Global| Jun 15 2018

Global| Jun 15 2018EMU Trade Deficit Shrinks

Summary

The EMU trade balance shrank in April, stepping back to a surplus of €18.1bln from €19.8 bln in March. One year ago the surplus stood at €20.4 bln. Exports nudged higher in April rising by 0.3% while imports surged by 1.4%. That [...]

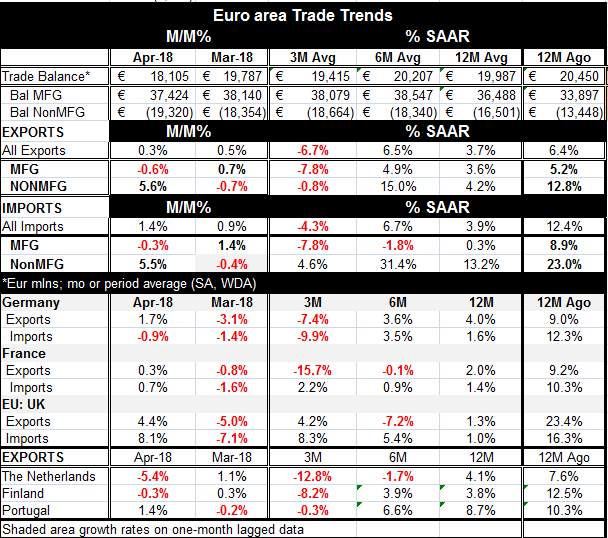

The EMU trade balance shrank in April, stepping back to a surplus of €18.1bln from €19.8 bln in March. One year ago the surplus stood at €20.4 bln. Exports nudged higher in April rising by 0.3% while imports surged by 1.4%. That combination of evens made the trade deficit smaller.

The EMU trade balance shrank in April, stepping back to a surplus of €18.1bln from €19.8 bln in March. One year ago the surplus stood at €20.4 bln. Exports nudged higher in April rising by 0.3% while imports surged by 1.4%. That combination of evens made the trade deficit smaller.

However, a shrinking surplus is not something that is well entrenched in European trade trends. Over three months exports are falling by 6.7% with imports falling by a lesser 4.3%. This pair of growth rates also reinforces a smaller deficit trend. But over six-months and 12-months the export and import growth rates are nearly identical and there is not much deficit shrinkage in the cards on those trends.

In the wake of the G7 summit, trade is obviously in a special spot light. Today, US President, Donald Trump indicated 25% tariffs on $50bln of US imports from Chinese. China wasted no time in offering the same tariffs on $50bln of US exports to China. It is not going to stop there. The US continues to make waves over trade on a broad front and the cold war over trade has just heated up. The G7 tiff was an hors d’oeuvres compared to this. Trade and trade performance is going to continue to be an issue in this tainted atmosphere. But it is also true that to a large extent the trend and fundamentals are perceived to be established and the Trump administration is looking for leverage to change results.

We see the stubborn trend in EMU manufacturing trade. Those exports and imports show imploding flows in progress with three month export and import flows declining and 12 month flows showing some gain. But on each horizon 3-months, 6-months and 12-months, exports are either stronger than imports or growing at the same pace. There is no trend ‘improvement’ that diminishes the surplus in manufacturing trade.

Non-manufacturing flows show the opposite trends. But they are substantially affected by commodity prices and especially oil. Imports of non-manufactures are stronger than exports on all horizons.

Beyond the EMU trends we offer samples of export trends from six other European nations. Five of six show exports declining over 3-months. Over six months most exports also show stable or slowing trends. And compared to one year ago the current year-over-year trends are lower. There is a broad slowdown in exports to couple with the stubborn EMU surplus.

Now, we are on the slippery slope with trade. This is no longer saber-rattling. This is stabbing and cutting and hacking. Damage will be done. The global economy already is showing some signs of slowing. The US continues to be the most resilient but US economic signals are still somewhat spotty despite the recent strength in US retail sales and in manufacturing PMI reports. Today’s drop in in US industrial output is an example of how no sector is safe or dependable. It is still too soon to know if the Trump tax cuts and fiscal reforms are going to deliver growth in the US. The European slowdown is severe enough to capture attention of newspaper reporters. Japan has cuts its outlook for inflation, but not growth. And, despite slowing in Europe and some very weak recent numbers from Germany, the Bundesbank has just cut is outlook and describes the situation as a boom with ‘strong wage growth’ and higher domestic inflation. Frankly I don’t think I have seen that particular German economy. But what’s important is that although the Bundesbank does, it’s the ECB that makes monetary policy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief