Global| Sep 26 2019

Global| Sep 26 2019EMU Money Supply Steps Up Its Pace; Credit Growth Continues to Trend Slowly Higher

Summary

Money and credit trends in the EMU are on the upswing and are encouraging. Money growth is almost as strong as it was at its peak pace earlier in this recovery period. Of course, the last time money growth perked up to this pace it [...]

Money and credit trends in the EMU are on the upswing and are encouraging. Money growth is almost as strong as it was at its peak pace earlier in this recovery period. Of course, the last time money growth perked up to this pace it then decelerated and there was no economic pick-up. However, this time the rise in the money growth rate is buttressed by an ongoing rise in credit growth.

Money and credit trends in the EMU are on the upswing and are encouraging. Money growth is almost as strong as it was at its peak pace earlier in this recovery period. Of course, the last time money growth perked up to this pace it then decelerated and there was no economic pick-up. However, this time the rise in the money growth rate is buttressed by an ongoing rise in credit growth.

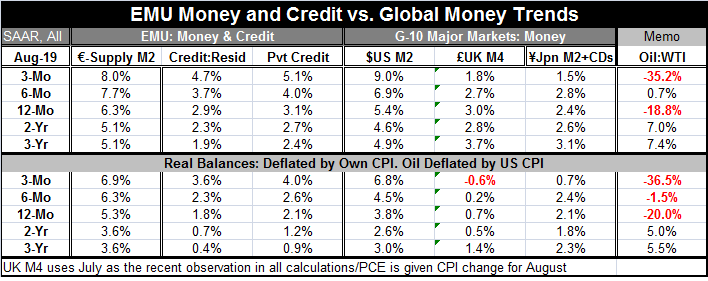

The money growth (M2) has in fact risen from 5.1% over three years and two years to 6.3% over one year and that is now up to an 8% pace over three months. The 8% rate is quite strong-even excessive - money growth and should not be sustained. The question is whether this is a stimulating transactional demand for money balances or the demand for extra liquidity because of heightened uncertainty. So the ramp up in demand that is strong may or may not be significant for growth and its impact could be in either a positive or negative fashion on growth depending on the reason for its emergence.

Credit growth has picked up from 1.9% over three years to 2.3% over two years and to 2.9% over one year. Over three months, growth is up to 4.7%. Private credit has similarly evolved.

Real (inflation deflated) data on money and credit also have showed a step up. Over the past year real money growth is up to 5.3%. Total credit is growing at a 1.8% pace and at a 2.1% pace for private credit. Over this period inflation is on the decline, that tends to bolster the growth rate of the series that inflation is used to deflate.

Global money supply shows a step up of money growth in the United States and the EMU. In Japan nominal money growth still seems to be decelerating while in the United Kingdom money growth has declined and has been waffling in a range of low growth rates.

Global money supply shows a step up of money growth in the United States and the EMU. In Japan nominal money growth still seems to be decelerating while in the United Kingdom money growth has declined and has been waffling in a range of low growth rates.

In real terms, U.K. money growth is mired in a crawl near zero growth. Japan's M2 plus CDs measure continues to meander around the 2% level since end-2017. From late last year for the EMU and from about March of this year, real money balances have been accelerating in both the U.S. and the EMU.

However, during this period what has been observed is a weakening of economic conditions in Europe and the adoption by the ECB of special stimulus to the extent it is able. Even though the ECB has a singular objective to manage inflation so that it is just below the 2% mark, the ECB has not been able to accomplish that…and some members have opposed steps that might help the ECB to hit its target.

All of these central banks aim at a 2% inflation target and none of them has been hitting it. The ECB has only one objective to keep inflation just under 2% and it has seen inflation above 2% only 4 times since February 2013 and inflation is currently too low and decelerating. Yet 9 members of the ECB executive committee resisted and opposed the ECBs recent stimulus plan. One German member, Sabine Lautenschläger, has quit because she cannot abide by the new stimulative policies but was apparently unaffected by the bank's loss in credibility after six years of not being able to reach its inflation objective with any consistency.

This episode is a very good example of the problem that the ECB encounters in making policy. Hard money rules–oriented German members and Germany itself have thrown up barrier after barrier to the ECB's attempt to create stimulus often delaying it to the point where it became effective even when adopted. The German have questioned everything as possibly inconsistent with the ECB's charter. Yet, what the ECB has so far done the most poorly is to achieve its one and only mandate: just under 2% inflation. The German economy is much more geared to perform at low inflation rates than other EMU economies. Even so Germany is now on the brink of recession. Italy has yet to achieve its pre-financial crisis level of real GDP of over 10 years ago (!). While unemployment rates across the EMU have fallen, there remains a lot to be done in Europe and there is ample evidence of fading growth. Welcome to the "euro area." Make no mistake about it. This 'zone' is about the euro, the currency. The 'euro' in euro Area does not stand for Europe; it stands for euro. As far the Germans are concerned, everything should be done to preserve the level of the euro…whatever the cost. But I don't think it actually says that in the ECB charter.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief