Global| Sep 15 2017

Global| Sep 15 2017EMU Trade Trends Cool; EMU Surplus Recedes

Summary

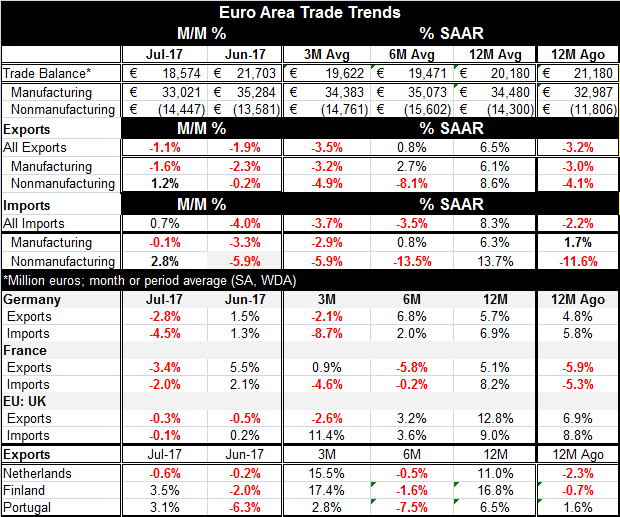

Despite its herky-jerky behavior, the EMU trade surplus is clearly in a declining phase. The surplus is at 18.6 billion euros in July, down from 21.7 billion euros in June and well below its 2016 average of 22.1 billion euros per [...]

Despite its herky-jerky behavior, the EMU trade surplus is clearly in a declining phase. The surplus is at 18.6 billion euros in July, down from 21.7 billion euros in June and well below its 2016 average of 22.1 billion euros per month. The broad euro exchange rate, trade weighted and expressed in real terms, has move up sharply and as a result EMU nations are losing some of their competitiveness (See Chart to right: values below 100 show a real effective exchange rate below parity; values above 100 show an exchange rate above parity). While European PMI data for manufacturing have been improving, the rest of the world is not improving as fast on that basis and recent economic data from China on retail sales and industrial output were weaker than expected. The new trade data in the EMU report show a weakening of export and import flows. Perhaps the belief that global growth and trade were on a roll has been exaggerated? It seems so judging from recent data trends. In addition, there will be some weakened trends for the U.S. as monthly reports register the negative impact of hurricanes that decimated broad and important economic regions of the U.S. in late August and in September. On balance, we are left to reassess where we stand.

The EMU in July shows a smaller trade surplus overall as well as a smaller surplus in manufacturing trade and a larger deficit in the trade of on manufactures trade.

Both exports and imports are weakening. Exports are lower in each of the last two months; imports are lower in June and make a small rebound in July. Contributing to that trend, the exports of manufactures are lower for two months in a row as are the imports of manufactures. Nonmanufactured exports and imports both show a drop in June and a gain in July.

However, trade trends are clear. All of these export and import categories show net declines over three months. Nonmanufactures of exports and imports also show net declines over six months. Despite that, all these flows show increases over 12 months. And over 12 months, nonmanufacturing imports and exports each are growing faster than their respective manufacturing flow. That gives us a good basis to think that oil price movements have a lot to do with the nonmanufactures trade patterns but beyond that the trade trends for manufactures are slipping too, on both the export side and import side. On balance, these are not good results for countries that are heavily dependent on trade.

Country level patterns

Germany, France and the U.K. each report July drops in both exports and imports. Germany and the U.K. also show three-month declines in exports; Germany and France show three-month declines in imports. The more stable year-on-year trends still show advances in exports and imports. Both France and Germany show exports growing slower than imports on that horizon whereas for the U.K. export growth exceeds import growth on this period. The pound sterling underwent a substantial drop that is likely helping U.K. exports to perform better.

The Netherlands, Finland and Portugal also are relatively early reporters; they show ragged patterns in their export flows. Two of three of these nations show exports higher in July while all three post export declines in June. All three show three-month export gains, six-month drops and 12-month expansions. All but Portugal are showing positive export growth over 12 months after exports declined over the previous year; Portugal is showing gains for the second 12-month period in a row.

France and Germany as EMU members show very similar patterns but the smaller countries of the Netherlands, Finland and Portugal also are EMU members and show quite different patterns. On balance, it does not seem that EMU-wide effects are mostly driving trade and that leaves the exchange rate out of the equation for now.

The ECB's dilemma

Still, the rising euro eventually will take a toll on trade as it is undercutting European competiveness. And as the ECB moves to raise rates, we can expect that the exchange rate effect will intensify. The ECB is aware of this effect and it is a fly in the ointment for ECB policy, but in the end there is nothing that the ECB can do if it is to make policy according to its directive. It will not be able to modify policy for the sake of the euro. It might modify the speed of its policy changes, but that is the outer-limit of its reach.

Summing up

For now we see that the EMU trade surplus is finally being redressed. We find the euro exchange rate is moving toward parity and rising in value. We see trade trends across EMU slowing. In the wake of recent economic data, all this should make us wonder about the state of global growth and if it has rebounded all that it is going to... and even, if it will now settle back and slow or if there is still an ongoing revival in place that will continue as many had been expecting.

Putting the 'Gee' in Geopolitics As we ponder those shifts, we have to admit that geopolitics put an ugly overview on all of this. Russia has large war games in play which it purposely placed in the Baltic region a sensitive geographical region for NATO. The U.S. and Russia are playing a tit-for-tat game of reducing one-anothers' allowed diplomatic missions on their home soil. North Korea continues to be a rogue state. With the UN having adopted some new sanctions on it, North Korea responded last night by shooting another missile in a high orbit over the Japanese Island of Hokkaido. The UN will meet again. Next time it might issue the same statement; this time typed in all CAPITAL LETTERS! That will show 'em who's boss. Syria is still a mess and the U.S. has been tinkering with its policy in Afghanistan. The geopolitical background is difficult and China and Russia are not making dealing with North Korea any easier. U.S.-China relations have been strained as the U.S. has pressured China to do more to contain and control North Korea at the same that the U.S. is opposing China's South China Sea grab. There is an old expression that the enemy of my enemy is my friend. But as you can see, in global politics our opponent in one area may be one whose cooperation we seek in another area. And that vastly affects political strategies and options. At the same time, the U.S. is trying to engage in various trade reform ideas that affect many U.S. allies and trade partners. The global situation is sticky to say the least. And the underlying economic situation may not be as strong as we had been assuming. That could cause policy-making to be even more difficult in the months to come.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief