Global| Apr 07 2015

Global| Apr 07 2015EMU Services Sector Is the Backbone of Recovery

Summary

The chart on the left underscores the relationship between the services sector and consumer confidence. The two series have moved in a near lockstep phase over the last five years and seem to have become more closely linked over the [...]

The chart on the left underscores the relationship between the services sector and consumer confidence. The two series have moved in a near lockstep phase over the last five years and seem to have become more closely linked over the past two years.

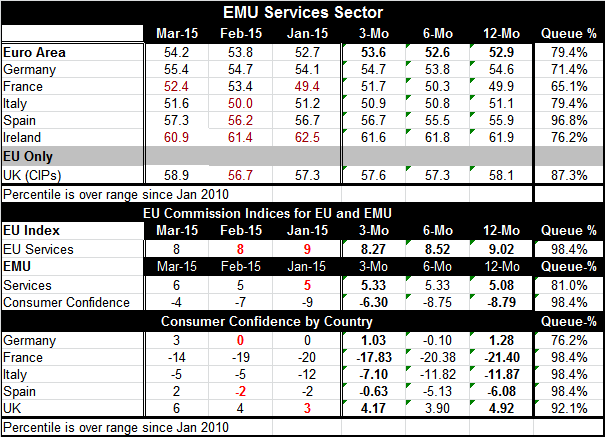

The chart on the left underscores the relationship between the services sector and consumer confidence. The two series have moved in a near lockstep phase over the last five years and seem to have become more closely linked over the past two years.

The queue standing of the services indicators for the EMU and its reporting members is at the 79th percentile. However, the two largest EMU economies come in with services sector standing below this mark with Germany at the 71st percentile and France at the 65th percentile. But Italy and Spain, the third and fourth largest economies, respectively, fare better. Italy's standing at its 79th percentile is right on the EMU average while Spain at the 96th percentile is much better.

The services sector continues to post higher percentile standings than the manufacturing sector by a wide margin across the euro area. That sector has become the backbone of Europe's recovery. Both manufacturing and services are growing, but compared to their respective historic norms, the services sector readings are much stronger than their manufacturing sector counterparts. That is the condition that the queue standings document.

While we might have expected EMU recovery to work more through manufacturing due to the impact the weak euro has had to enhance competitiveness, that is not the way it has happened. In some sense, that is the good news. With the euro continuing to be so much weaker, we would still expect a kick to the manufacturing sector to occur on top of the recovery in services.

The real story seems to be how conditions and perceptions have shifted in the EMU to impact consumer confidence. We see this in the EU Commission indicators for consumer confidence. The EU Commission indices also demarcate a services gauge that for the EMU stands in its 81st percentile, very close to the 79th percentile standing in the Markit framework reported above. On that ground, the two approaches do not seem so different. They have different absolute metrics, but their relative standings are nearly identical. That gives us reason to have more confidence in their message. The EU Commission take on consumer confidence shows generally much higher (queue) standings for confidence than even for services. Confidence is leading.

While the U.S. Federal Reserve has been making a big deal out of forward guidance (actually calling it a new `tool') and giving point estimates for future Fed funds rate by members, the ECB seems to have really won credibility with its policies and convinced people they will be successful. That must be the case since confidence has improved by leaps and bounds more than the actual improvement logged in either the services sector or the manufacturing sector in the EMU. The services sector's improvement seems to be the biggest beneficiary of this impact. And that is where you expect to see it if consumer attitudes are being driven by expectations instead of real events. Consumer spending habits will start small and work their up to durable goods when conditions improve further. That explains why the services sector is up ahead of manufacturing. Of course, to keep this momentum, the economy will have to perform as people have been encouraged to believe that it will.

Unlike the Fed in the U.S., Europe seems to be getting a response from its real sector. In the U.S., the manufacturing sector peaked in August 2014 and is steadily slowing according to its ISM index. Meanwhile, services in the U.S. also are off peak and making a more irregular decline. QE has been over for some time in the U.S. while Europe is in the throes of new stimulus. This is not exactly the performance you expect from the U.S., an economy where the central bank is poised to hike interest rates, believes the economy has shed its training wheels and turned the corner. Has it really? We will want to keep a close eye on real sector developments in both the U.S. and EMU. Financial and real sector conditions are in flux. The Fed clearly is fishing for a reason to hike rates but seems to have found a new source of disappointment. Europe's monetary policy is much more set in stone full speed ahead. But unexpected weakness in the U.S. has halted the dollar's rise for now as markets continue to handicap real world events.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief