Global| Aug 28 2017

Global| Aug 28 2017EMU Money Supply Is Flat and Credit Growth Is Off Peak

Summary

In the wake of the Federal Reserve's monetary conclave in the wilds of Jackson Hole Wyoming (albeit 'wilds' with room service), we find that global monetary conditions remain as they have been. This, of course, is not surprising since [...]

In the wake of the Federal Reserve's monetary conclave in the wilds of Jackson Hole Wyoming (albeit 'wilds' with room service), we find that global monetary conditions remain as they have been. This, of course, is not surprising since the Jackson Hole meeting is not one for action nor is it one where policy is usually changed. This year Jackson Hole was less about action than any other time in the past. Janet Yellen attended and spoke and managed to say nothing at all about policy. Mario Draghi noted that inflation was still absent and patience still a virtue. The BOJ's Haruhiko Kuroda emphasized that inflation targeting was still important in Japan and that he has no plans to seek a different target.

In the wake of the Federal Reserve's monetary conclave in the wilds of Jackson Hole Wyoming (albeit 'wilds' with room service), we find that global monetary conditions remain as they have been. This, of course, is not surprising since the Jackson Hole meeting is not one for action nor is it one where policy is usually changed. This year Jackson Hole was less about action than any other time in the past. Janet Yellen attended and spoke and managed to say nothing at all about policy. Mario Draghi noted that inflation was still absent and patience still a virtue. The BOJ's Haruhiko Kuroda emphasized that inflation targeting was still important in Japan and that he has no plans to seek a different target.

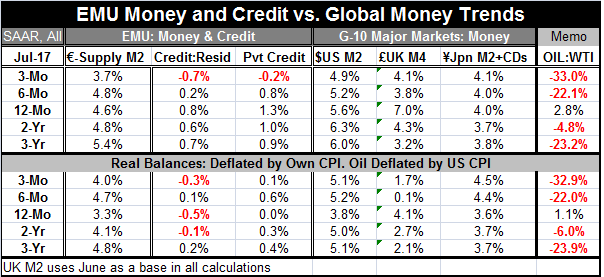

So this year the 'wake' from the speed boat 'Jackson Hole' is a small one. As we see in the table credit to residents and private credit in EMU are both contracting over the most recent three months. The growth rate of these two credit aggregates is only somewhat slower that recent growth rates going back a year or two. In other words, despite Mr. Draghi's willingness to paint a positive picture of the impact of the new monetary tools, they have not boosted credit growth rates. However, they still may be instrumental in holding them aloft, even at their current low trajectories. This is why it is hard to know what impact these tools have and why it may yet be too risky to dismantle these programs soon. When you do not really know fully how something works (as Mr. Draghi claims is the case with neo-monetary policy), it is hard to know what its actual contributions really are.

Only the Fed seems ready to stand up tall and let the bullets bounce off its chest. The Fed is confident that now is the time to hike (to keep hiking) rates despite inflation's undershooting. The Fed's bet is that hiking rates is not wrong since hiked rates are still below their long-term neutral position. By this approach monetary policy is still 'stimulative.' But it is not as stimulative as it would be if rates were not hiked. And there is the matter of 'r-star' a concept the Fed has not been very vocal about recently as this concept suggests that there is some sort of dynamic shift in the economy so that interest rates at this low level are not as stimulative as they might be normal times. The concept of r-star actually muddles the Fed's comment that rates are still accommodative because they are below their long-term neutral value. On closer inspection, that juxtaposition is irrelevant. The r-start paradigm gives the Fed an excuse for why rates are so low and yet have been so without impact. Yet, the 'r-star' framework also suggests that rates should stay low (maybe even that they should have stayed lower) if the objective has been to stimulate the economy and not just be at a 'dynamic neutral.' This in turn explains why inflation has not risen. It's because the Fed has been more or less tracking the series 'r-star' with policy; it has been hiking rates to prevent greater stimulus and inflation through. Note that it is the relationship of current rates to r-star not to the long-term neutral rate that matters in this assessment.

Still, whether at the Fed in the U.S. or on the ECB board, there remain people who fear a surge in inflation. The traditionalists are concerned about not having learned the lessons of the past. Yet, the question is this: is having learned the lessons of the past keeping those members from learning the new lessons of the modern economy and of the future? Who is right? Is inflation at risk because of a period in which rates have been too low for too long? Or has inflation still not been low enough for long enough because of the shift to the new normal? These obviously are very different things to consider.

In addition, there is the question of how we come to know the impact of policy on the economy given Draghi's view that the new procedures are still a mystery. One way to tell is in 'real time.' Of course, hawks think that real time is too late since once inflation gets rolling it always overshoots. The view that monetary policy works with lags and sometimes long ones puts inflation hawks on cautious footing regardless of current data. But since current data also show a chronic inflation undershoot anyone thinking that the 'new normal' has pushed back on inflation in such a way that it is no longer prone to rise sharply again as it did in the past also has some solid ground to stand on. The upshot is that there is a lot of monetary policy being made with voters looking over their shoulder. Monetary policy voters, whether at the BOE, the ECB, the Fed or the BOJ have very divided views on the risks because of the differences in these paradigms. And the fact the inflation has stayed low globally does not seem to sway traditionalists.

Since there is a parallel concern than rates that have been so low for so long also might engender financial instability, there has been a third group that has sort of swung policy in the U.S. (at least) to being less accommodative because of concerns about rising financial market instability risks. In Europe, those sorts of concerns have not yet carried the day when it's time to vote for policy. But it is only fair to say that policy-making is very much in flux in all the major money centers. Each has its own form of inertia. And it is far from clear that that inertia has changed at all over the past few months even though markets seem to think change is on the doorstep. There is a lot of study and questioning about the state of policy, but at the end of the day monetary policy-making requires at least as much interpretative art as science. And for now, it is hard to know just where central bankers stand because there are so many different beliefs and voting factions among the members of the various key central banks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief