Global| Jul 26 2019

Global| Jul 26 2019EMU Member PPI Trends...and the U.K.

Summary

PPI developments once again underscore that inflation pressure is not building in the EMU. Mario Draghi is getting progressively more concerned about the European situation and condition. Draghi's term is coming to an end and he is [...]

PPI developments once again underscore that inflation pressure is not building in the EMU. Mario Draghi is getting progressively more concerned about the European situation and condition. Draghi's term is coming to an end and he is trying to prepare the way for his successor Christine Lagarde.

PPI developments once again underscore that inflation pressure is not building in the EMU. Mario Draghi is getting progressively more concerned about the European situation and condition. Draghi's term is coming to an end and he is trying to prepare the way for his successor Christine Lagarde.

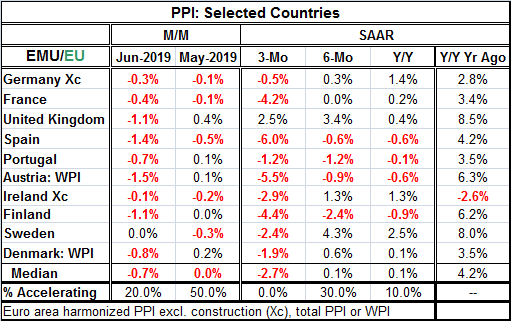

EMU inflation is not yet formalized, but with the availability of the French PPI today three of the big four EMU members' data are in hand. Germany, France and Spain show PPI declines in June and July as well as over three months on balance. Spain logs declines over 12 months, six months and three months. Germany and France show PPI gains over 12 months and six months but both show sequential slowing in the annualized PPI pace from 12-months to six-months to three-months. PPI disinflation is well in gear. For the moment, the 10-country sample shows inflation is well contained and decelerating across most fronts.

The U.K., still an EU member, is an exception. That's why with other central banks are in a rate cutting regime or on the doorstep of one, while the U.K. is on a different trajectory. The U.K. PPI is falling sharply in June. It is, however, making gains over 12 months, six months and three months. But it is not accelerating on that timeline. Still, the U.K. PPI tells a story of a different situation for the U.K. than for the EMU or for the rest of the world.

Brexit is going to be a difficult policy dilemma for the ECB and the BOE. Unfortunately, the EU and the U.K. governments are not really focused on transition issues but are concerned about other things. The EU may be too concerned about precedent and about not letting the U.K. ‘get off easy' now that it is leaving the EU. The EU has put the U.K. in a difficult position on purpose to send a message to other EU member countries that might be thinking of leaving. The message is that leaving it really too painful even to consider. Still, the U.K. and the other EU members have had a long and strong relationship. Germany and the U.K. trade a good deal (U.K. imports 75 billion pounds from Germany). And if there is a hard Brexit, it will do damage on both sides of the Channel. Also the U.K. has the most capable military force in the region; it seems unwise for the EU to think that the U.K. will remain as fully committed to NATO and have ‘Europe's back' while Europe is busy sticking a knife in the aback of the U.K. economy.

Europe has a lot of sorting out to do. But the gauntlet has been thrown down and the EU has said it will not negotiate any further. Yet, Boris Johnson, the new U.K. Prime Minister, is making all sorts of noises about problems with the existing agreement and how the Irish backstop is unacceptable if there is a hard Brexit. For now there are two talking heads just talking past one another. It is not clear to me that Boris Johnson has any way to reopen negotiations with the EU. The way is shut.

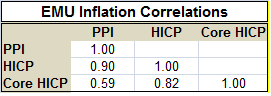

Meanwhile, the weakness in the PPI in Europe does have consequences for the HICP. The correlation between the two indexes is actually rather high at an R-squared of 0.8 since January 2012. But only about one third of the PPI change gets into the HICP. In terms of variation, the PPI is about three times more variable than the HICP. But they do move in the same cycles.

Meanwhile, the weakness in the PPI in Europe does have consequences for the HICP. The correlation between the two indexes is actually rather high at an R-squared of 0.8 since January 2012. But only about one third of the PPI change gets into the HICP. In terms of variation, the PPI is about three times more variable than the HICP. But they do move in the same cycles.

The weakening growth situation, weakening inflation trends, the ongoing Brexit tiff and pending trade negotiations between the EU and the U.S., and possible new trade deal between the U.S. and the U.K. all color the future in a very uncertain shade of near pitch black. Many of the European trends have been submerged or dealt with as simple collateral damage of the U.S.-China trade war up until now. But Europe is developing some boils and warts all its own that will need their own special attention.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief