Global| May 13 2020

Global| May 13 2020EMU IP Plunges...Leave No Sector Behind

Summary

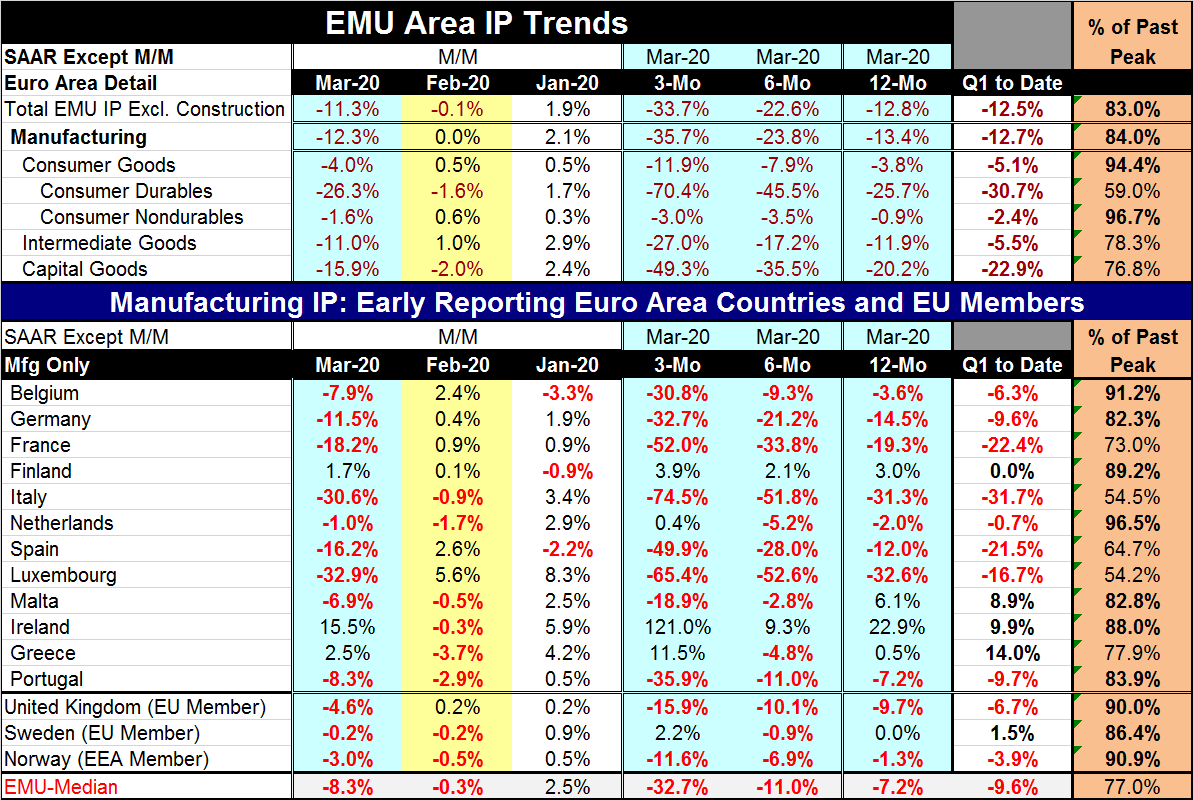

On a day that the U.K. has reported a 5.8% drop its economic activity in one month the largest ever, the EMU IP report finalizes with its own 11.3% drop in March. Manufacturing IP dropped by 12.3% in March as well. Of the Fifteen [...]

On a day that the U.K. has reported a 5.8% drop its economic activity in one month the largest ever, the EMU IP report finalizes with its own 11.3% drop in March. Manufacturing IP dropped by 12.3% in March as well. Of the Fifteen reporters in the table, all but three showed output drops in March. Only Ireland logged a large increase. Luxembourg and Italy posted declines in that one-month of 30% or more. Spain, France and Germany added their own drops of double digits in the month. Shutting down for the coronavirus has been costly indeed in Europe as it has been in the United States.

On a day that the U.K. has reported a 5.8% drop its economic activity in one month the largest ever, the EMU IP report finalizes with its own 11.3% drop in March. Manufacturing IP dropped by 12.3% in March as well. Of the Fifteen reporters in the table, all but three showed output drops in March. Only Ireland logged a large increase. Luxembourg and Italy posted declines in that one-month of 30% or more. Spain, France and Germany added their own drops of double digits in the month. Shutting down for the coronavirus has been costly indeed in Europe as it has been in the United States.

Just today the U.K. has announced it is beginning to unwind its lockdown. Meanwhile, a number of countries reported border policies that will largely keep European borders shut for about another month. Lockdowns are easing, but risks remain and everyone is walking barefooted on eggshells.

Country trends

Annualizing the IP declines over three months and six months simply produces more horrific results. Seven of 12 EMU members have three-month declines at an annualized rate of -30% or more. Six (nearly seven) have output declines at a double-digit annualized pace over six months. Eight have output declines over 12 months. The exceptions are Finland that shows output gains on all horizons. Also Ireland is an exception; it more aggressively shows output gains on all horizons as well as output acceleration. In the quarter-to-date, four and nearly six EMU members have a double-digit annualized drops. Contrarily, three countries post a double-digit increase in output annualized or something close to it (Malta, Ireland and Greece).

EMU sector trends

In March, all EMU IP sectors show falling output. There is a double-digit drop in capital goods output, intermediate goods output, and durable consumer goods output. But nondurable consumer goods show a much smaller decline and that helps to keep the decline in output for the overall consumer sector to -4% in March. February also saw a decline in output but the smallest fall possible of -0.1%. Capital goods and consumer durables led the way lower in February. January had seemed rather solid across the board with output increases. Clearly the virus came on hard and suddenly.

Growth

Sequential growth rates show extraordinary weakness. Over three months sector rates show declines ranging from an annual rate of -3% to -70%. All major sectors decline at a double-digit pace over three months. Over six months the decline in the consumer sector is a bit less at only a -7.9% rate of decline. Over 12 months the overall and manufacturing sector drops are in double digits along with capital goods output and consumer durables output. Intermediate goods slippage is nearly at a 12% pace and consumer nondurables decline at just less than a 1% pace. Quarter-to-date (that is now for a completed Q1) shows all sectors with output declining.

War of words over the ECB

The war of words between the Germans, the EU and the ECB about the propriety of ECB policy has escalated. The German Constitutional Court found the ECB policy to not be allowed and the EU commission said the Germans had no jurisdiction. Subsequently, Ursula von der Leyen, who is the European Commission President (and a German), suggested the possibility of a lawsuit. Today a member of the German Constitutional Court that last week was critical of the ECB's bond-buying plans said any legal action by the European Union against Germany over the ruling would “weaken or endanger” the bloc in the long run. I don't know what the Germans think or where they now stand. Is this a problem with the German constitutional court or the Bundesbank (which is not mentioned but must be there in the immediate background). Clearly Germany somehow wants a voice (maybe the Bundesbank dissent against ECB policy was overridden leading to this end run by the constitutional court in Germany). However, in what the ECB has done, the German court has been told that it does not have a standing. I guess the protocol would have been for a German contingent to press its case with EU judiciary instead of going it alone and trying to foist a German ruling on the EU. That was a bit heavy handed. I'm not sure if this more is a snit over what the ECB is doing or over the protocol of how to challenge a policy. Whatever it is, it seems serious.

Euro-Kumbaya

It is only clear from this fighting that the coronavirus has not brought everyone together. The U.K. left the EU arrangement over its increasing intrusiveness. Germany now is signaling that it has had enough to the ECB brand of largesse even as the EMU finds its members under a great deal of pressure and in need of relief. There is no common fiscal policy so that monetary action is all that is possible. And the German view is that the ECB under Mario Draghi may already have done too much. There is no room for more. So tensions in the EMU continue.

...and weakness elsewhere

In unrelated reports today, India reported a sharp drop in manufacturing IP of 20% year-over-year. In Japan, the economy watchers' index halved its reading from one month ago. Evidence of weakness, severe weakness and spreading weakness is plentiful, but at the same time most European countries are planning and taking early steps to end the lockdown.

And the U.S. example says, wait, go slow...danger

In testimony before Congress yesterday, U.S. expert Anthony Fauci, NAID Director, warned of the dangers of ending the lockdown too soon. In the U.S., this is not just a contentious piece of policy; it has roots with deep partisan divisions. How will anyone ever be certain that the risks are low enough to normalize? Must every single part of the Fauci plan be fulfilled in order to go ahead and take a step toward normalcy? Germany is engaged in a reopening but has just has some bad news about infection rates rising. Still, the German response is not to overreact to each data tid-bit but to watch it over time and see if the infection pick up is for real or not. In the U.S., policy will continue to be made by each branch of government according to the power of that fiefdom and the party or person that controls it.

That may not be the best way to proceed, but that is the way things are going to evolve.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief