Global| Jan 11 2019

Global| Jan 11 2019EMU IP Trends Turn Lower

Summary

The aggregated sector EMU totals for industrial production are not yet in, but there is a considerable country detail available and that shows widespread EMU weakness. Of the 11 EMU countries whose data are contained in the table, [...]

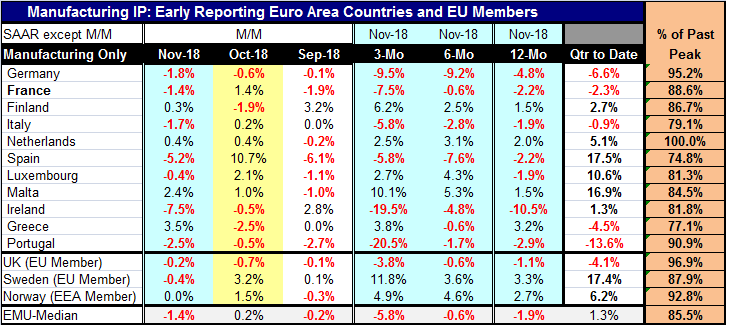

The aggregated sector EMU totals for industrial production are not yet in, but there is a considerable country detail available and that shows widespread EMU weakness. Of the 11 EMU countries whose data are contained in the table, seven show output declines in November. All four of the largest EMU members show declines in November: Germany, France, Italy and Spain. The U.K., still an EU member and a large economy, also has an output decline logged for November.

The aggregated sector EMU totals for industrial production are not yet in, but there is a considerable country detail available and that shows widespread EMU weakness. Of the 11 EMU countries whose data are contained in the table, seven show output declines in November. All four of the largest EMU members show declines in November: Germany, France, Italy and Spain. The U.K., still an EU member and a large economy, also has an output decline logged for November.

In October, five EMU members plus the UK show IP declines; in September seven-EMU members show declines plus the U.K. This has turned into quite a string of weakness.

In the quarter-to-date, only five EMU countries plus the U.K. show output declines that tells us that the weakness is still relatively intense as it remains lodged in the larger economies.

IP is also falling in seven-EMU countries plus the U.K. over 12 months and that includes the four largest economies in the EMU. Clearly, the weakness in the EMU is now relatively long lived (nearly one year) and broad based with up to 7 of 11 member countries showing outright output declines in manufacturing. IP fell over three months for all four of the largest EMU countries and the U.K. starting in February 2018. And while the degree of weakness did not endure, that seems to have been the start of the let-down. Of course, the PMIs for the EMU over this period have been weakening, but the IP weakness seems to have gotten out in front of the PMI weakness.

For the countries in the table manufacturing output averages about 85% of its past cycle peak. Production is over 90% of its past peak in Germany, Portugal, the U.K., Norway, and the Netherlands. The Netherlands alone is hitting a new cycle peak for output; the U.K. is the next relative strongest with output at 96.9% of its past cycle peak. Greece, Spain and Italy- all Southern European members - have standings in their 70th percentile indicating no capacity pressure and much more room to grow.

Markets range from confused, to distressed, to pleased, over central bank policies. Germans are very happy that the ECB has stopped its special stimulus programs and generally want the ECB to continue to normalize policy apace. Others are more wary based on the evolution of economic data. In the U.S., we find some very happy that the Fed has moved up the fed funds rate to its current position and encourage the Fed to continue to hike rates back to a normal level. Others look at markets and are warier of what the Fed is doing; they are glad that it paused. Some are quite concerned over the weakness engendered by rate hikes to date in the U.S. housing sector. Even so, that impact has been lessened by the flattening in the yield curve since so many mortgages have a long duration. Many in markets are simply confused about Fed policy since inflation continues to be in hand and below the Fed’s target and yet the Fed is still hiking rates. The current Fed policy is to pause amid what has been a lot of market turmoil. The pause has been well received globally. Turbulence in U.S. financial markets is quickly shared with overseas markets.

Knowing...and the danger of thinking we know

We are now at the cross roads where central banks have been headed for some time. The Fed in the U.S. has been tightening (raising rates) and shrinking its balance sheet. It is going to continue to shrink its balance sheet but will put tightening on a more patient path. That means the Fed is still tightening but not as rapidly and it is not a reversal of policy, just moderation. The question is: when will the ECB lift rates and begin its own balance sheet shrinkage? Can it even get there from here? The ECB has been planning to start these actions much later down the line. Will it be caught by economic weakness before it can get its rates higher? Those questions also apply to the BOE that has already cut rates then taken some of that back on Brexit concerns that have ebbed and flowed. Brexit in fact may be taking an unexpected turn into oblivion. News stories are now talking to Brexit supporters who seriously speak of the Brexit vote being recast and walked back. If Brexit goes away, there is a lot that has been done that may need to be undone. And confusion will stem from that as well. If Brexit is withdrawn, businesses will have outsourced work from the U.K. they did not need to. And EU governing bodies were relocated out of the U.K. since the U.K. was no longer to be a member. Would they come back? The un-Brexit will raise a lot of questions all on its own. And it is clear that we are now in a questioning stage of this economic cycle where nothing can be taken as given any more. Brexit is simply another unrelated example of how little we know about things we think we know.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief