Global| Dec 05 2017

Global| Dec 05 2017EMU Retail and Auto Sales Catch a Snag As PMIs Advance

Summary

The pullback in retail sales and in auto sales is a bit hard to understand against the background thoroughly painted about a strong ongoing industrial revival. In the first table below, we show retail sales and auto trends with some [...]

The pullback in retail sales and in auto sales is a bit hard to understand against the background thoroughly painted about a strong ongoing industrial revival. In the first table below, we show retail sales and auto trends with some country detail on retail sales. In the second table, we show PMI data for the largest EMU countries as well as the U.S., the U.K., Japan and China. Despite some very solid numbers on the manufacturing side, the demand side of the economy looks much weaker. When we broaden our focus on output to include the top Asian economies, we see a very different picture. And even a closer look within the EMU shows that the PMIs may not be the last word in economic strength.

The pullback in retail sales and in auto sales is a bit hard to understand against the background thoroughly painted about a strong ongoing industrial revival. In the first table below, we show retail sales and auto trends with some country detail on retail sales. In the second table, we show PMI data for the largest EMU countries as well as the U.S., the U.K., Japan and China. Despite some very solid numbers on the manufacturing side, the demand side of the economy looks much weaker. When we broaden our focus on output to include the top Asian economies, we see a very different picture. And even a closer look within the EMU shows that the PMIs may not be the last word in economic strength.

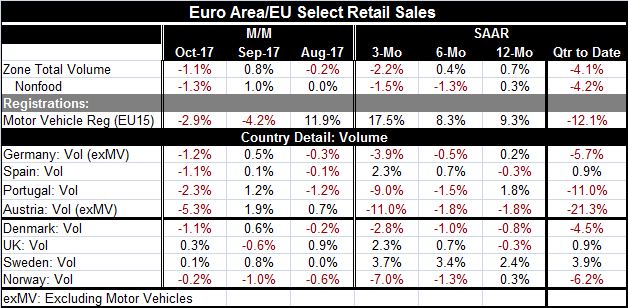

The retail view

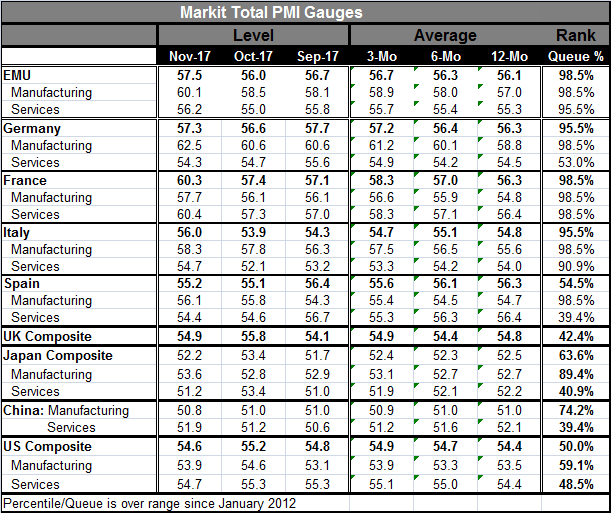

To start with the actual retail view is not the one we would pick out of list of possible companions for the kind of PMI data we have been fielding on Europe. The EMU composite PMI has a 98.5 percentile standing on data back to January 2012. That means it has been as good or better only 1.5% of the time. That is a very impressive figure. Yet, we see that result is paired with a surprisingly weak and deteriorating retail environment. Total retail sales, and sales excluding food, both are showing steady decelerations in their growth rates from 12-month to six-month to three-month. However, vehicle sales are on an accelerating path despite sharp declines in each of the last two months.

All four of the reporting EMU members and two of the four reporting EU-only members show falling retail sales volumes in October. Over three months, three of four EMU members show declining volumes while EU-only members show declines in two of four reporters. In addition, of these eight countries, four have volume declines on the books over 12 months: that is a high proportion.

This is a great deal of weakness in sales, especially against a background where the output sectors are supposed to be so healthy. Of course, we are comparing two very different types of reports. One is a government-sourced report on consumer spending; the other is on industry-level health and is a private sector report. Moreover, one is a traditional accounting report that measures amounts or 'strength' per se, while the other assesses business performance using a private survey based on diffusion responses and more appropriately depicts breadth rather than strength. The breadth of the increases in output is impressive even as the strength in retail sales is losing momentum. So how are to weigh and balance such results?

In the quarter-to-date, retail sales are falling at a better than 4% annual rate. Meanwhile, in the quarter-to-date, vehicle registrations are falling at a double-digit pace.

Turning to the PMI data for the EMU, there are several other truths revealed in the PMI report. The main one is that despite the overall indexes having such strong standings, some important members still show significant deficiencies. For example, even Germany with a 95.5 percentile standing for its own headline PMI sports only a 53rd percentile standing in its own services sector. Spain has a composite PMI that is dragged down to its 54.5 percentile standing because of a weak 39th percentile standing in services. Maybe, these lagging data are more important than they seem?

In the U.K. (still an EU-only nation), its PMI headline at 54.9 signals growth but has only a 42.4 percentile standing, well below its median (that occurs at a standing of 50%). The British retail consortium (BRC) has just given a thumbs-down assessment to British Black Friday sales. Moreover, vehicle registrations in the U.K. are falling for eight straight months. While U.K. inflation has been too high prompting the Bank of England to hike rates and withdraw some of the stimulus it previously injected, it is now facing the challenge of a weakening economy with still stubbornly excessive inflation. Importantly, this commentary would not be complete without noting that the U.K., with a weak PMI reading, is facing moderate growth in retail sales and, in fact, retail sales growth that is moderately accelerating. The oxymorons continue and proliferate.

Looking to Asia, we find some solid-to-strong PMIs in manufacturing but paired with sub-median standings for the services sector in both China and Japan. The U.S. shows moderate PMI readings in both sectors- but as an illustration of the fickleness of PMI readings- a separate survey by the ISM in the U.S. shows very strong manufacturing readings with strong regional surveys from other surveying entities including some by Federal Reserve district banks.

Do not cherry-pick your reality

On the whole, I suspect most people will shake their heads a bit at the retail data. After all, retail sales data always have a certain degree of volatility. We see a bit more of the PMIs and they seem to be a market favorite. If you are a private surveying entity, it is probably the only sort of survey you can get a firm to fill out for you as no one would want to trust you with its actual sales data. While I do like PMI type data and I think it can be very useful, we must always use it with its limitations in mind. I still believe demand is the biggest missing piece in order to believe in global recovery and some acceleration. There is still plenty of supply globally. But demand continues to turn up lame here and there.

The EMU retail sales report for October raises questions about the state of demand in Europe. It may be a bit soon to start counting our growth chickens. And apart from the hurricane snap back and surge in auto spending in the U.S., there is a similar question mark hanging over the consumer's head there.

To be sure, consumer attitudes seem to have improved globally. But one problem with that is that in time I believe consumers learn to accept new realities and to scale back expectations when the baseline for growth shifts. I am still somewhat wary about what improving consumer attitudes mean and mindful that the lack of inflation pressure at a time when many national unemployment rates are low speaks to a need to reinterpret what some of our oldest data reports mean. In that context, I am still not sucked in by impressive PMI scores and I am wary as consumer spending and price trends continue to pancake (no syrup). Be careful not to cherry-pick your optimism or pessimism.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief