Global| Mar 26 2008

Global| Mar 26 2008EMU Orders Rise in January but Trends Point Lower

Summary

It may not be resiliency as much as volatility as the rise in January EMU orders still shows growth rates steadily declining from 12 months to 6 months to 3 months. In the current quarter despite the bump up in January orders are only [...]

It may not be resiliency as much as volatility as the rise in January EMU orders still shows growth rates steadily declining from 12 months to 6 months to 3 months. In the current quarter despite the bump up in January orders are only rising at a 1.2% annual rate over Q4. Still, other more ‘timely’ data tell a better resiliency story.

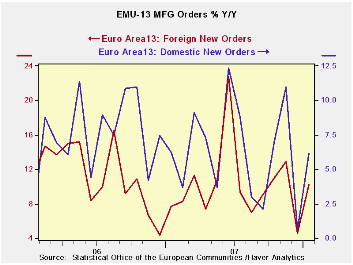

Total domestic orders show the same steady deceleration in orders as overall orders with the recent three-month order growth rate at a -3.7$ saar. Foreign MFG orders do not show the clear slowdown of overall orders, but that is a bit of nitpicking since the 6-month growth rate is about the same as the 12-month pace and the recent 3-month growth rate is about half of those rates at 5.5%. The Euro Area does seem to be slowing domestically and, despite the strength of the euro, foreign growth is keeping the EMU stronger.

Germany and Italy show withering order trends. France is consistent with a slowdown. Only the UK is different on a jump in orders in January that has sent the three-month growth rate soaring.

On balance though, the ECB and EU Commission seem still very worried about the level of the euro. But the German IFO index has risen again in March and the new Belgian Bank index for March also has shown growth for the second month running. This domestic resilience was not expected.

Data and Policy Conundrums… The

orders data tell us that domestic orders are in a slowing pattern. The

strength has come from orders outside the EMU. Now some new measures

are showing that there may be some domestic resiliency in February and

March in Germany and Belgium. None of this will make the ECB ready to

reverse its course and cut rates anytime soon. It makes you wonder if

the euro really does have more upside, something I have been unwilling

to ponder up to now. Is

Europe swallowing its teeth to hide the euro’s damage to its economy?

Or is Europe really this resilient? If Europe is this resilient, the

ECB’s carping about inflation risk makes sense, but complaining about

‘euro strength and excessive FX volatility’ does not make sense. Which

is it?

| Euro Area and UK Industrial Orders & Sales Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| SAAR except M/M | % m/m | Jan-08 | Jan-08 | Jan-08 | Jan-07 | Jan-06 | Qtr-2 Date |

||

| Euro Area Detail | Jan-08 | Dec-07 | Nov-07 | 3-Mo | 6-mo | 12-mo | 12-mo | 12-mo | Saar |

| MFG Orders | 2.0% | -3.6% | 2.0% | 1.2% | 3.6% | 6.7% | 7.7% | 6.7% | 1.2% |

| MFG Sales | 0.8% | 0.3% | 0.0% | 4.6% | 1.8% | 4.1% | 7.2% | 6.5% | 6.3% |

| Consumer | 0.3% | 0.3% | 0.2% | 3.1% | 2.9% | 3.4% | 7.2% | 6.5% | 3.3% |

| Capital | 0.4% | 0.1% | 0.0% | 1.6% | 2.4% | 4.6% | 4.7% | 3.4% | 2.4% |

| Intermediate | 1.1% | 0.5% | 0.2% | -3.7% | -0.4% | 6.2% | 8.4% | 6.0% | 9.2% |

| MFG Orders | |||||||||

| Total Orders | 2.0% | -3.6% | 2.0% | 1.2% | 3.6% | 6.7% | 7.7% | 6.7% | 1.2% |

| EA13 Domestic MFG orders | 1.6% | -4.3% | 1.8% | -3.7% | -0.4% | 6.2% | 6.2% | 1.6% | -4.2% |

| EA13 Foreign MFG orders | 3.3% | -5.4% | 3.7% | 5.5% | 11.3% | 10.2% | 7.8% | 11.2% | 4.7% |

| Countries: | Jan-08 | Dec-07 | Nov-07 | 3-Mo | 6-mo | 12-mo | 12-mo | 12-mo | Qtr-2 Date |

| Germany: | -1.1% | -1.5% | 3.5% | 3.5% | 9.4% | 9.3% | 9.2% | 8.6% | -5.5% |

| France: | 3.1% | -2.1% | -0.2% | 3.0% | -2.7% | 5.9% | 5.1% | 7.8% | 10.1% |

| Italy | 2.6% | -5.6% | 2.9% | -1.0% | -3.0% | 7.2% | 4.6% | 9.0% | -1.8% |

| UK (EU) | 23.0% | -1.3% | 4.0% | 154.7% | -4.6% | 31.1% | 10.1% | -8.8% | 255.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.