Global| Oct 20 2015

Global| Oct 20 2015EMU Trade Surplus Contracts in August

Summary

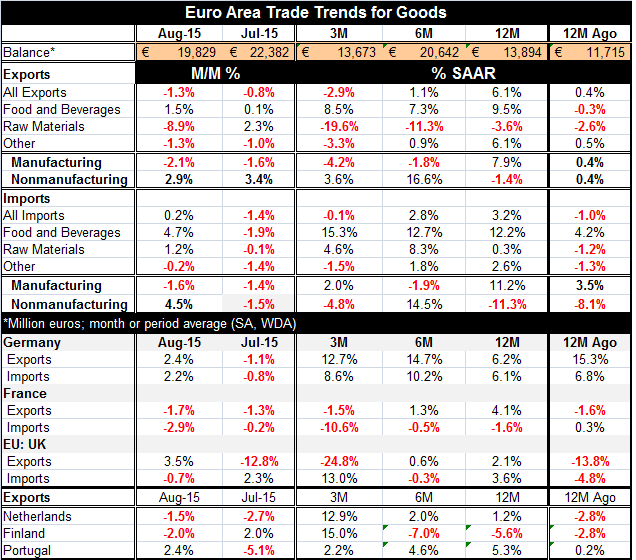

The EMU trade surplus contracted sharply in August, falling by 2.5 billion euros month-to-month. Still, the surplus is smartly higher year-over-year. Both exports and imports are losing momentum (see chart). In August, exports fell by [...]

The EMU trade surplus contracted sharply in August, falling by 2.5 billion euros month-to-month. Still, the surplus is smartly higher year-over-year. Both exports and imports are losing momentum (see chart).

The EMU trade surplus contracted sharply in August, falling by 2.5 billion euros month-to-month. Still, the surplus is smartly higher year-over-year. Both exports and imports are losing momentum (see chart).

In August, exports fell by 1.3%, their second consecutive monthly drop. As a result, exports also are lower over three months.

Imports edged higher by 0.2% in August after a 1.4% decline in July and are only slightly lower over three months.

Both exports and imports show a tendency toward weakness in their sequential growth rates inside one year. For exports, that trend is amplified for the exports of manufacturers alone where the 12-month growth is at a strong 7.9% and gives way to a -4.2% pace over three months. For imports, there is not quite the same affirmation of weakness from manufacturing flows. But the 12-month pace for imports at 11.2% is well above its six-month and three-month rates. Nonmanufacturing trends, of course, are subject to a great deal of variability owning to the unstable prices in this environment. So the trends of manufactures are likely to be more telling.

By country, Germany continues to show solid export and import growth. But France shows declining exports and imports over three months and sharply declining imports over most recent horizons. The U.K., an EU member country, shows some erratic growth rates with exports sharply lower over three months and imports rising sharply on that same horizon- a very mixed picture. The Netherlands, Finland and Portugal show some recent monthly export weakness but demonstrate growth over three months.

The trade picture has been erratic. The euro exchange rate is low and that should impart to all EMU members a degree of competitiveness when trading with nations outside the monetary union. But global growth is still so weak that price competitiveness is not the help that it could be in better times.

The overall picture of the EMU, drawn from its trade performance by looking at manufactures and nonmanufactures, exports and imports, is not very reassuring. We know that because of the weak euro exports should be supported; yet, overall EMU export growth is not very good and is fading. That performance is worse for manufactures and it's not a good sign at all. Overall nominal import weakness is also a bad sign since imports should reflect the conditions of domestic demand. They appear slack from this gauge. What logical guesses we can make of EMU economic conditions from the state of its trade picture are not reassuring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief