Global| Jul 14 2017

Global| Jul 14 2017EMU Trade Surplus Expands: Is Trade Back on Track? Is It Fair?

Summary

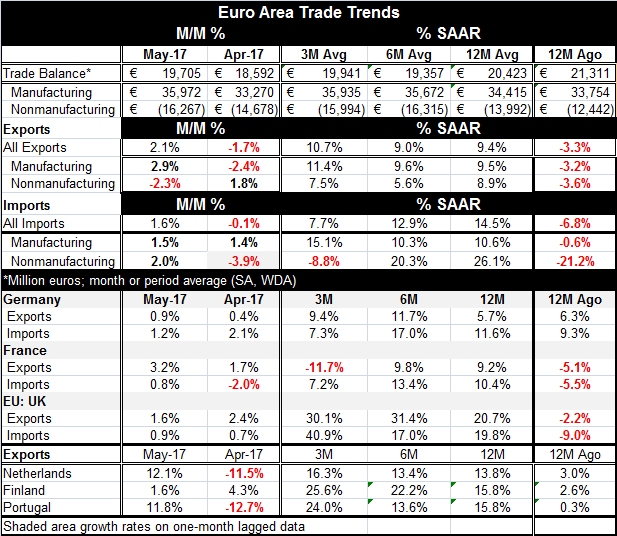

The EMU trade surplus rose to 19.7 billion euros in May from 18.6 billion euros in April. That compares to a 12-month average of 20.4 billion euros. The euro surplus has been a political hot potato that Germany is a part of and has [...]

The EMU trade surplus rose to 19.7 billion euros in May from 18.6 billion euros in April. That compares to a 12-month average of 20.4 billion euros. The euro surplus has been a political hot potato that Germany is a part of and has sought to defend while the U.S. has attacked Germany for its uncompetitive trade as evidenced by its large structural surplus. This month will not bring the two sides closer together. While as far as I know Angela Merkel has not actually done this on Facebook, her campaign has de-friended the U.S. and Donald Trump. She no longer refers to the U.S. or Mr. Trump as Germany's close friend and has accused the U.S. of no longer being a trusted ally. The ongoing surplus condition in Europe and its expansion will help to extend this atmosphere of acrimony. No one will have to 'show you the acrimony' in a movie starring Tom Cruise- it will be obvious.

The EMU trade surplus rose to 19.7 billion euros in May from 18.6 billion euros in April. That compares to a 12-month average of 20.4 billion euros. The euro surplus has been a political hot potato that Germany is a part of and has sought to defend while the U.S. has attacked Germany for its uncompetitive trade as evidenced by its large structural surplus. This month will not bring the two sides closer together. While as far as I know Angela Merkel has not actually done this on Facebook, her campaign has de-friended the U.S. and Donald Trump. She no longer refers to the U.S. or Mr. Trump as Germany's close friend and has accused the U.S. of no longer being a trusted ally. The ongoing surplus condition in Europe and its expansion will help to extend this atmosphere of acrimony. No one will have to 'show you the acrimony' in a movie starring Tom Cruise- it will be obvious.

Trade Trends Calm

Over the past few months, the EMU trade balance has been unstable. The EMU surplus dropped sharply in January but has since been rising as the year has progressed and seems headed back to its old stomping ground. Also, early in the year, much of the story was a story of very different trends for manufactured goods vs. nonmanufactured goods, as oil prices bobbed around and dictated the month's trade events. Oil prices are still unstable and until very recently they have been undergoing another albeit a measured bout of weakness. Oil prices are now showing little enough variation and have been stuck in a range for long enough that they are not imparting huge volatility to the trend picture and we see that this month. Oil still plays a part, but it no longer is dominating.

In May, German exports grew by 2.1% with imports up by 1.6%.

Export Trends

Let's look at exports first. On the month, manufacturing exports rose by 2.9% with nonmanufacturing exports falling by 2.3%. From 12-month to six-month to three-month, EMU manufacturing exports are advancing at annual rates of 9.5% to 11.4%, consistently strong and also stable. Nonmanufacturing exports have been slower to gain but are still in a range of 5.6% to 8.9%, a solid range.

Import Trends

EMU manufacturing imports are up by 1.5% in the month with nonmanufacturing imports up by 2.0%. Manufacturing imports have a strong and consistent profile with sequential growth rates ranging from 10.3% to 15.1% and showing some tendency to accelerate. For nonmanufacturing imports, there is a slowing in progress from a 12-month gain of 26.1% to a six-month pace of 20.3% to a three-month pace of -8.8%. The weakness in oil prices does show through over the recent three months, but oil does not dictate the profile of trade.

The Balance... On Balance

However, under the surface the conditions that make the U.S. angry are getting worse as the EMU manufacturing balance rose to a surplus of 36.0 euro billions in May from 33.3 euro billions in April; it is above its 12-month average of 34.4 euro billions. That trend is hidden by the deterioration in nonmanufacturing trade where the deficit rose to 16.3 euro billions in May from 14.7 euro billions in April compared to a 12-month deficit of 14.0 euro billions.

Select Country Trends

Germany: For Germany, imports grew faster than exports over 12 months, but over three months the situation is reversed with exports slightly stronger.

France: French exports trail imports by a slight amount over 12 months with both pacing at a near 10% rate. Over three months French exports are off at a double-digit annualized pace with imports still growing firmly.

U.K.: Sterling's deprecation calls the tune here. Exports are on a tear on growth rates from 12-month to six-month to three-month that run at rates of 20% to 30% annualized. Imports in the U.K. are up strongly at a 19.8% annual rate over 12 months, but the annualized rate has been jacked up to a colossal 40.9% pace over three months on sterling weakness even in the face of weak oil prices.

Netherlands, Finland and Portugal: In this triad of odd EMU bedfellows, exports are rising at a pace of 14% to 16% over 12 months. These rates accelerate to a range of 16% to 25% over three months.

Normalizing trade or old habits dying hard?

The trade picture in Europe is looking much more normal. Exports are not just recovering, but for a nice varied grouping of countries, exports are showing some real strength and acceleration across the board and brining EMU surpluses back to life. Of course, the numbers for the U.K. reflect mostly inflation and are based on sterling. The Bank of England is still trying to decide if this import price bubble which is the pass-through effect (that should have been expected from a sharp plunge in sterling) is worth a policy response or not since Brexit inspired weakness lies ahead. So far, U.K. import price inflation has not leap-frogged to domestic prices. As long as inflation remains an artifact of weak sterling, the BOE can choose to hold its fire on policy. It has done this so far, but Mark Carney has put markets on notice that at some point this period of super accommodation will end. Plus he is dealing with some actual policy dissent among his fellow monetary policy committee members.

Fair-weather Friends Hit Foul Weather

The revival of trade in Europe is not occurring in a way to lessen trade tensions with the U.S. which have mostly been hopped up in U.S. discussions with Germany. While Germany and other Europeans are doing what they can to tar the U.S. image on its varied stances of climate control, free trade and NATO, the fact is that they are the ones with the structural trade surpluses that take domestic demand from the rest of world while the U.S. deficit gives the world stimulus as that stimulus also leaches wealth from the U.S. economy. Under Donald Trump, there is finally some complaint about this long standing leaching relationship. Europe has taken this sort of exploitation of markets for granted as though it were a birth right and as though it were endorsed by economic theory (which it most definitely is not). This demeanor also fits with the mood expressed in Europe when President Trump began to insist and demand that Europe pay for more of its own defense in NATO. That sparked the de-friending of the U.S. by Angela Merkel. Despite fact the Germany can afford this and is nearly running a fiscal surplus while the U.S. runs large fiscal deficits, apparently this is an 'unfriendly' move by the U.S. Why the U.S. should run a larger fiscal deficit to defend Europe and Germany while Germany spends less and runs a fiscal surplus is beyond my understanding. And why a German leader should get her back up over an effort to change this relationship makes no sense at all. The U.S. should be thanked for its loyalty and financial contributions over all these years and for its ongoing willingness to stay in the relationship IF Europeans pay their fair share. Why should that condition be a sticking point? Should we spend to protect people who will not spend to protect themselves? This was not done as a threat by the U.S. to abandon Europe but a hardline drawn to let them know that the gravy train ride is over and they needed to pony up. And they have been asked (so very nicely) on this points for years. This tougher line was forced on them by their own actions (inactions). It's no wonder Europe does not like Trump. He is a man of action and the policy is America first, not Germany first. Is the U.S. only 'your friend' when it pays your way? Who is the fair weather friend here? We want someone to have our back in NATO too. The least they could do is help protect our wallet.

Hijacking Free trade

The U.S. has run large and consistent trade and current account deficits for most of the post Bretton Woods era. In the more recent years since early 1981, the U.S. has run no surpluses at all. And the reason is not U.S. over-consumptiveness or under-saving but the manipulation of exchange rates to create and preserve certain trade patterns. Floating exchange rates were supposed to be shock absorbers and a mechanism to give countries more policy independence, not a vehicle to be exploited for mercantilism in trade. The academic study of fluctuating rates expected that exchange rates would move to restore balance after current account imbalances arose. But that has not been the case. Exchange rates have been used to manage trade imbalances to make them so and keep them thus. To make the point in its simplest form, had we stayed on a Bretton Woods gold standard the trade surplus countries never would have accumulated such surpluses or been able to raise exports to drive such strong domestic growth rates since a current account surplus would imply a transfer of gold to the surplus country from the deficit country and no one would have been willing to lose that order of magnitude of its gold reserves. So this is the point of Donald Trump whether he knows it or not. The exchange rate systems combined with commercial policy enforcement has been hijacked to the U.S. disadvantage. Even if tariffs are low and if lower tariffs cover a broader array of products than in the past, this has not been free or freer trade. The trade statistics themselves aptly demonstrate that trade has produced a result not expected under Free Trade.

Put on Your Big Boy Pants One Leg at a Time Europe

Mr. Trump's pressure for fair trade will slow global growth and will force more consumption from low consumption nations like China and like Germany that will need to provide more of the demand at home to drive their output since they will not be able to do it through chronic trade surpluses anymore. And there will be a lot a friction on the way to doing this because it has not been their way of life and each of these - and several other- economies have built a nice way of life suckled by gaming the exchange rate feature of this system. But this watch is over. There will be a new order simply because economic stability demands it, not because Donald Trump demands it, although he is the proximate cause. Large structural and enduring trade imbalances are dangerous and destabilizing. It's time for the rest of the world to recognize that they have two feet in several respects and to stand on them and to find a way to do it without the acrimony of kicking the U.S. in the shins because it wants them to put on their big-boy pants and stand on their own two feet. Donald Trump is not the bad guy many paint him as. He is the messenger being upbraided for a message others don't like. But what the U.S. had been doing before he took office was wrong, unsustainable and damaging to the U.S. economy. Fixing it is way overdue. And now we see how our allies really view us. It appears that we never really had their respect. They only wanted our money. But now that we know that, it is a base on which to build a relationship that both sides can understand instead of misunderstand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief