Global| Jul 15 2009

Global| Jul 15 2009EMU Inflation Really Does Turn Lower and Higher, Too

Summary

EMU inflation remained tempered in June; the Yr/Yr rate even turned negative! Headline inflations trend, however, is actually doing a slow up-creep as energy prices dived and have since begun to rise. But that was through June. [...]

EMU inflation remained tempered in June; the Yr/Yr rate even turned negative! Headline inflation’s trend, however, is actually doing a slow up-creep as energy prices dived and have since begun to rise. But that was through June. Recent energy market events suggest some of that rebound may be giving way. But with oil you can’t be sure. The ECB practice of ‘targeting’ headline inflations surely suffers a lot in times like this. The Fed’s preference to look at core inflation certainly looks superior and was a much better, more consistent, guide to policy in the recession and before when energy prices soared.

Energy prices never did affect the Fed’s preferred core measure of inflation much, while the ECB needed the ‘cover’ of an international rate cut to allow it to cut rates with inflation still screaming over the top of its target and the financial sector in dire need of a rate cut. Maybe someday the ECB will see the error in its ways.

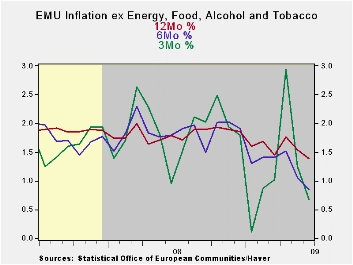

Core inflation technically has perked up slightly in June but it’s really hovering around the 1% mark. While there is tendency to look at such a mild acceleration as a non-event, the data across key EMU countries (where available) show that both core and headline inflation are engaged in an acceleration from 6-months to three-months. Germany’s core rate has accelerated from 12-months to six months as well.

With central banks having pumped a lot of liquidity into markets there are investors on edge and on an inflation watch despite the fact that some bankers still warn of a deflation threat. This report embodies all those oddities by having such low inflation – indeed a rate that drops year-over-year- but at the same time emits signs of inflation acceleration. The IMF has been cautioning countries not to wind their easing yet. But, if these inflation trends press ahead, there will be a moment of conflict not too far down the road.

The Fed has all-but-pledged to keep the stimulus on ‘longer’ noting that the BIG MISTAKE in past financial episodes has been for the central bank to let up too soon. The subtext of that message is that the Fed will not have a hair-trigger response to rising inflation despite concerns about its bloated bank reserve base. US core inflation and core is above the pace in EMU and even above the pace in Germany. While 1.5% to 1.8% to 2.0% core pace (core ex tobacco) step up in the US over, respectively, 12-mos to 6-mos, to 3-mos, is not severe, it is above Europe’s profile. With huge increases in the bank reserves in the US one wonders how long until some sort of inflation concern grips markets?

For now the recent flirtation with renewed economic weakness has trumped any concerns about inflation. It is also true that even core inflation often shows pressure when energy prices rise and the rise from energy this month was severe. This pressure too may pass. Still, there is a risk that policymaking is about to get more interesting. Perhaps the US and Europe are getting closer to a period when their policy directions will even diverge. That would have an interesting impact on currency markets.

| % mo/mo | % saar | ||||||

| Jun-09 | May-09 | Apr-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU | 0.3% | 0.0% | 0.0% | 0.9% | 0.4% | -0.2% | 3.9% |

| Core | 0.1% | 0.0% | 0.1% | 1.0% | 0.9% | 1.3% | 2.5% |

| Goods | 0.3% | 0.1% | 0.4% | 2.8% | 1.1% | -1.5% | 5.0% |

| Services | 0.1% | 0.1% | 0.4% | 2.2% | 1.2% | 1.9% | 2.5% |

| HICP | |||||||

| Germany | 0.5% | -0.2% | 0.0% | 1.1% | 0.7% | 0.0% | 3.4% |

| France | #N/A | 0.0% | -0.1% | #N/A | #N/A | #N/A | 4.0% |

| Italy | 0.3% | 0.0% | 0.2% | 1.9% | 0.7% | 0.5% | 4.0% |

| Spain | 0.0% | -0.1% | -0.1% | -0.9% | -1.4% | -1.5% | 5.0% |

| Core excl FE&A | |||||||

| Germany | 0.2% | -0.1% | 0.3% | 1.5% | 1.3% | 1.2% | 1.7% |

| Italy | 0.1% | 0.1% | 0.1% | 1.1% | 0.9% | 1.6% | 3.0% |

| Spain | 0.2% | 0.0% | 0.0% | 0.8% | -0.3% | 0.8% | 3.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief