Global| May 09 2018

Global| May 09 2018EMU Members Show IP Rebound Amid Weakening Trends

Summary

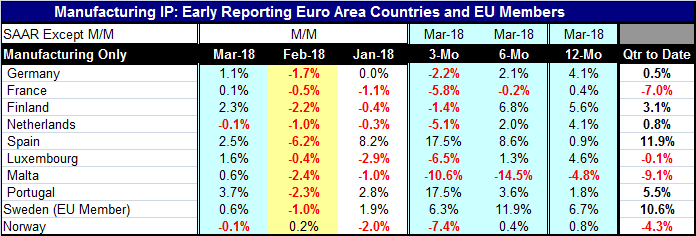

Manufacturing industrial output among eight early reporting EMU members (plus Sweden and Norway) showed only two declines in the group in March. IP edged lower by 0.1% in the Netherlands and Norway. Everywhere else in the table there [...]

Manufacturing industrial output among eight early reporting EMU members (plus Sweden and Norway) showed only two declines in the group in March. IP edged lower by 0.1% in the Netherlands and Norway. Everywhere else in the table there were output increases for manufacturing. However, this same sample of countries showed declines everywhere up and down the line except in Norway last month. Finland, Luxembourg, Portugal and Norway are the only countries out of the ten in the table with net IP gains over the last two months. Despite the broad rebound in March, IP is not yet on solid footing.

Manufacturing industrial output among eight early reporting EMU members (plus Sweden and Norway) showed only two declines in the group in March. IP edged lower by 0.1% in the Netherlands and Norway. Everywhere else in the table there were output increases for manufacturing. However, this same sample of countries showed declines everywhere up and down the line except in Norway last month. Finland, Luxembourg, Portugal and Norway are the only countries out of the ten in the table with net IP gains over the last two months. Despite the broad rebound in March, IP is not yet on solid footing.

Three-month growth rates find output declines in seven countries, six of them EMU members. However, over six months IP declined only in tiny Malta and in France. Over 12 months only Malta showed an IP drop, but both EMU members France and Spain log IP increases of less than 1% (along with Norway).Year-on-year as well as over six months, this group of countries is still growing. Is the recent weakness just a more rapid return to a sustainable trend or is it something worrisome?

Output is moderating in the EMU and we can see that in the trends above. We know it from other country-level reports and from the Markit PMI data. In addition with the U.S. hiking rates, there has come to be some pressures in emerging country markets. Argentina with interest rates that have surged up to 40% is an example. The question might be asked who or what will drive growth in the period ahead?

Interest rates are rising in the U.S. and in the U.K. The ECB is contemplating changes. Japan is one step removed from that process. The new monetary profile has had the effect of causing market participants to look ahead and reevaluate the landscape. This reevaluation has consequences.

In a recent speech, Fed Chairman Powell has sought to take the Fed’s fingerprints off of any market repercussions that might have developed abroad as the Fed has begun to raise rates. In the end, there is no getting around the fact that the Fed will set an important base rate and other countries will have to decide how to price their rates around it.

The Federal Reserve does not want to bear the blame for the fall out from things that happen in overseas markets but just as surely its ‘plan’ to steer the Fed funds rate to ‘neutral’ and its policy discussion to markets that they will have to prepare for an above neutral Fed funds rate cannot help but create instabilities abroad. Monetary policy more generally, will interact with the world economy according to the state that it is in. If the Fed is going to dictate the business cycle, then those things that happen in the business cycle will be dictated as well. These things include bond market yields commodity prices and exchange rate movements.

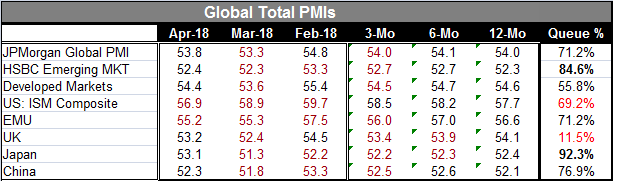

The table below shows composite PMIs. Japan with a relatively low diffusion reading, nonetheless, has the relative strongest queue standing in April (its relative strength vs. its own history of the past five years). That standing is followed by emerging markets. Developed markets have fallen to a ranking in their 55th percentile, barely above 50 which marks their median reading over the last five years. The U.K. with its Brexit issues is especially lagging while China, the U.S. and EMU have similar middling standings. Moreover, the U.S. and EMU all show three months of PMI weakening in a row. Emerging markets nearly do the same. Upward momentum is no longer an attribute of the global economy. There is growth but not acceleration. And there is monetary policy tightening... and more to come.

The U.S. and EMU may be in a position to hold up well to a hike in rates since their PMIs are relatively elevated. But they already are losing momentum. There is no getting out from under the fact that higher interest rates in the main monetary center countries will spread internationally and that business cycle effects will spread and be magnified across markets and to countries of all stages of development. All this is just another reason for central bankers to be sure of what they are doing when they move. Currently, OECD-area inflation continues to hover around the 2% mark which is the standard for central bankers these days. Where will more inflation come from? Despite global tightness, there is little evidence that it is spreading out of the labor markets. Where will continued growth come from? Can the global economy bear up under higher rates? Interest rate levels seem low compared to past standards, but then my third grade clothes looked small once I got to 7th grade. Are past standards applicable to the economy today? Are central bankers being responsible for wanting to put rates back at historic norms or is that wholly irresponsible? These questions have answers but perhaps not until we try them on for size. And the fitting could prove to be painful.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief