Global| Feb 04 2014

Global| Feb 04 2014EMU PPI Remains Weak, So Does Euro Area-Wide Inflation Generally

Summary

Inflation in the euro area continues to be mild. The total for the PPI-excluding-construction rose by 0.4% in December; that was a hearty pace by recent standards. However, it follows a 0.1% increase in November and the three-month [...]

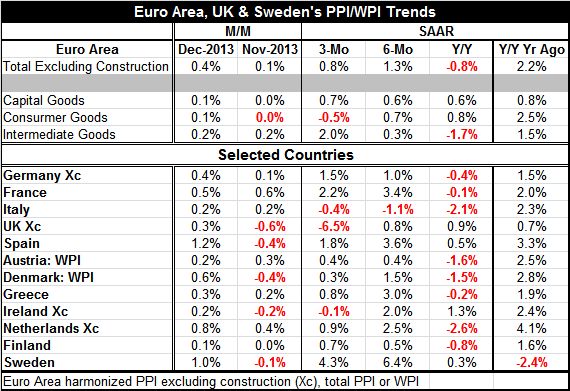

Inflation in the euro area continues to be mild. The total for the PPI-excluding-construction rose by 0.4% in December; that was a hearty pace by recent standards. However, it follows a 0.1% increase in November and the three-month rate annualized is only 0.8%. Over six months the euro zone PPI excluding construction is up at a 1.3% annual rate; over 12 months it is falling by 0.8%. Inflation and its trend remain damped.

Inflation in the euro area continues to be mild. The total for the PPI-excluding-construction rose by 0.4% in December; that was a hearty pace by recent standards. However, it follows a 0.1% increase in November and the three-month rate annualized is only 0.8%. Over six months the euro zone PPI excluding construction is up at a 1.3% annual rate; over 12 months it is falling by 0.8%. Inflation and its trend remain damped.

Consumer prices the in the euro zone are also well-contained and more clearly decelerating. The consumer metric is more important from the standpoint making policy at the European Central Bank. Bond yields in the euro zone are starting to move lower on the notion that some stimulative policy response to continued low and falling inflation may be in line from the ECB. Is it?

The PPI details show us that capital goods inflation is only a 0.6% over the last year. Consumer goods prices are up by 0.8% and intermediate goods prices down by 1.7%. The three- and six- month trends for inflation show fairly steady inflation for capital goods, while consumer goods pressures have declined and consumer goods prices are falling on balance over three months. Although intermediate goods are lower year-over-year, over three months they accelerated to a 2% pace. Intermediate goods have the highest content of raw materials of any the pricing categories and therefore show the most volatility (see chart).

Looking across the euro zone countries, interestingly, none posted PPI declines in December compared to November. But in November there had been declines in five of the 12 countries in the table, three of them being members of the European Monetary Union. Year-over-year inflation is falling on these PPI and WPI metrics in all but four countries; over six months only one country showed a decline, but over three months three countries showed declines in their PPIs.

The news on inflation from the PPI is mixed. Prices are more volatile than are CPI prices and they are more prone to erratic movements. The December data are little bit more suggestive that prices maybe firming, but looking at trends over three-months, six-months and one-year, that conclusion doesn't seem warranted.

Although the manufacturing PMI data released yesterday seem to show a solid rebound in January compared to December, data generally continue to show erratic readings from the various euro zone members. Today German orders for engineering products reported by the trade group VDMA showed a sharp drop in German orders at the end of the year. Although Spain has started to show some growth in its GDP, that growth has been week. In its employment report today, unemployment continues to advance in Spain in December.

Italy is seeing weaker price trends, but it is already a weak economy; for once, seeing inflation turn down in Italy may not be a good sign.

Inflation is only making clear progressive gains in Germany, Finland and Sweden. In Germany the year-over-year rate of -0.4% moves up to 1% over six months and 1.5% over three months. In Sweden the progression is unclear, but the pattern is still suggestive since year-over-year inflation is at 0.3%; six-month inflation rises to a 6.4% pace; and three-month inflation ticks `back down' to a still-strong a 4.3%. That is the highest pace in the table for any country over three months. Finland shows a true progression with inflation moving up from -0.8% over 12 months, +0.5% over six months and to +0.7% over three months. In the case of Finland it is a clear progression, but it is also clearly a slow rise to a three month pace that is not very ominous.

Along with Italy, the UK shows a progression of inflation rates to lower levels from 0.9% over 12 months, to 0.8% over six months and to a pace of -6.5% over three months. This trend is in an economy that has been showing rapid growth. Finland has the seventh slowest PPI rise over three months (in the table) despite that progression.

Inflation containment in -and around- the euro zone is impressive. The euro zone inflation rates are so compressed that over three months the highest inflation rate anywhere is 4.3%. But that is in non-member Sweden and the second-highest rate is 2.2% in France. Over six months the highest rate is 6.4% again in non-member Sweden followed by 3.6% in Spain. Over 12 months the highest inflation rate is 1.3% in Ireland followed by 0.9% in the UK (non-single currency participant). These summary statistics tell us that over six months inflation appeared to be making some come back, but over three months the pressures that seemed to emerge have gone away again.

The real question is how policymakers will view these metrics and perceive these trends. Year-over-year inflation rates are well below ECB-mandated marks (which apply to the CPI) and they are still preponderantly negative. Three- and six-month inflation rates show a little more tendency for inflation to rise, but the paces are still contained; also the change in inflation's pace from six-months to three-months is still quite suppressed. Will the policymakers look at this and think there's something wrong with the economy and that the central bank has more to do? That is a viable question for policymakers.

Inflation has been well within the zone prescribed by the ECB for some time. At the moment, the PPI is showing a decline over 12 months. For the targeted harmonized index of consumer prices (HICP) inflation is up by only 0.8% over 12-months and it is decelerating over six months and over three months to an even lower pace. It is definitely an environment where the ECB could decide that it has some work to do to boost inflation closer to its 2% mark (applicable to the HICP). It is also a situation where the central bank could play wait-and-see.

Moreover, it is not exactly as though the traditional high inflation countries in the euro zone are leading the parade. Countries like Spain and Italy continue to show suppressed inflation in their PPI and CPI trends. Both Italy and Spain have a smaller rises in inflation over 12 months than does Germany.

The ECB has some thinking to do. We know it is planning relatively strict-seeming stress tests for the banks in the euro zone. It's not possible to think in the wake of those requirements and tests that lending is going to loosen up at all. Maybe more help is needed?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief