Global| Apr 02 2008

Global| Apr 02 2008EMU PPI Trends Press Higher…

Summary

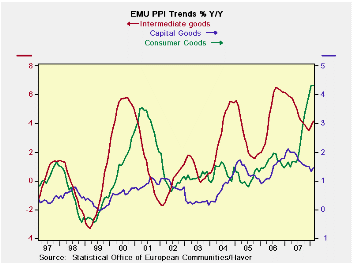

PPI trends are decidedly poor in the Euro Area. The core PPI excluding energy is on the rise with its three-month pace at 5.1% up from 3.9% over six months and from 3.6% over 12 months. This sort of acceleration in the ex-energy rate [...]

PPI trends are decidedly poor in the Euro Area. The core PPI excluding energy is on the rise with its three-month pace at 5.1% up from 3.9% over six months and from 3.6% over 12 months. This sort of acceleration in the ex-energy rate is going to be disquieting. This sort of pressure is the reason that the ECB remains vigilant on inflation and that a German Banker group, the German Bankers Association (BDB), registered concerns today about strong inflation pressures and elevated wage deals. The BDB is concerned about a wage-price spiral. ECB rhetoric is usually couched in terms of avoiding ‘second round effects’ and anchoring inflation expectations.

However you express these concerns, the PPI embodies the risk that the ECB and the German bankers fear.

So far, however, it is the PPI that is bad off and the HICP that is relatively better behaved. HICP inflation rates are more subdued. But there will be concerns that this PPI inflation pressure and this ex-energy trend can be passed on. Germany, France, Italy and the UK (and EU country) each embodies the trend of an accelerating ex-energy price spurt. That by itself is troubling. At 3.6% the yr/yr rate for PPI inflation in the EMU is already ahead of the allowable ceiling (2%) for the HICP. Italy’s 12-mo ex-energy PPI pace is 5.7%, France’s is 3.1%, and Germany’s is 2.7%. This is a lot of congestion above the ceiling rate for the HICP.

The February PPI is not a welcome report in the Euro Area, nor will the BOE like it..

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro Area 15 | Feb-08 | Jan-08 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Total ex Construction | 0.6% | 0.9% | 6.6% | 7.4% | 5.3% | 2.9% |

| Excl Energy | 0.5% | 0.7% | 5.1% | 3.9% | 3.6% | 3.5% |

| Capital Goods | 0.3% | 0.4% | 3.0% | 2.0% | 1.5% | 2.1% |

| Consumer Goods | 0.3% | 0.6% | 5.0% | 5.2% | 4.3% | 1.6% |

| Intermediate &Capital Goods | 0.6% | 0.7% | 5.2% | 3.2% | 3.1% | 4.4% |

| Energy | 1.1% | 1.6% | 12.0% | 19.9% | 11.7% | 1.0% |

| MFG | 0.6% | 0.5% | 4.7% | 5.8% | 5.3% | 2.5% |

| Germany | 0.7% | 0.8% | 6.1% | 6.0% | 3.8% | 2.8% |

| Ex Energy | 0.5% | 0.4% | 4.0% | 2.7% | 2.7% | 3.0% |

| France | 0.4% | 0.6% | 4.6% | 6.1% | 4.9% | 2.2% |

| Ex Energy | 0.3% | 0.5% | 4.0% | 3.3% | 3.1% | 2.9% |

| Italy | 0.7% | 0.6% | 5.9% | 7.4% | 5.7% | 4.0% |

| Ex Energy | 0.5% | 0.7% | 4.8% | 3.6% | 3.4% | 4.2% |

| UK | 0.1% | 1.5% | 11.8% | 19.2% | 8.3% | -1.0% |

| Ex Energy | 0.3% | 1.1% | 6.8% | 5.2% | 3.9% | 3.5% |

| Euro Area Harmonized PPI excluding Construction. | ||||||

| The EA 15 countries are Austria, Belgium, Cyprus, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, the Netherlands, Portugal, Slovenia and Spain. | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief