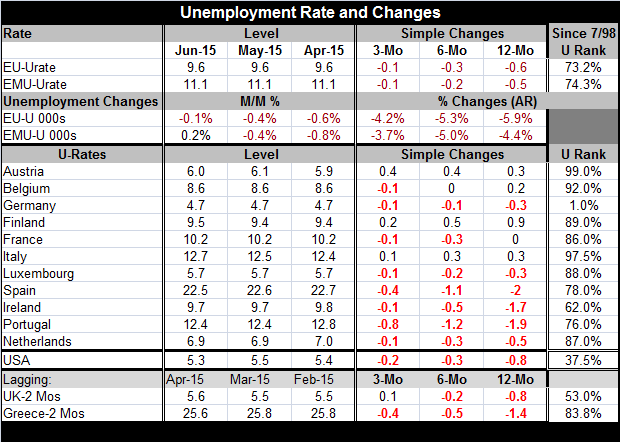

he EU unemployment rate is unchanged in June at 9.6%. The EMU rate is at 11.1%, also unchanged from the previous month. The unemployment rate is still falling in both the EU and the EMU over three months, six months and 12 months. But [...]

he EU unemployment rate is unchanged in June at 9.6%. The EMU rate is at 11.1%, also unchanged from the previous month.

he EU unemployment rate is unchanged in June at 9.6%. The EMU rate is at 11.1%, also unchanged from the previous month.

The unemployment rate is still falling in both the EU and the EMU over three months, six months and 12 months. But the pace of decline has slowed. Unemployment is lower by just 0.1% over three months in both the EU and the EMU.

For the EMU members in the table, unemployment is lower in only two countries, Austria and Spain. Unemployment rose in Finland and Italy to counterbalance that.

However, over broader periods, the country-level data agree with the overall EMU trends; unemployment rates are still falling. While the EMU-wide unemployment drop was small, only 0.1% over three months, the breadth of that drop was very widespread. Unemployment fell in 8 of 11 countries in the table. Over six months, unemployment rates fell in seven of 11 countries. Over 12 months, unemployment rates fell in six of 11 countries. While the amount of the unemployment decline has been withering, the breadth of the decline has been spreading.

Still, unemployment conditions in the euro area show the same old, same old, circumstances. Unemployment rates are in their top 10% (90th percentile) in three countries. They are in their top 20% (80th percentile) in another four members. One member has unemployment in its 70th percentile and one in its 60th percentile. Only Germany has unemployment in single digits, and there it is in its lowest one percentile.

Unemployment is low in Germany and is high-quite high just about everywhere else in the euro area. Germany continues to run a huge current account surplus and is shooting for a raw fiscal surplus at a time the rest of the euro area is struggling. Germany is disobeying EMU rules by not ridding itself of its excessive current account surplus. If it did take action to reduce the surplus, it could increase domestic demand to help the rest of euro area members who would have a chance to satisfy that demand. Instead, Germany is running polices it deems best for Germany and flaunts EMU rules on balance of payments excesses. Meanwhile, it demands that Greece to obey the rules. Germany is benefitting from the ills in other nations as their problems drag the euro to a weaker level and improve German competitiveness in the global economy. Reticence and intransigence never worked out so as they have for Germany.

The chart shows very clearly that Germany has blossomed in the financial crisis and its aftermath The German unemployment rate was higher than the EMU average prior to 2008; it is now substantially lower. Germany is doing bupkis to help the rest of the euro area perform better. It sole role is that of an inflexible task master and possibly of a lender should Greece eventually drink das Kool Aid.

Mexican standoff crosses the Atlantic

However, the possibility of German participation in a Greek bailout has been turned on its head. Germany has said it would find it hard to lend to Greece without IMF participation. The IMF has said it will not lend to Greece unless the Greek debt load is sustainable. Germany has also been refusing any debt deal with Greece. And for its part Greece has refused to give in to any more of its creditors demands. This is the very definition of a Mexican standoff: three hombres, in a circle, each pointing a gun at the guy next to them. The Greek debt negotiations have hit a real difficult spot with three of the main participants refusing to go ahead until each one of the others does something it has sworn that it would not do. Interesting, isn't it? Carumba!

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief