Global| Jan 24 2018

Global| Jan 24 2018EMU Manufacturing and Services Take Different Paths

Summary

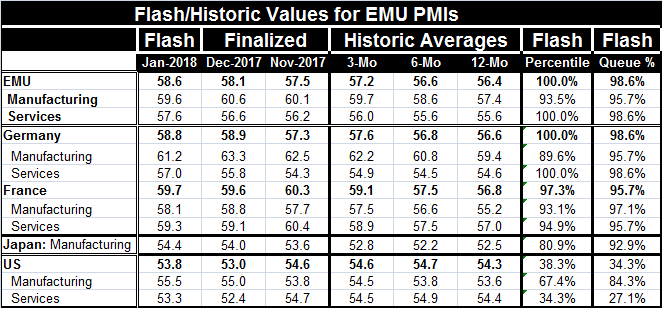

Euro area and German manufacturing PMIs stepped back in January while the services sector made gains. Services that have been flat or weaker terms of their 12-month and six-month average PMI levels in the EMU and Germany have broken [...]

Euro area and German manufacturing PMIs stepped back in January while the services sector made gains. Services that have been flat or weaker terms of their 12-month and six-month average PMI levels in the EMU and Germany have broken out in January. While the services sector averaged 55.6 over 12 months and six months, its January index breaks above that with a reading of 57.6. In Germany, the services PMI averages 54.6 over 12 months and a weaker 54.5 over six months then catapults to 57.0 in January. The German and EMU services indexes are now on their highest readings since January 2012. Overall EMU manufacturing sits at its 95.7 queue percentile standing with manufacturing in Germany at the same relative standing. France continues to show slow and steady progress in both of its manufacturing and services PMIs in January. Its various sequential averages continue to rise.

Japan also reports an early reading on manufacturing and it shows a gain in January. Japan's progress backtracked over six months as that average fell below its 12-month value, but over three months the PMI is rising again surpassing even is 12-month average; its January reading is its best since February 2014.

The U.S. follows a different path in January as its composite index falls on a weaker services sector and a stronger reading for manufacturing. The queue standing for U.S. manufacturing is solid at its 84th percentile, but U.S. services only have a 27th percentile standing. The Markit gauges are much weaker than their respective ISM counterparts. That begins to muddy the waters of trust for the PMI process.

The PMI indexes have been among the more encouraging data that we see on a global basis. They have been uniformly strong in the West and lagging somewhat among Asian countries. The January developing economy PMIs are not available, but as of December the EMU reading in manufacturing was 60.6 compared to 59.7 in the U.S., and 53.9 in Japan and 51.5 in China. While China and Japan still rank strongly over the period from 2012, their absolute scores are low because they have been in a depressed situation and remain so despite some pick up. However, in relative terms, Indonesia, Malaysia and South Korea also have weak or moderate readings for manufacturing with each of them sporting a raw score below 50 in December.

Having said that, there is still a gap between what PMI surveys of breadth say and what traditional measures of strength tell us. The chart on the right depicts the year-on-year gain in EMU manufacturing IP against the EMU manufacturing PMI gauge. In 2014 and 2015, the gap between IP and the PMI gauge was large. As growth progressed in 2016 and 2017, the gap has narrowed. That tells us the rise in the PMI index has not resulted in a comparable gain in industrial production. The relationship between the two manufacturing measures has changed. IP is still relatively strong in the EMU, up by some 4% year-on-year. But if the relationship with the IP had held pace with the PMI gain, output growth would be in the neighborhood of 7% not 4%.

There is no denying the strength in the PMI data, but there are concerns about what that strength means. Breadth (diffusion) is not the same as strength. And we see that in a direct comparison of the manufacturing PMI to the manufacturing industrial production index or its growth rate.

And there is also the question of momentum. Last month, for a group of 11 manufacturing indexes of Asian countries, only 57% of them improved month-to-month (China, Singapore, Japan, India, Indonesia, South Korea, Malaysia, Myanmar, Philippines, Thailand, and Vietnam). The average (unweighted) PMI was 51.8 in December, down from 51.9 in November. These are both weak readings (but consistent with growth). And even though the groups averaged (unweighted) PMI queue standing is at 71.7%, that standing only reflects that Asian activity is relatively 'solid' compared to a period in which the region has been weak. Asia is not weakening any more. But its growth is uneven and still poor.

The IMF yesterday moved up its growth outlook globally by two ticks basically because the most developed economies were doing better. But the observations above draw from PMI data that already seem to overrate growth in Europe. They do the same in the U.S. Additionally, in the U.S., the ISM PMI surveys are much stronger than the Markit surveys; thus, raising the question of what is really going on.

How does this all fit together?

The U.K. today reported out a 42-year low in its unemployment rate. Unemployment has been low or making progress in Europe and it is very low in the U.S. and Germany. But despite this 'strength' wage pressures in low unemployment rate, economies are not really present. There is some creeping wage inflation but really nothing special given the low pace. Central banks (except in the U.K.) are lowballing their inflation targets too. Does it occur to anyone anywhere in policy circles that this weak performance in Asia that has been a driver of growth and that is probably the low marginal cost producer in the global economy is the reason why the lack of slack in the West does not generate price pressure?

Globally, technology, trade and trend are keeping prices/wage low. I do not argue so much that Keynes was wrong or that Keynesian models don't work, but rather that for them to work they need to be modified and reapplied. Country limits and constraints no longer stop at national borders. Labor supply is a more globalized concept. If you think German, U.K. and U.S. unemployment rates are low and if you believe traditional Keynesianism applies, why aren't there wage pressures? Is it because firms can source product out of slack Asia? You see the domestic capacity concept no longer seems useful for labor or capital. The Fed continues to fight this admission tooth and nail. The Fed thinks that the Phillips curve is coming back. But the Phillips curve is based on old labor market and pricing dynamics that no longer exist. Firms no longer look to pass on cost increases. They look to stop them. And if they can't or won't raise prices, they surely are not rising wages or not doing so without a jolt to productivity and none of those conditions is present.

On balance, the PMI data can help us explain a lot about the trends in the global economy, but we also have to be careful to give these indexes some room to breathe. Breadth isn't strength. And you can't take the message of a PMI index fully to heart. Current evidence suggests that in this era of slow growth, breadth might be making better progress than strength. That is not surprising and it seems to be the same message as the one we get from the low unemployment rates. However, that is a more complex issue since there are strange goings on with labor force participation rates beyond just an aging population. Still, the relentless fall in unemployment is another example of breadth outpacing strength, as wages and higher paid jobs remain elusive even in the 'tighter' labor market.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief