Global| Apr 17 2008

Global| Apr 17 2008EMU Trade Deficit Shoots Back Into Surplus

Summary

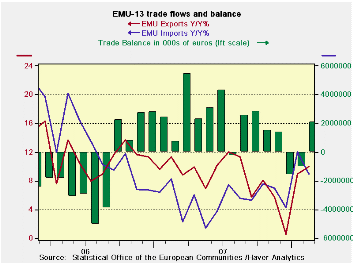

The Euro Area is not going to make it easy for us to understand it. After two months of deficits, the trade surplus is back. Imports fell across the board in February paving the way for the trade improvement. Both export and import [...]

The Euro Area is not going to make it easy for us to understand it. After two months of deficits, the trade surplus is back. Imports fell across the board in February paving the way for the trade improvement. Both export and import flows have accelerated in recent months. But the year/year import picture is showing some softening. Meanwhile, exports, after looking for all the world like the strong euro value was getting to them toward the end of 2007, have rebounded sharply and put in two strong months of growth. Export growth exceeds import growth again in February (Yr/Yr) for the fist time since early in 2007.

These trends create a quandary about growth. The main research houses in Germany have cut German and EMU growth estimates for this year. But how much of this is financial uncertainty at work, and how much is due to the strong exchange rate? The institutes expect EMU exports to slow in 2008 and to slow further in 2009. Meanwhile, import volume is expected to slow slightly as well in 2008 and in 2009. The picture is still one of an expanding surplus because even though exports are projected to slow over the period they are continuing to outpace imports early in 2008 and will only lose out by small growth differentials in 2008 for the year as a whole and not enough to overwhelm the fact that exports already exceed imports. Exports will, however, slip relative to imports again in 2009, bringing a small deficit. While the strong euro seems to be having some impact it is not enough to bring persisting deficits to the e-Zone trade account until 2009. It makes you wonder how much pain the current euro exchange rate is causing and if it is proportional to the noise that is being made about it? The euro seems high. The trade weighted real euro exchange rate is extremely high. And Europe is quite trade-dependent. So why is the euro’s strength having such a small impact on trade? That remains a conundrum. The Euro reached a record high Vs the dollar and real trade-weighted high in late 2007 yet even by end 2009 the impact on trade is expected to be muted.

| Euro Area-Trade Trends for Goods | ||||||

|---|---|---|---|---|---|---|

| m/m% | % Saar | |||||

| Feb-08 | Jan-08 | 3M | 6M | 12M | 12M Ago | |

| Balance* | €€ 2,103 | €€ (1,048) | €€ (178) | €€ 876 | €€ 1,888 | €€ (569) |

| Exports | ||||||

| All Exp | 2.0% | 6.8% | 23.5% | 10.4% | 10.0% | 11.4% |

| Food and Drinks | -1.7% | 3.4% | -2.5% | -0.5% | 5.4% | 10.8% |

| Raw materials | 1.0% | 6.4% | 28.3% | 12.0% | 13.2% | 5.2% |

| Other | 2.2% | 7.0% | 25.2% | 11.1% | 10.3% | 11.5% |

| MFG | 0.3% | 6.6% | 7.9% | 1.6% | 6.6% | 10.1% |

| IMPORTS | ||||||

| All IMP | -0.4% | 6.3% | 21.1% | 11.4% | 9.0% | 8.3% |

| Food and Drinks | -2.1% | 2.8% | -4.4% | 7.1% | 9.1% | 11.4% |

| Raw materials | -1.3% | 1.5% | 5.0% | -4.7% | -1.1% | 24.5% |

| Other | -0.3% | 6.8% | 23.8% | 12.6% | 9.5% | 7.3% |

| MFG | -2.8% | 4.6% | -1.5% | -8.6% | -2.5% | 12.8% |

| *Millions of Euros; mo or period average | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief