Global| Aug 28 2018

Global| Aug 28 2018EMU Monetary Stimulus Is Just Not Taking

Summary

As central bankers have been acting, planning and pondering their next move, all of them are on the road or on the tilt to reduced monetary stimulus. The Fed in the U.S. is the farthest along that trail with some 7-notches on its [...]

As central bankers have been acting, planning and pondering their next move, all of them are on the road or on the tilt to reduced monetary stimulus. The Fed in the U.S. is the farthest along that trail with some 7-notches on its belt. The BOE also is hiking rates. The Fed, in addition for concerted rate-hiking, is reducing the size of its balance sheet. Japan has announced a plan to allow more variability in its 10-year note peg, a shift that most see as a way for the BOJ to leg its way out of its zero rate peg for that maturity. The ECB is still in the planning stages for its exit.

As central bankers have been acting, planning and pondering their next move, all of them are on the road or on the tilt to reduced monetary stimulus. The Fed in the U.S. is the farthest along that trail with some 7-notches on its belt. The BOE also is hiking rates. The Fed, in addition for concerted rate-hiking, is reducing the size of its balance sheet. Japan has announced a plan to allow more variability in its 10-year note peg, a shift that most see as a way for the BOJ to leg its way out of its zero rate peg for that maturity. The ECB is still in the planning stages for its exit.

If it’s stimulus, what isn’t it stimulating?

The degree of monetary stimulus taken in the form of central bank asset purchases and in terms of the low nominal and real rates, both of which that have been endured worldwide, are stunning for their lack of impact on real growth and on inflation. Growth during this period has been nurtured back into existence. But no one would call it ‘strong.’ Because of the advanced stage of the business cycle that would be asking too much now, but in this cycle with gobs of stimulus, growth has never been ‘strong’ anywhere. And Inflation is still MIA (Missing In-spite-of Accommodation). Economists of the 1970s and 1980s would be stunned by this result. Had you been a graduate student in economics anywhere back then and had you tried to write a paper about how this would happen, you would today be operating a cash register at Wal-Mart – or at least not having any career as an economist.

Flummoxed by the facts

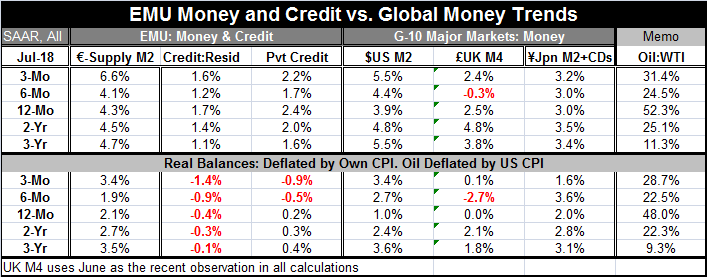

Indeed, modern day economists, too, remain flummoxed by the lack of impact from monetary policy and just to prove it they remain disbelievers and are at this very moment worried as can be that the forces of inflation are regrouping and planning an attack that will drive the inflation rate up and force central banks to pull out the stops and act more aggressively with a likely deleterious impact on growth. However, despite what can be characterized as excessive ‘monetary stimulus’ during the period since the financial crisis, money supply growth itself in the key monetary center countries has largely remained well-behaved and right now money growth rates are still moving lower.

Year-on-year nominal money growth rates largely erode

Year-on-year nominal money growth rates largely erode

Fixed fears!

So it is no wonder that inflation expectations on the part of monetary officials are rising? (huh?) Inflation expectations by market participants, however, are not rising. In the U.S., the yield curve is flattening, a well-known and highly reliable signal of recession that makes inflation a less likely event should the yield curve actually invert. And yet the Fed is crazy-glued™ to its tightening path.

Germany: the outlier

In Europe, the Germans are all but apoplectic of the degree of stimulus in play and the length of time that it has been there. Of course, Germany is carrying more inflation than most EMU members largely because Germany has had a post reunification low in its unemployment rate for many months now. And to Germans, even low inflation rates can seem high. Even though we think of central banks as targeting 2% inflation, the ECB targets a rate just below 2%- just to put that added measure of intolerance in there.

What good is it? What bad is it?

For all of the stimulus in the EMU, money growth remains moderate and credit and loan growth which stopped falling in 2015 still are not really advancing when expressed in real terms. So if ‘excessive monetary stimulus cannot get money or credit growth in gear, what good is it – and what ‘bad’ is it (what sort of bad effects can it generate?)?

The bad and ugly without ‘the good’

There is rising concern that monetary stimulus (in this case than means low interest rates) contributes to financial sector risk even though it is not stimulating much real sector activity. And for the moment, that view seems to be a dominant one and it is one of the driving forces to put monetary policy back ‘where it belongs.’ But no one knows where that is.

A place for everything and everything in its place...your place or mine?

If excessive monetary policy stimulus is not a stimulant, can we conclude that monetary policy does not matter and that we can raise rates and go back to old standards without any adverse impact? Or is the anemic reaction to excessive stimulus an indication of a still-needy economy and will taking rates back to old benchmarks prove to be an excessive tightening for policy in this new environment?

Never let the facts get in the way of a good opinion

There is hardly anyway to know. But policymakers have opinions and some of them have very strong opinions on this.

Think but also LOOK

Interest rate levels still have the potential to move exchange rates in the real world and we are seeing that interest rates also have an impact on the housing market. And they have impact in the financial sector itself in various ways. So rising interest rates are going to have an economic impact; it’s just not clear that they will have the impact that is expected or desired. I simply hope that whatever choice monetary officials make they do not move too fast and they do keep their eyes AND THEIR MINDS open to what actually happens. It is not a time to let dogma trump reality. Reality has been too unpredictable for us to think we really understand it or can predict it. Against that background, policy calls for economists who are grounded in reality not immersed in dogma.

Oh captain, my captain

While many think the time is due or overdue to have a German at the head of the ECB, I wonder if it isn’t too soon to install someone who has the inflexible position on monetary policy that is taught in Germany. For one thing, the EMU is not Germany. Things that can be done in Germany cannot as easily be pulled off in the EMU. I have always believed that the economic and monetary structure of country (or region) was in some way tailored to the societal values. Things that policy can do in Germany, Finland, Sweden and Norway (yes the last two are not EMU members) cannot be done in Spain, Portugal, Italy and Greece. And it is not as simple as just imposing a new will or discipline. Italy and Greece are two different cases but clear examples of what excessive austerity can do. The Greek economy is still in shambles and Europe has not arranged any debt forgiveness just a debt payment moratorium that hangs over Greece like the sword of Damocles. Italy, under austerity, has been unable to return its GDP level to its pre-crisis standing after a decade of struggle. Some would call Italy a success because of its low inflation rate but how can that kind of growth (none!) be construed as a success?

There are lessons but has there been learning?

Europe still faces many challenges. The struggles with austerity should have been an eye opener. They weren’t. The severity of the crisis in Greece should have changed some views, but it didn’t. The ongoing struggle with migrants and Europe’s willingness to stuff the problem in the economies of its border countries is only becoming an eye opener because Italy’s new government has vowed not to take it anymore. The U.K. decided to leave the EU because of its intrusive and inflexible policies and the EU arrogantly viewed the British as ‘the problem.’ If the British were the problem, why do so many problems –many stemming from migrant issues- still linger and fester like the protest explosion in Germany just yesterday in Chemnitz? Europe is a place in denial. And denial does not solve problems. The issues surrounding monetary policy are only some of the things that Europeans must address. They have one monetary policy; yet, they are all are different and they have not yet figured out how to deal with it. Germans think the answer is to turn the Greeks, Italians and everyone else into Germans. Well that is not going to happen. Putting a German at the helm of the ECB at this time might just make things worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief