Global| May 31 2017

Global| May 31 2017EMU Unemployment Continues to Fall Lowest in Eight Years

Summary

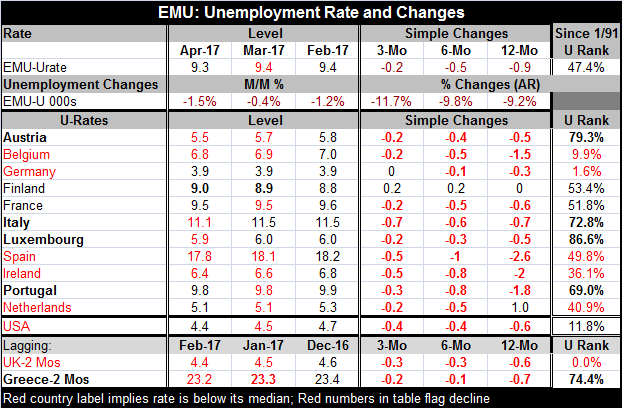

The lowest unemployment rate in eight years is an accomplishment for the EMU. But of the 11 original members whose data are arrayed in the top of the table, only five have unemployment rates below their respective medians since 1991. [...]

The lowest unemployment rate in eight years is an accomplishment for the EMU. But of the 11 original members whose data are arrayed in the top of the table, only five have unemployment rates below their respective medians since 1991. They are Germany (whose rate just hit a new post-reunification low), Belgium, Spain, Ireland, and the Netherlands. Finland and France are close to that benchmark with queue rankings in their respective low 50th percentiles. But four countries are quite far from making true progress; they are Austria, Italy, Luxembourg, and Portugal. For them, unemployment rates have been higher less that 30% of the time.

The lowest unemployment rate in eight years is an accomplishment for the EMU. But of the 11 original members whose data are arrayed in the top of the table, only five have unemployment rates below their respective medians since 1991. They are Germany (whose rate just hit a new post-reunification low), Belgium, Spain, Ireland, and the Netherlands. Finland and France are close to that benchmark with queue rankings in their respective low 50th percentiles. But four countries are quite far from making true progress; they are Austria, Italy, Luxembourg, and Portugal. For them, unemployment rates have been higher less that 30% of the time.

The verbal war over what ECB policy should be was re-engaged this week as Mario Draghi surprised some with his assertion that despite progress in the EMU low rates and stimulative monetary policy were still needed. Today the preliminary inflation data showed that EMU inflation moved lower in May; the headline price gauge shows a 12-month gain of just 1.4%, below its target of 'just under 2%.' Core inflation is up by just 1%. In Germany, headline and core inflation each fell by 0.3% month-to-month. The German HICP is up by 1.3% year-on-year and its core rate is up by 1.3% as well. It would appear that simply on inflation terms alone Draghi's judgement is being vindicated.

Turning back to unemployment, certainly the euro area would want to make better progress on unemployment than this. The EMU-wide rate is below its median, but barely at a 47.4% queue standing. And while Italy is one of the large economies making progress, it is doing so with great difficulty. Still, Italy surprised us with an outsized drop in its unemployment rate (still the second highest among the group of original members).

Finland, France, Italy, Portugal, and Spain all have unemployment rates of 9% or more. Obviously, there is still a long way to go. Against this background, the Draghi analysis seems to be spot on. In the U.S., policy is involved in its second year of ambitious tightening goals. In 2015, the Fed began its tightening and followed with a plan for four rate hikes calling it moderate. But in fact, the Fed was not able to hike rates against until end-2016. Now in 2017, the Fed has managed to follow the 2016 rate hike with more. But the plan to continue is now in some jeopardy. Draghi is learning from these sorts of setbacks. The U.S. is not the only place where tightening moves or plans have been made and have had to be scaled back. The Fed may yet be able stay the course, but as of now the path to more hikes is not clear. Inflation has stopped rising in the U.S. and globally. OPEC's plans are still unresolved and at the moment unsuccessful. The path to growth is still challenging. The coming months will tell if the U.S. economy is up to it or not. Meanwhile, Europe has made some very solid, if hard won, gains and Draghi seems determined that the small amount of momentum it has achieved is not squandered. He is taking nothing for granted. That seems quite smart in cycle. In the 'new normal,' nothing can be taken for granted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief