Global| Aug 17 2018

Global| Aug 17 2018EMU Inflation Picture Gets as Dicey as the Outlook for EMU Policy

Summary

The EMU inflation picture has begun to get dicey with headline inflation at or above 2% for two months running and the core rate (excluding food and energy) running at a pace closer to 1%. Even Alice in Wonderland did not have it so [...]

The EMU inflation picture has begun to get dicey with headline inflation at or above 2% for two months running and the core rate (excluding food and energy) running at a pace closer to 1%. Even Alice in Wonderland did not have it so bad, she had two pills, one to make her larger and one to make her small; not one to make her too tall and small at the same time.

The EMU inflation picture has begun to get dicey with headline inflation at or above 2% for two months running and the core rate (excluding food and energy) running at a pace closer to 1%. Even Alice in Wonderland did not have it so bad, she had two pills, one to make her larger and one to make her small; not one to make her too tall and small at the same time.

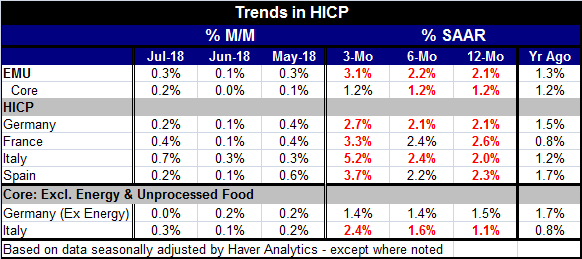

Headline inflation, the formally 'targeted' HICP measure, shows a progression to a higher pace as inflation rises from a pace of 2.1% over 12 months to 2.2% over six months to 3.1% over three months. Meanwhile core inflation is dead in the water at a pace of 1.2% over all those same horizons. This, of course, gives EMU members plenty to argue about.

Targets for inflation in the EMU refer to the headline and the pace is supposed to run at a bit less than 2%. During the financial crisis and then in the post crisis when oil prices screamed higher, Mario Draghi had operationally shifted the focus to 'core' inflation as rising oil prices boosted the headline in a way that the core had not responded. That split has given contrarians a solid argument for setting the headline aside even though the ECB has no formal dual mandate like the Federal Reserve. Growth in the EMU had been so poor that it was hard to make monetary policy without reference to that shortfall. For a while under the mandate of hitting the inflation target, the ECB adopted super stimulative policies to try to boost the inflation rate (more than growth) back to its targeted pace. Now that the headline is back closer to its target (albeit over the top), the core is still lagging, growth is less-stressed and this legacy inflation policy is bound to come under attack. This is especially true as oil prices stop gyrating.

The problem is that the ECB has been planning to arrange an exit from its super stimulative policies and growth has been looking better. But now several things are happening. One is that core inflation remains way to too low. The other is that headline inflation has become too high. The third is that growth that had appeared to be taking root and becoming firmer has been made more tentative as Brexit has dragged on and trade wars have threatened…and then there is Italy

Core inflation/ex-energy inflation is too low but it has been climbing

Oil prices have not yet stabilized, but they are believed to be close to levels where they will stabilize. For now oil prices are still up strongly from their lows of 2015-2016 and continue to show relatively sharp gains for their levels of one year ago. That means oil is still a factor in creating some temporary inflation pressure. Beyond oil Europe has some of the same concerns as the Federal Reserve in the U.S. as unemployment rates have dropped, labor markets have tightened and there is some concern that there next will be wage inflation although wage inflation has been one of the great missing persons acts of 2017-2018. No one is quite sure how that is going to work out.

Oil prices have not yet stabilized, but they are believed to be close to levels where they will stabilize. For now oil prices are still up strongly from their lows of 2015-2016 and continue to show relatively sharp gains for their levels of one year ago. That means oil is still a factor in creating some temporary inflation pressure. Beyond oil Europe has some of the same concerns as the Federal Reserve in the U.S. as unemployment rates have dropped, labor markets have tightened and there is some concern that there next will be wage inflation although wage inflation has been one of the great missing persons acts of 2017-2018. No one is quite sure how that is going to work out.

Meanwhile, the ECB-like the Fed, the BOJ and the BOE- has increased anxiety about interest rates and stimulative policies that may have been on the books for too long. Just as the central banking community was developing an independently arrived at decision to begin to withdraw stimulus, growth has shifted gears, geopolitical risks have heightened and the U.S. has become aggressive about pursing trade reform. All of this has upset the policy apple cart and the growth outlook.

In some sense, nothing has changed since central bankers continue to have the same objectives and responsibilities. But since monetary policy is made in the real world and not in a vacuum, the shift in real world perceptions does make a difference and it makes more of a difference to some than to others.

So it is that this month's inflation statistics in the EMU drive a wedge between 'warring' factions in Europe over monetary policy. The too-high headline inflation rate and the legacy of low rates and stimulative policy scream for one thing as the core inflation rate seems to demand another. All of this is only going to focus even more attention on the question of who will replace Mario Draghi at the ECB. There is no denying that the time is overdue for a German to run this bank since the ECB has been run by a Dutchman, a Frenchman and an Italian. It is interesting to stop here and note that in Europe the controversy is over the nationality of the next ECB head while in the U.S. the issue is over the race and sex of the next Federal Reserve member. It's not always about monetary policy but it is always something…

The ECB was formed under rules to make it as rock solid as the Bundesbank used to be then the financial crisis hit and a number of things took it away what had been expected to be its policy track. But economic circumstances hint strongly that snapping back too strongly to the Germanic vision of the ECB could be dangerous.

All of that has everyone on the edge of their seats, watching the ECB and the incoming data and the global economy. Everyone is aware of the difficult geopolitical environment and the international trade situation. No one is sure how it all shakes out. Of course, Europe is not without its own special problems as Brexit has dragged on and a new government coalition is seated in Italy with what seems like some very different ambitions. To say that we live interesting times would be an understatement.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief