Global| Jun 15 2017

Global| Jun 15 2017EMU Trade Surplus Is Getting Erratically Lower As Trade Flows Slow

Summary

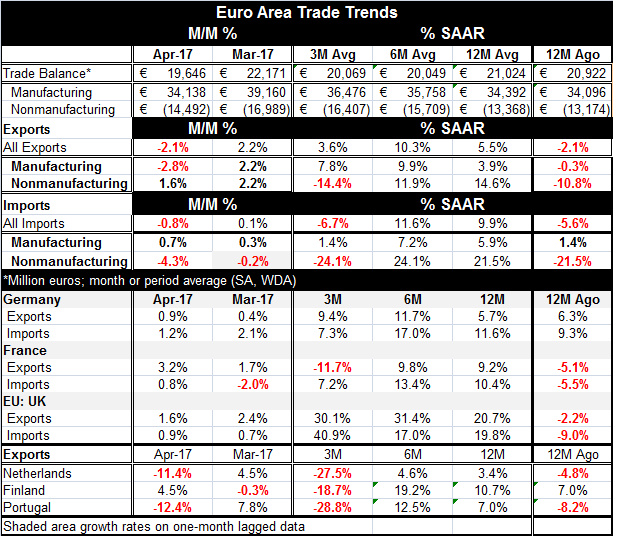

The EMU trade surplus contracted significantly in April to 19.6 billion euros from 22.2 billion euros. Still, the year-over-year shrinkage is small. The balance of trade for the manufactured goods surplus fell by 5 billion euros [...]

The EMU trade surplus contracted significantly in April to 19.6 billion euros from 22.2 billion euros. Still, the year-over-year shrinkage is small. The balance of trade for the manufactured goods surplus fell by 5 billion euros month-to-month while for nonmanufactures the deficit was reduced by 2.5 billion euros. Manufacturing trade saw a worsened balance while nonmanufacturing trade saw an improved performance.

The EMU trade surplus contracted significantly in April to 19.6 billion euros from 22.2 billion euros. Still, the year-over-year shrinkage is small. The balance of trade for the manufactured goods surplus fell by 5 billion euros month-to-month while for nonmanufactures the deficit was reduced by 2.5 billion euros. Manufacturing trade saw a worsened balance while nonmanufacturing trade saw an improved performance.

EMU-wide exports and imports both fell in April with exports falling by 2.1% as imports fell by 0.8%.

There are no clear sequential trends for exports, but three-month annualized growth at 3.6% is weaker than 12-month growth at 5.5%. For imports, the same is true, but imports are actually falling at a 6.7% pace over three months while they are up by 9.9% over 12 months.

For manufactured goods, exports hold up better with a 3.9% gain over 12 months compared to an annualized rise of 7.8% over three months. Imports weaken on that same timeline but not uniformly. Still, manufactured goods import growth is only at a 1.4% annual rate over three months compared with 5.9% over 12 months.

For nonmanufactures, both exports and imports show no clear trend, but three-month growth rates are contracting sharply compared to 12-month; 12-month growth rates are expanding strongly for nonmanufactures of both exports and imports.

Obviously, there are still a lot of cross currents in trade with gyrating oil prices responsible for a lot of that instability. Today in markets oil prices slipped yet again as it is now hard to tell if the Saudis have lost their grip, or lost their will or are waiting to pressure fellow members and launch a new tactic after a dosage of low oil-price pain.

The bottom of the table contains some trade data by country on exports and for imports in the case of the U.K., Germany and France. All six countries show exports expanding over 12 months at growth rates ranging from 20.7% for the U.K. where sterling has been falling to 3.4% for the Netherlands. Still, four of these six countries also have export values falling at double-digit rates over three months France, Finland, the Netherlands, and Portugal.

For Germany, exports are still steady/strong. For the U.K., with a weak exchange rate as a tail-wind, exports are busting out at growth rates of 20% to 30%, but for the U.K. a lower pound has raised the price of imports and import value is accelerating even faster than exports are growing. German imports are relatively strong as they are in France as well.

On balance, the EMU shows an erratic withering of its trade surplus. Germany is part of that process but with its surplus eroding at a slower pace. The higher cost of oil is one huge factor behind the European surpluses shrinking. Outside of the EMU, the drop in the pound sterling is juicing U.K. exports and imports and introducing inflation there. Still, the BOE today in a split vote held policy steady as it braces for more Brexit effects and in the wake of a weak retail sales report. Across Europe manufactures trade shows more stability and more export strength in particular. But trade flows are being impacted, except for the U.K., most trade flows have weakened their pace over three months compared to their pace over 12 months. Some exchange rates are in motion and the Brexit process will soon be adding to that toll.

Speaking of tolls...

With the Federal Reserve in the U.S. taking its next step to hike rates amid less than glowing economic performance, it is warning that it plans to continue tightening and it is adopting a program to shrink the balance sheet as well and starting that process before yearend. In the wake of that decision, there will be more pressure on other central bankers to follow suit. Bond yields are affected pretty much straight up across countries and across exchange rates when changes are made. If the Fed begins a process of balance sheet normalization, there are likely to be effects on U.S. interest rates and knock on effects on interest rates overseas. Central banks that normalize last will be paying the highest costs for normalization as those that did QE will be reducing assets in a higher rate environment meaning that their asset sales will produce lower proceeds and cause the asset selling central bank to incur a larger loss. It's all coming soon to a central bank near you. The controversy about policy shifting is only just beginning.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief