Global| Dec 13 2017

Global| Dec 13 2017EMU IP Gains in October after Drop

Summary

The September decline in EMU industrial production was a stumble not a lasting problem. In October, IP is back in the plus column and since the September drop came on the heels of a strong 1.5% August rise, EMU IP continues to trend [...]

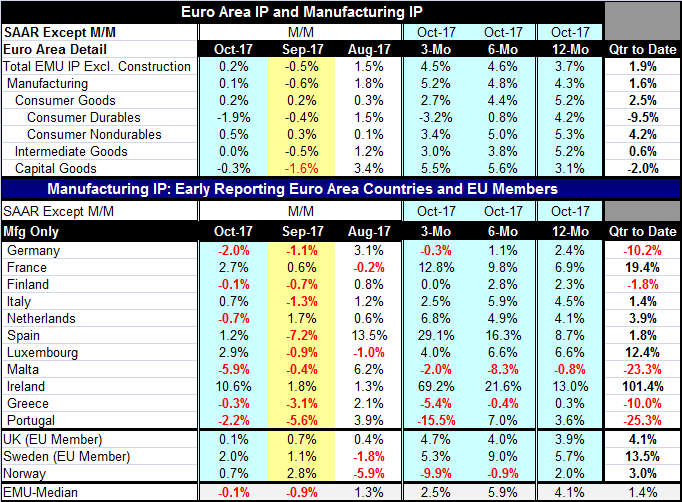

The September decline in EMU industrial production was a stumble not a lasting problem. In October, IP is back in the plus column and since the September drop came on the heels of a strong 1.5% August rise, EMU IP continues to trend strongly higher.

The September decline in EMU industrial production was a stumble not a lasting problem. In October, IP is back in the plus column and since the September drop came on the heels of a strong 1.5% August rise, EMU IP continues to trend strongly higher.

Headline IP shows improving growth rates, but manufacturing IP also shows sequentially accelerating IP gains. Manufacturing IP expansion is at 4.3% over 12 months with the pace rising to 4.8% over six months and elevating further to 5.2% over three months. Of course, such progressions are inevitably cut short... for now, growth is still accelerating and that sort of acceleration hints at an improved trend pace.

However, by sector there are divergences. This expansion is not being led by the consumer where growth rates are losing steam sequentially. The output of intermediate goods also is losing momentum sequentially as well. But capital goods output jumps from a 3.1% gain over 12 months to a pace of 5.5% or more over six months and three months and that is providing a lot of the push to production over the shorter horizon. Despite this effect, capital goods output is strong over three months because of a jump in August; output in that sector has fallen month-to-month in each of the subsequent months of September and October.

The trends within manufacturing give some pause to what otherwise might be exuberance. Clearly, IP is experiencing cross-currents of sorts. We have also seen some interruption recently in German shipments of capital goods despite what have been strong orders there.

Looking across the ranks of early IP reporters in the EMU among its original members plus Malta, we see output declines in October for six of these eleven early reporters. In September, there were declines across eight of eleven reporters. In August, when output in EMU rose briskly, output only fell in two of these eleven reporters, in France and Luxembourg.

Over longer horizons, however, industrial production expansion across the EU seems quite widespread. Over three months, IP is lower in only four countries: Germany, Malta, Greece and Portugal. Over six months, only two countries have output declines: Malta and Greece. Over 12 months, output is only falling in one country in the table, Malta. Apart from Malta, the smallest year-on-year performance is Greece's 0.3% gain, but after that the next smallest gain is 2.3% in Finland and followed by 2.4% in Germany and by more robust rates elsewhere, of course. Apart from several members, the year-on-year growth rates of IP in the EMU are quite solid and impressive. The trend still points higher for IP.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief