Global| Nov 16 2017

Global| Nov 16 2017EMU Inflation Stays Down

Summary

The chart does a good job of showing what inflation has been up to in the euro area. Inflation troughed in early-2016 after making a brief and deeper but shorter-lived trough a year earlier. In the wake of the recession/financial [...]

The chart does a good job of showing what inflation has been up to in the euro area. Inflation troughed in early-2016 after making a brief and deeper but shorter-lived trough a year earlier. In the wake of the recession/financial crisis/oil price collapse, inflation has been moving back toward normal as oil prices have been stabilizing after their dizzy ride of the past decade. After regaining momentum and rising to a peak in early-2017, prices once again are in a retrenchment mode with the pace of inflation falling compared to year-over-year highs made earlier this year. Inflation in Italy still seems to be trending lower. Inflation in Germany, France and the EMU as a whole has picked up but then softened again. Only France has a persisting rise in pace since 'bottoming' around midyear. The U.K. is included in the first table below because it is a large European economy, but it is not part of the monetary union. The U.K. is seeing the strongest headline year-on-year inflation and acceleration; however, its core rate is decelerating from 12-month to six-month to three-month. Despite this, the BOE has started to hike rates. British wages are still being eroded by inflation. The U.K. is being smacked around by forces that are hard to pin down as it struggles to set a post-Brexit-vote course for the economy.

The chart does a good job of showing what inflation has been up to in the euro area. Inflation troughed in early-2016 after making a brief and deeper but shorter-lived trough a year earlier. In the wake of the recession/financial crisis/oil price collapse, inflation has been moving back toward normal as oil prices have been stabilizing after their dizzy ride of the past decade. After regaining momentum and rising to a peak in early-2017, prices once again are in a retrenchment mode with the pace of inflation falling compared to year-over-year highs made earlier this year. Inflation in Italy still seems to be trending lower. Inflation in Germany, France and the EMU as a whole has picked up but then softened again. Only France has a persisting rise in pace since 'bottoming' around midyear. The U.K. is included in the first table below because it is a large European economy, but it is not part of the monetary union. The U.K. is seeing the strongest headline year-on-year inflation and acceleration; however, its core rate is decelerating from 12-month to six-month to three-month. Despite this, the BOE has started to hike rates. British wages are still being eroded by inflation. The U.K. is being smacked around by forces that are hard to pin down as it struggles to set a post-Brexit-vote course for the economy.

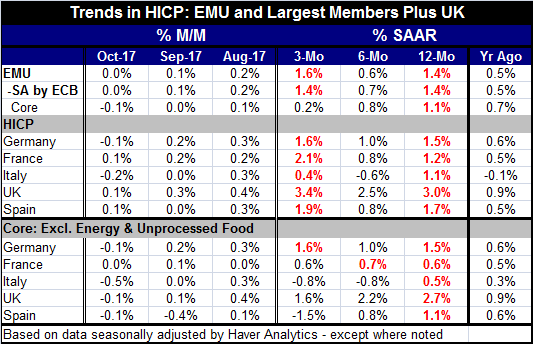

In the EMU six-month headline inflation is lower for all countries in the table compared to its 12-month pace. The three-month pace is higher than the six-month pace for all countries and the EMU. For the core, things are different. The six-month pace is below the 12-month pace and the three-month pace is below the six-month pace with a few exceptions. Yes, inflation is still decelerating. Those exceptions are France where the six-month pace is at 0.7% and barely above its 12-month pace of 0.6% - not much of an exception, really. The French three-month pace is back 'lower' at 0.6%, only even with its 12-month pace. Germany is the other exception and it is much more of an 'exception.' Its three-month inflation pace is higher than its six-month pace and the three-month pace also is higher than its 12-month pace. As a strong growing economy in Europe with the lowest unemployment rate, this is not a surprising result. But it is pure angst for Germany.

In addition to these trends, Italy has core prices falling over three months and six months. Spain has prices falling over three months. Despite German desires to get the ECB off the easing programs, there are lingering adverse and even deflationary conditions in other parts of the EMU.

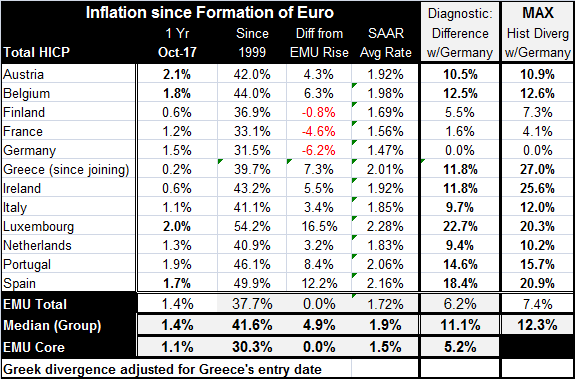

The second table is the headline inflation 'score' since EMU formation. The table includes the original EMU members plus Greece. This table gives you an idea of how competitiveness shapes up within the EMU which is a fixed exchange rate zone. Germany, France and Finland have kept inflation the lowest since the currency union was formed. German prices have risen by just 31.5% since January 1999. At the highest end, prices in Luxemburg have rising by 54.2% and in Spain by 49.9%.

Of course, the EMU mandate is for inflation a little less than 2% and it applies only to the aggregate EMU statistic. There are not country level 'targets.' Still, it is useful to think about inflation in that sort of country by country paradigm. Since the EMU was formed, only four countries are not on board for that: Luxembourg (2.3%), Spain (2.2%), Portugal (2.1%) and Greece (2.0%). Still, Germany enjoys a large advantage vs. most members because it has kept its inflation rate well below 2%, under 1.5% by a small margin. Given the German inflation pace, prices would double there in 47 years compared to in 35 years at a pace of 2%. Germany has built a competiveness advantage by keeping its inflation rate lower than everyone else and well below the ECB target which is a weighted average target of member inflation rates. Apart from Luxembourg and Spain, it is remarkable that Portugal and Italy as well as France - which has done amazingly well - have been able to leave their inflation-prone days behind them to keep inflation at or very near the ECB mandated pace. After all, these are countries that have long-run high inflation policies and relied on currency depreciation to close the competitiveness gap. Their economies had been designed to embrace inflation unlike Germany. The euro area experiment has been in force for nearly 19 years now. And while there are still some major problems in the area, it has weathered some really tough times; inflation differences no longer seem about to blow the euro area apart. Still, there are other matters of interest and populist movements still lurk at the national level although many of them have been defanged.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief