Global| Jan 15 2010

Global| Jan 15 2010EMU Trade Surplus Shrinks

Summary

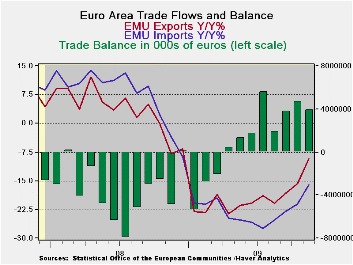

Exports in the Euro-Area faltered and fell in November, dropping for the second month in a row. Even so over three months export growth is at a strong 16.8% pace and is steadily accelerating. Imports are at a three month annual rate [...]

Exports in the Euro-Area faltered and fell in November, dropping for the second month in a row. Even so over three months export growth is at a strong 16.8% pace and is steadily accelerating. Imports are at a three month annual rate of 8.5% and also are accelerating. Despite the relatively better export performance since exports have dropped for two months running there is concern about export prospects. With the drop in exports this month as imports advanced the e-Zone trade surplus naturally receded.

Globally export volume trends are still tuning higher and the pace appears to be accelerating. In the e-Zone Germany’s Yr/Yr export volume performance improved marked between October and November, improving from a Yr/Yr growth rate of -14% to -3%. The UK (an EU country) and Japan also made substantial improvements in that period. US trade made its surge earlier, from August to September.

But for the Zone as a whole exports are not so clearly on better footing even though they are improving on trend. It could be that the Zone countries are simply improving at different speeds and that prevents the overall assessment from improving as rapidly as in the individual large G-10 countries where exports appear to be doing much better.

The trends continue to favor positive appraisals of e-Zone trade but the last two months’ exports have raised some concerns.

| Euro-Area TradeTrends For Goods | |||||

|---|---|---|---|---|---|

| m/m% | % Saar | ||||

| Nov-09 | Oct-09 | 3M | 6M | 12M | |

| Balance* | € 3,926 | € 4,726 | € 4,142 | € 3,610 | € 1,098 |

| Exports | |||||

| All Exp | -0.4% | -0.1% | 16.8% | 10.8% | -9.3% |

| Food and Drinks | -- | -1.8% | -1.9% | -5.9% | -13.4% |

| Raw materials | -- | 4.0% | 29.7% | 17.2% | -6.3% |

| MFG | -- | 1.7% | 24.2% | 6.5% | -16.3% |

| IMPORTS | |||||

| All IMP | 0.3% | -1.0% | 8.5% | 5.7% | -16.1% |

| Food and Drinks | -- | -5.3% | -16.4% | -14.2% | -11.8% |

| Raw materials | -- | 1.5% | 82.1% | 12.9% | -32.9% |

| MFG | -- | -1.6% | -3.0% | -4.6% | -18.2% |

| *Eur mlns; mo or period average; Gray shaded areas lag one month | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief