Global| Oct 12 2018

Global| Oct 12 2018EMU IP Gain Is Unexpectedly Strong

Summary

After two months of relatively deep declines, EMU IP has turned higher. It gained 1% in August over its depressed level of July. However, industrial output still declines on balance over three months and it is falling in the quarter- [...]

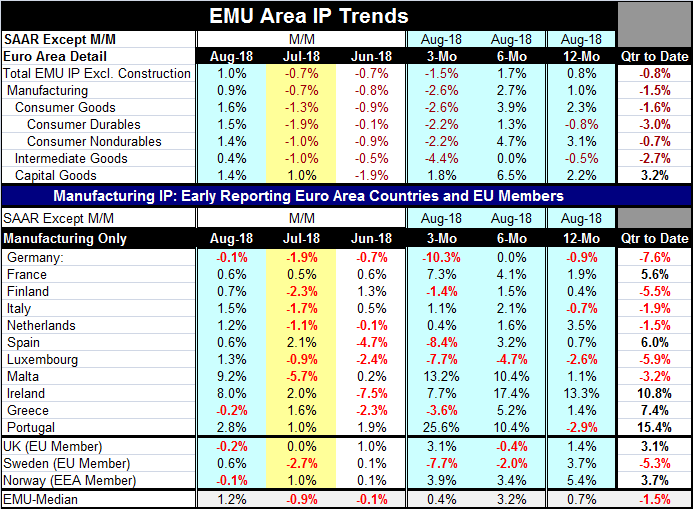

After two months of relatively deep declines, EMU IP has turned higher. It gained 1% in August over its depressed level of July. However, industrial output still declines on balance over three months and it is falling in the quarter-to-date. Output is only up by 0.8% over 12 months. The 1% rebound in August, while pleasant, does not put European output back in the high life by itself.

After two months of relatively deep declines, EMU IP has turned higher. It gained 1% in August over its depressed level of July. However, industrial output still declines on balance over three months and it is falling in the quarter-to-date. Output is only up by 0.8% over 12 months. The 1% rebound in August, while pleasant, does not put European output back in the high life by itself.

Consumer durables and intermediate goods output both show that output is lower on balance over 12 months. The small output gain that IP does manage over 12 months is on the back of a solid 2.2% gain in capital goods output and a 3.1% rise in the output of consumer nondurables.

Looking at the performance among early EMU member countries (we have 11 reporting in the table including late comer Malta; excluded are Austria and Belgium who have not yet reported IP data), we see than weakness lingers across EMU members despite the output gain in August. August saw output declines in only two of eleven countries in the table: Germany and Greece. But over three months, output is still falling in five of eleven countries as it fell by 1.5% (SAAR) in the EMU as a whole. As noted above, EMU output is up by just 0.8% over 12 months and that is with output falling in four member nations: Germany, Italy, Portugal, and Luxembourg. Over 12 months, only Ireland (13.3%) has industrial output growth in double digits. After Ireland, the strongest gain is 3.5% in the Netherlands, then 1.9% in France. Clearly, 12-month growth rates by county are skewed to the lower register.

Despite a solid across the board (more or less) set of rebounding data for August, the quarter-to-date (QTD) results are poor. Two months into the quarter, overall EMU output is falling at a 0.8% rate in the QTD; output is falling in six of eleven members.

When we talk about policy in the EMU, we speak exclusively of monetary policy since there is no EMU- or EU-wide fiscal policy. On the monetary front, Germany is experiencing some inflation pressure as its inflation rate at 2.2% is the highest it has been in seven years. That can be spun two different ways. One is to be fearful of inflation that is at a 7-year high. The other is to have some perspective and realize how tempered prices have been that 2.2% is the highest rate of inflation Germany has seen in 7-years - that is remarkable, especially as oil price recently have recovered sharply. And while Germans are hyper-inflation sensitive, their domestic CPI gauge excluding energy is still in a 66-month string of consecutive observations (5.5 years) in which year-over-year inflation has been below 2%. Meanwhile, EMU-wide inflation is just touch over 2% with a core pace just a touch over 1%. This theme of mildly excessive headline inflation coupled with quite low core or ex-energy inflation has some breadth to it.

Europe has not gotten to the point where it has a policy dilemma. It does have some internal strife since its hard money members are already eager to raise rates and the ECB is ready to end its special stimulus program. But the things that are worn in the EMU and EU are not going to be fixed by special monetary stimulus. The two most visible signs are the very uncompromising Brexit talks with the U.K. that have been dragging on and the EU Commission’s head-butting with Italy over the Italian budget. A rising sign of internal discord is also apparent in the flagging support for Angela Merkel’s coalition whose popularity has fallen to a record low. And there are well-known ongoing arguments over the migrant policy in the EMU with many members. These are the same policies that caused the U.K. to split off from the EU in the first place. The EU is sitting on a pile of trouble and not all of it has percolated to the surface yet. But there are a lot of matters that the EU and EMU have to attend to that like cans they have been kicking down the road instead of dealing with them. Inflation is only something convenient to talk about and complain about; it isn’t a real issue. The real issues are much harder to solve than that one... and they are being ignored.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief