Global| Jan 26 2018

Global| Jan 26 2018EMU Money, Credit Growth and Trade

Summary

While optimism about growth is moving ahead in leaps and bounds and many are concerned that monetary policy has overstayed its welcome on the side of accommodation, the monetary measures themselves show a much more muted view of this [...]

While optimism about growth is moving ahead in leaps and bounds and many are concerned that monetary policy has overstayed its welcome on the side of accommodation, the monetary measures themselves show a much more muted view of this process. Judging from the low level of interest rates, there is a good deal of angst about monetary policy being far too stimulative. But if that risk is real, how does that process work; does it circumvent money and credit flows?

While optimism about growth is moving ahead in leaps and bounds and many are concerned that monetary policy has overstayed its welcome on the side of accommodation, the monetary measures themselves show a much more muted view of this process. Judging from the low level of interest rates, there is a good deal of angst about monetary policy being far too stimulative. But if that risk is real, how does that process work; does it circumvent money and credit flows?

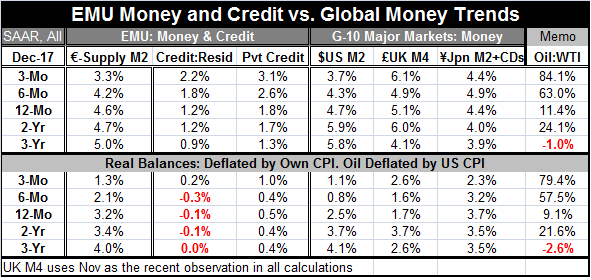

As we look at money and credit growth rates in the EMU, we are struck by the mild and even tepid trends for both the growth rate in the quantity of money and for the growth rate on the quantity of credit. Neither of them seems to be progressing too briskly. It does not look like excessive accommodation is working its way through these channels.

Year-on-year money growth is 4.6% which is lower than over the previous 12 months and lower than the 12 months previous to that. Credit growth is picking up over three years, it averages 1.3% over two years, then it pops up to 1.7%, and now over the most recent 12 months it is up at a 1.8% annual rate; an acceleration in technical terms only.

In the great scheme of things (see the chart above), money and credit growth are both listless. Money growth appears to still be a part of a broader deceleration and credit growth has a slight hint of pick up. But turning our attention to real money and credit flows reveals a deceleration in real money balances and an ongoing contraction in total credit with private sector credit really stuck in the 0.4% to 0.5% range for annual growth. That's annual growth in real credit of one half of one percentage point or less. That hardly looks excessive.

From the financial sector to the real sector

Yes, it really seems that Europe is jumping out of its skin and from these data very clearly excessive monetary accommodation is the reason. All sarcasm aside, interest rates are still very low and real rates are clearly negative for a number of instruments. But the actual economic performance we observe is in part the result of the monetary conditions we report above and the low interest rates. In other words, with all this accommodation from low interest rates, other financial metrics really are not responding. But there is some pick up in the real economy and PMI data seem to be exceptionally strong.

In earlier reports I have looked at the PMI data and I have demonstrated that both for the EMU and for the U.S., the relationship between the PMI gauges and the IP has shifted in such a way that PMI strength is no longer such an accurate barometer of what industrial output will do. Still, consumer spending is positive in Europe and strong in the U.S. Consumer confidence is up on a broad front, not just for the EMU but within the EMU in various local country markets. The presence of consumer optimism is a very important signal.

Financial markets have been reinforcing growth. Stocks, especially in the U.S., had an outstanding year last year. The Trump tax cuts were pushed through. While the economic revival may be somewhat exaggerated by PMI data, the Q4 GDP report today for the U.S. shows solid growth and a step-up in the growth rate for both exports and imports. The U.K., an economy that has long seemed ready to slowdown, failed to do that yet again as U.K. growth in Q4 has speeded up. The U.K. continues to buck the slowdown trend that has been broadly expected in the wake of the Brexit vote.

Growth is restarting globally. We can see it in the growth of global imports and exports which are finally growing faster than GDP for the first time since 2012 (see the G-20 chart). Exports and imports customarily outpace GDP growth. But this feature had been absent until last year when global trade flows began to stir. It is a sign of progress toward normalcy, but some will also be wary about the impact of a new more aggressive U.S. posture toward trade.

Growth is restarting globally. We can see it in the growth of global imports and exports which are finally growing faster than GDP for the first time since 2012 (see the G-20 chart). Exports and imports customarily outpace GDP growth. But this feature had been absent until last year when global trade flows began to stir. It is a sign of progress toward normalcy, but some will also be wary about the impact of a new more aggressive U.S. posture toward trade.

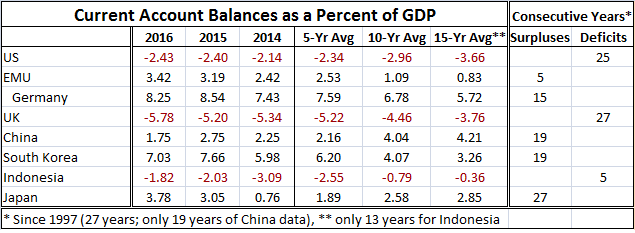

And while defenders of free trade and proponents of global growth like the second chart, the table below is a more difficult challenge for them. The table reminds us that while global trade may be an engine of global growth, it is also an engine of redistribution. The table shows eight countries/regions. Among them, only the EMU and Indonesia have had relatively short experiences with persistent deficits/surpluses ('short' in this case meaning five years). Apart from them, Germany, China, South Korea and Japan have run unrelenting surpluses for periods ranging from 15 to 27 years. The U.S. and the U.K., the two countries very committed to free trade, have suffered unrelenting deficits for 25 to 27 years. Trade has persistently weakened the U.S. and the U.K. and boosted growth in Germany, China, South Korea and Japan. Exchange rates have not moved to offset deficits and surpluses for periods spanning a generation or more! Donald Trump in the U.S. is not opposed to free trade but to this structural mercantilism that creates persistent winners and losers by not letting exchange rates adjust or by using more subtle trade distorting practices. Mr. Trump may be volatile, loud and sometimes quite out of control. But on the issue of trade, he has a very powerful point. And while the rest of the world wants to sound sanctimonious about it, the fact is that the U.S. still stands on the moral higher ground. U.S. market has been more open and there are fewer nontariff and other restrictions and there has been a commitment to free trade. Trump is now trying to make sure that that trade is a two-way street. Since so much of global investment already is based upon the goods trade patterns memorialized in the table, you can imagine that Trump's view rocks more than a few boats. That does not necessarily make him wrong.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief