Global| Feb 15 2018

Global| Feb 15 2018EMU Trade Balance Logs Larger Surplus

Summary

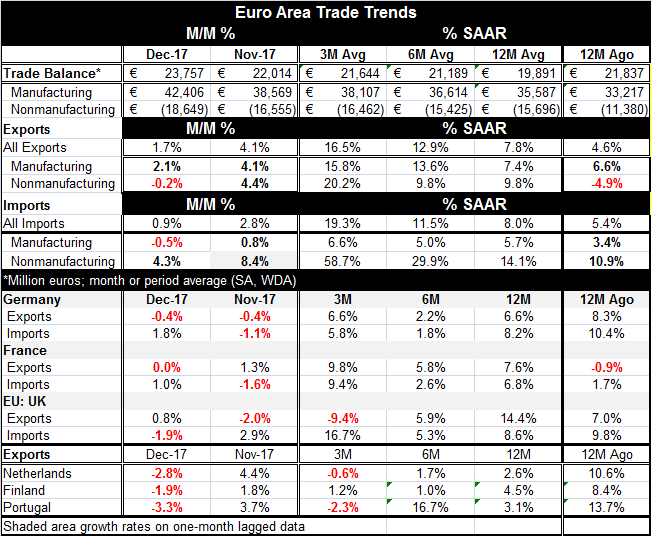

In December, EMU exports rose by a strong 1.7% as imports gained 0.9% with the net result of driving the euro area trade surplus even higher. The surplus is the third highest of all time for the euro area at a time that U.S. President [...]

In December, EMU exports rose by a strong 1.7% as imports gained 0.9% with the net result of driving the euro area trade surplus even higher. The surplus is the third highest of all time for the euro area at a time that U.S. President Donald Trump is on the warpath about fair trade and talking about implementing a reciprocal tax.

Germany has a huge current account surplus to GDP ratio. South Korea is not far behind it. China's aggregate surplus is large, but it is a much larger economy and its ratio to GDP is more tempered. However, these are countries with long-term surpluses, structural surpluses. These surpluses through the balance of payments accounting constraint imply that offsetting deficits must exist in other countries, and of course, the U.S. has run unrelenting deficits since the early 1980s. Asian countries try to explain this away by saying they have a high saving rate and the U.S. saving rate is too low (or alternatively that the U.S. 'consumes' too much). In accounting terms, that is another way to look at the picture. But all that could be remedied by Asian countries stopping their relentless acquisitions of foreign exchange reserves (dollars) and allowing the consequence of that to flow through foreign exchange markets. In addition to their high saving rates, these countries buy a lot of dollars to add to their foreign exchange reserves, an action that artificially inflates the demand for dollars and raises the dollar's foreign exchange value; thereby, undercutting U.S. competitiveness and paving the way for China, South Korea and others to continue with export-led growth. A variety of factors explain the German situation including less than open markets and a situation Germany has contrived in its currency arrangement to make sure that Germany is the most competitive economy in the EMU system.

December trade

The euro area trade data for December show a larger deficit on nonmanufacturing trade (as oil prices have risen). That is more than offset by a fast rising surplus in manufacturing trade.

Short term, some flows have accelerated

EMU manufacturing exports have double-digit growth over three and six months while for manufactured imports, the growth rates are less than half of what they are for exports. For nonmanufacturing trade, the growth rates of imports are explosive on what have been steadily rising oil prices -- a move in price that has been wholly manipulated by OPEC and Russia against the fundamentals as the IEA estimates that oil supply will nonetheless outstrip demand in 2018. Getting oil prices higher in this circumstance is like getting water to flow uphill.

Annual export pace remains quite moderate

Rising oil prices have boosted trade growth, in some cases sharply, in the short run. But German and French exports over 12 months show growth in the neighborhood of six and one-half to seven and one-half percent. U.K. exports reach nearly 15% pace. But for the Netherlands, Finland and Portugal, nominal export growth is under a pace of 5% over 12 months.

Global growth is supposed to be picking up. The EMU and German surpluses remain high. And while rising oil prices put a sugar-coating on trade value growth, the annual export growth of the six countries in the table shows only one, the U.K., with export growth in double digits. The Baltic Dry goods index, a well-known trade barometer is currently embroiled in an ongoing contraction. What is going on here? How can trade volume be slowing when global growth is supposed to be on an upswing? Yet, the annualized export growth metrics here are not particularly impressive. It's just one of the paradoxes lying in the weeds and threatening the tidy belief in a bullet-proof global revival. Is this just another cycle in the Baltic index that is part of the uptrend or is it something to worry about?

Global growth is supposed to be picking up. The EMU and German surpluses remain high. And while rising oil prices put a sugar-coating on trade value growth, the annual export growth of the six countries in the table shows only one, the U.K., with export growth in double digits. The Baltic Dry goods index, a well-known trade barometer is currently embroiled in an ongoing contraction. What is going on here? How can trade volume be slowing when global growth is supposed to be on an upswing? Yet, the annualized export growth metrics here are not particularly impressive. It's just one of the paradoxes lying in the weeds and threatening the tidy belief in a bullet-proof global revival. Is this just another cycle in the Baltic index that is part of the uptrend or is it something to worry about?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief