Global| Oct 14 2015

Global| Oct 14 2015EMU IP Clings to Growth But Decelerates

Summary

EMU industrial production excluding construction (IPxC) fell by 0.5% in August after a 0.8% increase in July. Over three months, IPxC is net lower, falling at a 0.2% annualized rate. Over six months, IPxC is falling at a 1.2% pace. [...]

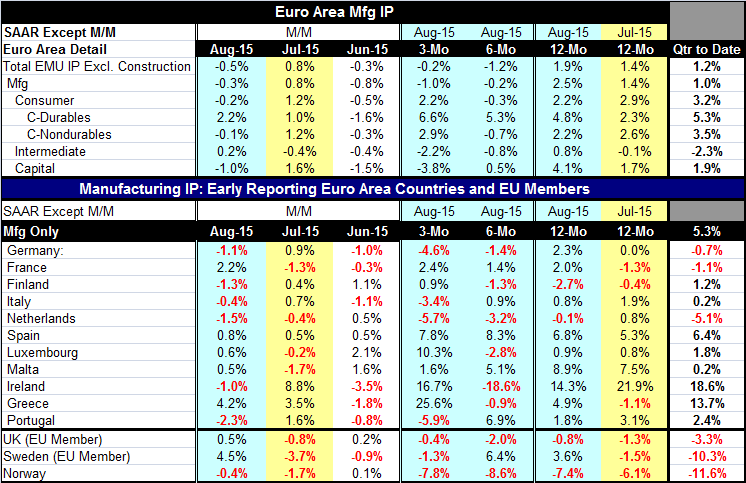

EMU industrial production excluding construction (IPxC) fell by 0.5% in August after a 0.8% increase in July. Over three months, IPxC is net lower, falling at a 0.2% annualized rate. Over six months, IPxC is falling at a 1.2% pace. Year-over-year, however, IPxC is still rising at a 1.9% annual rate. And in the quarter-to-date, IPxC is advancing at a 1.2% annual rate.

EMU industrial production excluding construction (IPxC) fell by 0.5% in August after a 0.8% increase in July. Over three months, IPxC is net lower, falling at a 0.2% annualized rate. Over six months, IPxC is falling at a 1.2% pace. Year-over-year, however, IPxC is still rising at a 1.9% annual rate. And in the quarter-to-date, IPxC is advancing at a 1.2% annual rate.

Manufacturing IP fell by 0.3% and is weaker over three months falling at a 1% annualized pace. Over six months manufacturing IP is off at a 0.2% pace while over 12 months it is up at a more solid 2.5% pace. In the quarter-to-date, manufacturing IP is up at a 1% annual rate.

Consumer goods show strength over three months, rising at a 2.2% pace, the same as their year-over year gain. Both capital goods and intermediate goods show three-month declines in IP and year-over-year intermediate goods output is up by just 0.8% as capital goods output is up by 4.1%. In the quarter-to-date, capital goods output is rising at a 1.9% pace while intermediate goods output is lower at a 2.3% pace.

There are mixed trends for industrial output, but only consumer goods are showing near-term strength and all of that is in consumer durable goods - and much of that is in autos.

There is a lot more country detail within the EMU now. The table shows manufacturing IP for 11 of the earliest EMU members. In August, six of 11 show output declines, up from four in July. Over three months, only four countries show IP declines: Germany, Italy, the Netherlands, and Portugal. Small countries have the most strength over three months with IP up at a strong annual rate in Greece (25.6%), Ireland (16.7%), and Luxembourg (10.3%).

Year-over-year manufacturing IP is lower in only Finland (-2.7%) and the Netherlands (-0.1%). On balance, year-over-year growth is still in good shape. But the recent weakness and its breadth is something to worry about. There were also IP declines in 6 of 11 EMU countries in June so this is more than a one-month soft spot. Overall monthly IPxC is lower in two of the last three months and it is lower on balance as well.

The European Central Bank still has its stimulus program in place and it has been steadfastly refusing to step up its pace. Consumption has been leading Europe while capital spending has been weak and now exports have begun to slow despite the weak euro exchange rate. China's recent weakness has come as a blow to the global economy; thus, contributing to weak commodity prices which are reverberating through global supply chain as well. There is nothing anywhere in the guise of new stimulus. There is still debt to work off and slower growing income which makes the debt burn off slow and painful. We have new weaknesses but not new strengths. Fiscal policy is frozen and monetary policy has been overused; these facts leave the global economy vulnerable. We are as vulnerable as if we were on the gold standard because policy is handcuffed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.