Global| May 06 2009

Global| May 06 2009EMU Services: In Near Lockstep With US

Summary

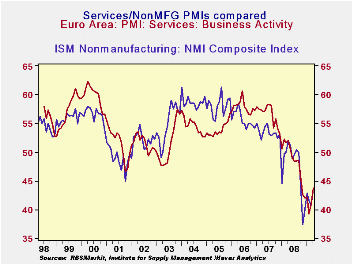

April’s jump is the second largest increase in Markit’s e-Area Services PMI index since late 2000. The April surge brings the index up to 43.76 still well below a neutral reading of 50 but that still leaves the index relatively low in [...]

April’s jump is the second largest increase in Markit’s e-Area

Services PMI index since late 2000. The April surge brings the index up

to 43.76 still well below a neutral reading of 50 but that still leaves

the index relatively low in its historic range in the 21st percentile.

Over the same period, however, the EU Commission’s EMU service sector

index stands at the 8th percentile in its range, a relatively weaker

reading. If we assess the Markit reading on a queuing basis, by ranking

the index reading and telling where the current percentile of the

ranked readings stands, we find it is in the bottom 5% of all readings.

That is more similar to the dismal EU Commission’s assessment. Anyway

you slice it the index it is showing improvement but the current

assessment is still poor.

The month’s move is strongly in the right direction and the

improvement is cast wide across reporting EMU countries. It also fits

nicely with the pattern of improvement reported by the Markit MFG

indices. The current ISM reading ranks 97th out of the last 102

readings. Most EMU countries are at about that some relative position.

Ireland is worse off, posting the second worst reading in the last 102

observations. Over this same period the US ISM for nonMFG, the closest

comparison we have to the EMU reading, also ranks 97th out of the same

102 observations. The US and EMU ‘services’ sectors are roughly in the

same cyclical position.

In terms of the levels of the readings the US is now a hair

behind the level posted in EMU and behind it as a percentage of the

mean as well. So EMU services have rebounded quite sharply but in

comparisons with the US, the US rebound was sharper. The main reason

that the US is better off in percentile terms is that it had carved out

a lower low in this cycle than did EMU services. So its standing in its

range is better relative to its lower low. Both service sectors are now

on about the same path for recovery.

| Markit Services Indices for EU/EMU | |||||||

|---|---|---|---|---|---|---|---|

| Apr-09 | Mar-09 | Feb-09 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 43.76 | 40.95 | 39.24 | 41.32 | 41.77 | 45.11 | 21.1% |

| Germany | 43.76 | 42.30 | 41.32 | 42.46 | 44.05 | 47.77 | 12.4% |

| France | 46.52 | 43.64 | 40.18 | 43.45 | 43.27 | 46.12 | 25.9% |

| Italy | 42.05 | 39.10 | 37.85 | 39.67 | 39.98 | 43.80 | 17.5% |

| Spain | 42.30 | 34.11 | 31.73 | 36.05 | 33.39 | 35.39 | 43.7% |

| Ireland | 32.16 | 35.69 | 31.78 | 33.21 | 33.39 | 37.02 | 1.1% |

| EU only | |||||||

| UK (CIPs) | 48.68 | 45.47 | 43.24 | 45.80 | 43.36 | 45.17 | 42.0% |

| US NONFMG ISM | 43.70 | 40.80 | 41.60 | 42.03 | 41.08 | 45.09 | 26.3% |

| EU Commission Indices for EU and EMU | |||||||

| EU Index | Apr-09 | Mar-09 | Feb-09 | 3Mo | 6Mo | 12Mo | Percentile |

| EU Services | -30 | -31 | -29 | -32.67 | -30.67 | -24.83 | 8.3% |

| EMU | Apr-09 | Mar-09 | Feb-09 | 3Mo | 6Mo | 12Mo | Percentile |

| Services | -24 | -25 | -24 | -24.33 | -20.67 | -11.42 | 1.9% |

| Cons Confidence | -31 | -34 | -33 | -32.67 | -30.67 | -15.89 | 8.3% |

| Consumer confidence by country | |||||||

| Germany-Ccon | -34 | -31 | -29 | -31.33 | -26.33 | -16.92 | 0.0% |

| France-Ccon | -32 | -36 | -36 | -34.67 | -33.67 | -28.75 | 10.0% |

| Ital-Ccon | -25 | -31 | -28 | -28.00 | -27.67 | -25.25 | 18.2% |

| Spain-Ccon | -39 | -43 | -48 | -43.33 | -44.00 | -41.00 | 18.8% |

| UK-Ccon | -22 | -28 | -32 | -27.33 | -28.83 | -25.67 | 34.2% |

| percentile is over range since May 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief