Global| Jun 29 2018

Global| Jun 29 2018EMU: Mixed Signals from the HICP; What Will the ECB Do Now?

Summary

For the second time in approximately one year, EMU area and large country inflation rates (HICP definition; year-over-year) are pushing up to, through, or over the key 2% mark (the ECB’s inflation objective is for inflation ‘a little [...]

For the second time in approximately one year, EMU area and large country inflation rates (HICP definition; year-over-year) are pushing up to, through, or over the key 2% mark (the ECB’s inflation objective is for inflation ‘a little less than 2%’ making the 2% level a ‘key’ level for inflation assessment).

For the second time in approximately one year, EMU area and large country inflation rates (HICP definition; year-over-year) are pushing up to, through, or over the key 2% mark (the ECB’s inflation objective is for inflation ‘a little less than 2%’ making the 2% level a ‘key’ level for inflation assessment).

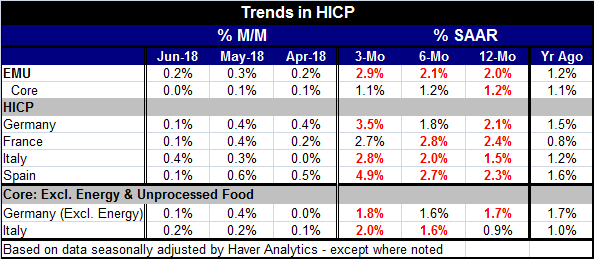

Inflation in the EMU is slightly excessive at 2% in June. Inflation in France is excessive at 2.4% so is Spain’s at 2.3%, and at 2.1% Germany’s inflation rate is also above the mark sought by the ECB for the EMU community as a whole. Only Italy, among the four largest EMU economics, has headline inflation at 1.5%, clearly below the ECB objective.

However, the reported core inflation rate for the EMU actually dipped from 1.3% in May to 1.2% in June. At 1.2%, it is well below the headline objective of a little less than 2%.

This puts the ECB in a bit of a sticky spot. Formally, the ECB aims to keep the headline pace at less than 2%. There is no separate objective or treatment for the core rate. But the core rate to any sensible person is a good double check on how and why inflation is doing what it is doing. Right now Europe is in a period in which oil prices have pushed up and they have carried the headline higher than they have had much impact on the core rate and a core-headline gap has opened up.

Still, over the years the Germans have been real sticklers for inflation rules: 2% is 2% and the headline is the headline. This sort of interpretation and inflexibility is made slightly worse now with Germany itself facing a slightly higher rate than the already excessive 2% pace for the EMU and with both France and Spain with inflation that is too high and that has accelerated.

The ECB, like the Fed, has an aspirational target for inflation. It aims at all times to try to control inflation to be inside its target. What that means is that price level targeting is not pursed in either the U.S. or EMU. Inflation misses of the past do not constrain or give flexibility to monetary policy in the future. So the persistent undershooting of the ECB target that you observe in the graph above is not relevant to making policy in the EMU. The chart shows about five years of persistent and protracted undershooting.

It is widely talked about that the next ECB head will probably be German. And with a German heading the ECB today, policy rates would probably already be higher. Indeed, Mario Draghi, himself, has been preparing the ECB to head for normalization.

The only question at hand is how rapidly Draghi’s hand might be forced now with EMU-wide inflation slightly above target and with pressures stirring for headline inflation in three of the four largest EMU economies.

I think we can make judgements from Mr. Draghi’s recent statements and past actions. While inflation may be in excess, it is in excess in only the most technical way. The past inflation undershooting may have no standing as a policy lever, but policy is made by people and the inflation hawks are not in the majority on the ECB board – nor is their case ‘fundamentally’ strong. This is not inflation cooking in an economy that is overheating with activity. Europe is engaged in a broad slowdown as the EU Commission sentiment indicators and the Markit sector diffusion indexes agree. While a narrow disciplined assessment of policy might find the time ‘right’ for the ECB to become more aggressive, I doubt that the ECB is going to step up its pace. Draghi wants to move gradually and technical issues aside all signs continue to point to the ECB as having some room to use discretion. It is dismantling tools of stimulus. It is moving in the right direction.

Of course, Germans will want the ECB to be more aggressive now and are already worried that their own domestic inflation rate has moved up over 2% a far cry from German past practice. Germans acquired a privileged competiveness spot in the EMU since its formation by persistently running the lowest inflation rate among members. Running one of the higher rates is not part of the German modus operandi. And that probably explains why Germany now is so dead set on running a fiscal surplus. Unable to control monetary policy since the ECB took over that task from the Bundesbank, Germany finds itself in a very slight excessive inflation condition. The last lever it has to pull is fiscal policy so it is running a contractionary fiscal policy to try to bleed the heat out of its domestic economy, the strongest economy in Europe with a historically low unemployment rate. And Germany feels strongly enough about this that it is unafraid to fall short in its contribution to NATO again in order to run this surplus.

Oil prices ebb and flow. Despite being at a point in the cycle when oil prices have ridden up and boosted the overall price level, the U.S. policy on Iran is likely to result in Iranian oil being taken off the market again and could result in yet another boost to oil prices. In that case, headline inflation in the EMU might not come down so quickly to or toward the pace of the core.

Policymaking in the EMU has become a stickier affair. Despite a lot of animosity generated among monetary hawks about the more stimulative things Mario Draghi has done while at the ECB, Europe has been able to weather a difficult recession and financial crisis as well as strains on the EU/EMU systems themselves. And Europe is recovering. Moreover, the ECB’s legacy on inflation is going to look extremely good from the standpoint of not overshooting its target to do so. Draghi would have to really let the inflation cat out of the bag in the coming months for his stewardship as head of the ECB to look like a failure. It is much more likely that he will be viewed as an innovator at a central bank that prides itself on living in the stone age and that his ability to have moved the ECB out of several well-worn ruts established by the Bundesbank on which the ECB is modeled will be seen as successes- but not by all.

The German influence on the ECB is the one thing every EMU member bought into when they joined-up. There may have been prevarication, but there was really not any dispute that the new currency area would look more like the Deutschemark area than like a blended currency zone. Still, the lack of any EMU-wide fiscal policy put extraordinary pressure on the EMU in the recession and financial crisis. And Germany took that opportunity to take fuller control and enforce long standing and much ignored fiscal rules; Germany also fought for strict interpretations of the ECB charter. And Europe paid a price for all that. But still Mario Draghi found a way to policy flexibility.

Draghi is in the twilight of this final year and in this period I do not look for him to change his spots. His view for a gradual restoration of normalcy continues to make sense. The technical overshoot of inflation in the EMU is not something to overact about. But it is going to increase tensions and pressures within the ECB. Draghi’s final days are not going to be a walk in the park- well maybe a German park guarded by Doberman Pincers, just to make sure he doesn’t stray.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief