Global| Sep 05 2017

Global| Sep 05 2017EMU Services Sector Continues to Pull Back

Summary

The service sector PMIs for the largest EU and EMU members took a step back in August everywhere but in Germany. But unlike many measures where Germany is the exception, and is so because it is so much stronger than the rest of [...]

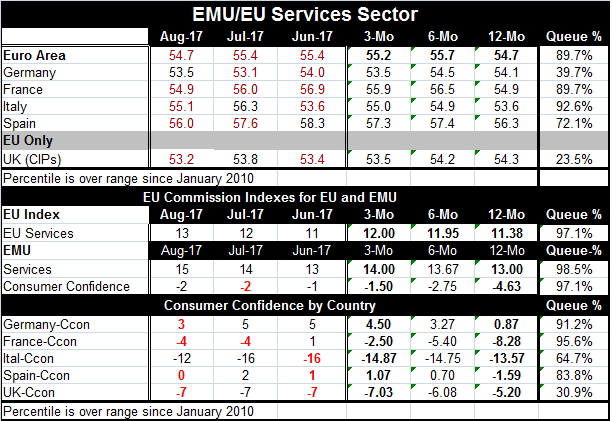

The service sector PMIs for the largest EU and EMU members took a step back in August everywhere but in Germany. But unlike many measures where Germany is the exception, and is so because it is so much stronger than the rest of Europe, in this case Germany is the laggard with the lowest raw diffusion score among the big four EMU members and with the lowest percentile standing as well. The U.K. raw diffusion index is slightly weaker than in Germany as is its percentile queue standing.

The service sector PMIs for the largest EU and EMU members took a step back in August everywhere but in Germany. But unlike many measures where Germany is the exception, and is so because it is so much stronger than the rest of Europe, in this case Germany is the laggard with the lowest raw diffusion score among the big four EMU members and with the lowest percentile standing as well. The U.K. raw diffusion index is slightly weaker than in Germany as is its percentile queue standing.

As the chart shows, there are very different things going on in the manufacturing and services sectors as manufacturing continues to reach to new recent highs while the services sector skids.

Consumer confidence which is an overarching gauge not drawn from any particular sector shows elevated readings for confidence in the 90th percentile for France and Germany despite the weak German services sector. Spain's consumer confidence has an 83rd percentile standing, reasonably firm-to-strong. Italy's standing on the EU measure of confidence is in its 63rd percentile, much weaker than its domestic measures. U.K. confidence resides in the lower quartile of its percentile queue and like many U.K. measures is impacted by Brexit concerns.

Still, euro area retail sales declined in July on a fall in food sales. Retail sales volume decreased 0.3% month-on-month in July, partially offsetting June's 0.6% increase. The pace of decline matched expectations and reminds us how uneven the data reports are. Despite high confidence, including a 90th percentile reading for all of the EMU, consumer spending continues to struggle. The services sector that is the main job sector does not seem to underpin job growth all that well, but confidence stays aloft. And it is hard to understand country level differences as Germany with such a weak services sector logs a strong EU confidence reading and an even stronger domestic confidence reading.

Internationally, there are fewer of the service sector gauges available than there are manufacturing readings. But services gauges for some select economics show Japan weaker in August with a 60th percentile overall standing for services. China is up in August after weakening in July and with the same 60th percentile standing as Japan. Russia saw its services sector improve significantly month-to-month in August and has a 73rd percentile standing, a firm reading. India improves in August but continues to show contraction in its services sector. It has been floundering around and below the zero growth line since November.

As excited as one might get over the recent manufacturing PMI data, the services outturn reflects how depressed one might get over the recent services trends. The global economy is not firing on all cylinders and is difficult to puzzle out. The fact that manufacturing is having a better/faster revival in Europe and in the U.S. is another aspect of the surprising nature of developments in this cycle. In most places, consumer confidence is holding up better than you might think given some of the recent gauges such as in Germany with weak services. But there are also other strong German reports like the IFO and ZEW surveys which support strong consumer readings. In the U.S., there is a very strong ISM manufacturing and a very weak reading from Markit on the exact same subject.

Thoughts on growth

All of this leads me to several thoughts on the matter of growth. If growth is uneven, different approaches to measuring it may produce different results. So I am led to the conclusion that growth in fact is uneven regardless of the metric. On the matter of consumer confidence, we have several very different readings for the concept for same country and with confidence I think the problem is that it is difficult to measure and that it is a relative gauge. I presume that one of the things going on with confidence is that people are beginning to lower their standards and giving off higher readings for weaker growth because it is clear that conditions are shifted and people are shifting their expectations and standards for evaluation. These sorts of things might produce different results under different survey methods. As we see for the EMU in July, despite glowing manufacturing performance and strong confidence, spending is sputtering. In many ways, the world is just not what it seems or at least it refuses to lie down and be what we think it should be. And that fact continues to bedevil policy particularly monetary policy as inflation continues to settle down and refuses to obey the result that economists have been written in the text books. Inflation is supposed to surprise us by going rogue not soft. What are we to make of that?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief